An update from LGT Wealth Management Australia's Chief Investment Officer Scott Haslem

As investors, we are being challenged ferociously in the early months of 2026. While a casual glance at market indexes doesn’t scream alarm, below the surface, at a stock, bond, sector and regional level, volatility is rife. Some of this reflects this year’s relatively ‘hot’ start to geo-politics, as we discussed last month. But increasingly, violent bouts of dispersion are sourced from the uncertainty investors now face in assessing the likely ‘creative destruction’ associated with artificial intelligence’s (AI) pervasive acceleration. Which companies and sectors will lead in this AI apocalypse, how resilient are their moats, and who can reinvent themselves to survive and create value?

These are issues we will undoubtedly revisit – and provide guidance on – as we navigate this year. Markets in Australia, too, are mirroring many of these uncertainties. In this month’s Core Offerings, we turn our attention to Australia’s shifting interest rate debate. While we discuss the challenges facing the Reserve Bank of Australia (RBA) as it battles the recent uplift in inflation, we focus on what we believe are the more meaningful questions. Are we comfortable with an economy confronting a now lower 2% speed limit with a much larger government sector, a depressed level of business capex that’s impeding productivity, and an increasingly unaffordable housing sector?

Inside, we also briefly discuss our year-ahead outlook for Australian equities, and how they compare to global developed and emerging markets. We flag our decision to move overweight domestic government bonds where we believe starting yields are now attractive. We also update our latest thinking on the currency, which has the potential to squeeze higher near term.

I hope the government turns out to be more ambitious than it currently looks like it will be because if it doesn’t and productivity growth remains weak, the supply capacity of the economy will remain weak. That means that demand growth has to remain weak and real wage growth has to remain weak. That’s the fundamental problem.

Dr Phil Lowe, former RBA Governor, February 2026

During the second half of 2025, the cyclical recovery in Australia’s economy gathered momentum. The RBA had modestly trimmed their policy rate from a peak of 4.35% to 3.60% between February and August, contributing to stronger demand across housing and consumer sectors. Indeed, the economy’s growth rate accelerated from below 1% mid-2025 to just over 2% by end-2025.

As the narrative goes, 2025 and 2026 are the years where the growth baton will be passed from the public sector (which has been expanding rapidly) to the private sector (which has been in recession), creating room for renewed business capex, potentially spurring productivity with the hope of reinvigorating non-inflationary (near 3%) growth that boosts household living standards.

To date, the government sector – both federal and state – appears to have struggled to release the growth baton. Moreover, while the global economy retains its clearly disinflationary bias (for now), Australia’s cyclical recovery now appears to be supported by an increasingly positive global growth backdrop. As UBS notes, “the key lead indicators of the global cycle, such as PMIs and trade, are tracking higher. This is likely supporting commodity prices, which is important because Australia's largest export is commodities, and hence Australia's export values [are being] boosted solidly”.

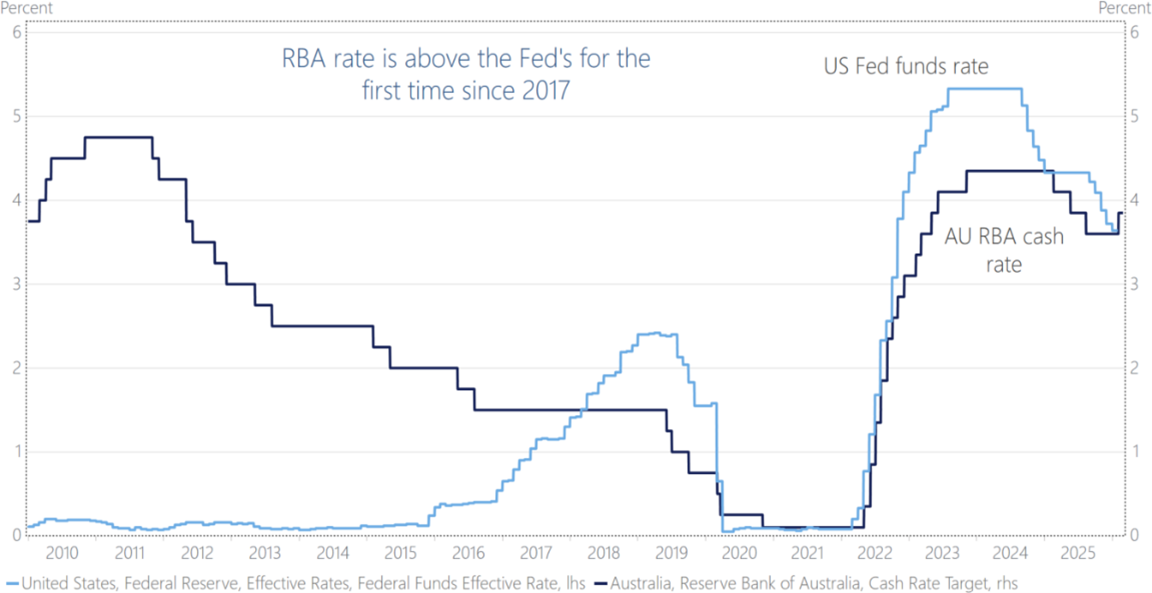

Together with an unexpected reacceleration in inflation through H225, these factors have led the RBA to reverse course in early 2026, and become one of the first in the developed market (apart from Japan) to hike rates this cycle. Like most economies, Australia’s jobs market has been relatively firm (with unemployment up only modestly). And with inflation reaccelerating above the 2-3% target, the new narrative is, as RBA Deputy Governor Hauser recently enunciated, that inflation is too high, partly reflecting a stronger economy that is operating against capacity constraints.

Hiking rates - the path of least resistance: Given this, the RBA has chosen the path of least resistance. It’s hard to be too offended by this (even if one questions how the Bank went from a vote of 9-0 to cut rates in August to 9-0 to hike them just six months later). Growth has reaccelerated; inflation is too high. Of course, there are parallels to other economies that are not hiking rates. In the US, the Federal Reserve’s (Fed) core PCE (it’s preferred inflation measure) is well above its target, growth is running well above trend, yet the market is priced for rate cuts.

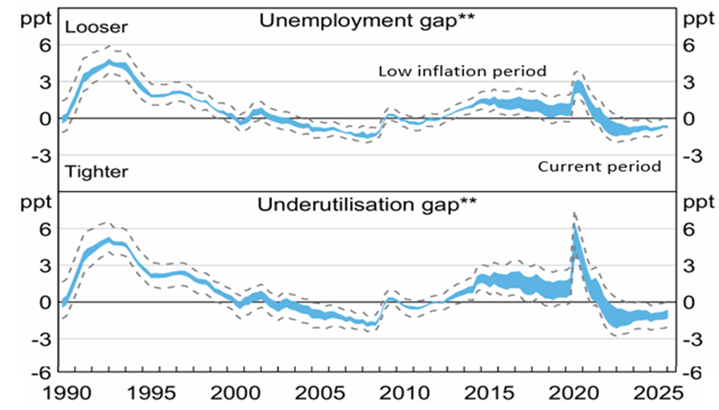

Key to the RBA’s reassessment is its focus over the past year on updated models of the economy that suggest a constrained capacity environment (low productivity, see Figure 1), that suggests the economy’s ‘potential’ rate of growth, or speed limit, is closer to 2% (no longer around 2¾%). Moreover, their analysis suggests that the unemployment rate below which inflation rises is about 4½% (not below 4%) and thus the ‘neutral’ or average cash rate might be 3.6% (not toward 3% as previously thought). Given that recipe, with the cash rate only at ‘neutral’, growth near potential and inflation rising, it’s no surprise the RBA hiked rates. Of course, as Daniel Susskind argues in Growth: A Reckoning (2024), economists’ growth models rely on “highly simplified” assumptions that strip away much of the real-world complexity they seek to describe. Their value lies in framing possibilities, not predicting precise outcomes. More time will help validate the RBA’s thinking.

Holding rates (no longer cutting) - the path of least regret: Which then raises the issue of whether the RBA could have taken what might end up being the path of least regret. Rather than reversing course to hike rates, the framing could have been more about the next move being higher should inflation trends not improve, holding fire to assess what has been a rapidly changing global and domestic geo-macro and data environment.

There has clearly been a lot of volatility in the inflation data, led by travel prices during the Ashes tour and government electricity rebates. Growth in private demand of 3.1% (recovering only relatively recently from 0.6%) is well below its pace ahead of prior hiking cycles, while employment growth of just 1.0% is half its average pace. With consumer confidence collapsing back to where it was before the first rate cut last year, and recent consumer spending data weakening, there’s a reasonable risk the economy will (regretfully) slow sharply over the rest of 2026.

And as far as the inflation outlook is concerned, there’s a strong case for lower outcomes as we move into H226. As Andrew Ticehurst from Nomura pens, “monetary policy is now tighter, fiscal policy is likely to be tightened a little bit, and the Australian dollar has risen as well…they’re all moving in a way which is going to cause growth momentum to slow this year”.

But is this the right debate, and are these the right questions? Sure, the RBA looks likely to hike rates one more time this year (most likely May), after which growth and inflation should (cyclically) retrace. Longer term, there appears to be more important structural topics to debate.

Over various long periods in Australia’s past, growth has averaged 3.3%, and from 2000-20, growth averaged 2.8%. But since mid-25, a range of forecasters – including the RBA, Barrenjoey, and CBA – have independently estimated that our ‘potential’ has collapsed to just over 2%. CBA put Australia’s “speed limit” at 2.1%/2.2%, attributing this to “persistently weaker productivity”.

Productivity, as a key contributor to the economy’s speed limit, also has a significant impact of what our ‘neutral’ RBA cash rate is – the rate above which policy is deemed to be ‘restrictive’. Previously, the RBA viewed a 3.6% cash rate (before last month’s hike) to be restrictive but has since shifted that view given the recent rising in inflation. Productivity also impacts estimates of the NAIRU – the non-accelerating inflation rate of unemployment – the rate above which inflation stops rising. This too has been lifted from around 4.1% by the RBA to 4.8% in its modelling (meaning today’s 4.1% unemployment rate needs to rise for the RBA to be confident inflation is returning to its target).

All of this is wrapped up in the RBA’s assessment that due to low productivity, Australia’s current 2.1% growth rate has consumed our ‘supply capacity’, which in turn is intimately linked to our failure to maintain our past near-3% speed limit via improving productivity. That lack of productivity growth is most frequently attributed to our lack of meaningful supply-side reform (despite our ability to host productivity round tables) as well as the rise in dominance of low-productivity services sectors, which in Australia’s case, has been led by the care economy and public sector more broadly.

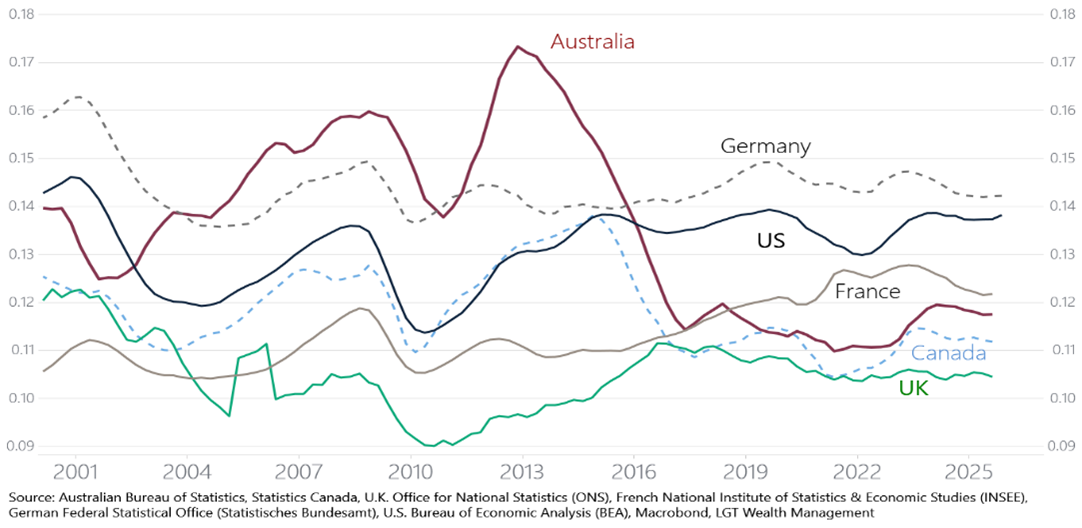

There’s no doubt the most recent data for Q3 signal a turn higher in Australia’s business investment, not surprisingly led by software investment. This is a pleasing development that provides some hope that the more cyclical elements of productivity will resurface in the period ahead and help support lower inflation and a higher growth ‘speed limit’ for the economy. But there is also little doubt that the collapse in our business capex from high teens as a share of GDP to low teens since 2016 (Figure 2, previous page) has been a critical contributor to Australia’s poor productivity performance (and new lower growth speed limit). Many will argue this reflects the unwind of the extraordinary mining capex boom from the early 2000s to mid-2010s. There is also the trend toward capital-light growth in a services and digitally dominated world (though this is also a global trend).

The key question is why the non-mining sector has not been able to fill that productivity gap. This likely reflects a range of factors, and we highlight three. Firstly, there is low expected demand. RBA research late last decade identified ‘expected demand’ as a key driver of firms’ capex plans, and linked business pessimism about the outlook to weak capex, despite low interest rates. Secondly, the Productivity Commission (PC) identified high input costs and regulatory complexities (including regulatory uncertainties) as a key headwind. Thirdly, there are structural factors, such as Australia’s high company tax rate relative our OECD peers (a factor highlighted by the Treasury and the PC). Australian firms’ bias to M&A and buybacks versus ‘risky’ organic expansion has also played a role.

That lack of productivity growth is most frequently attributed to our lack of meaningful supply-side reform (despite our ability to host productivity round tables).

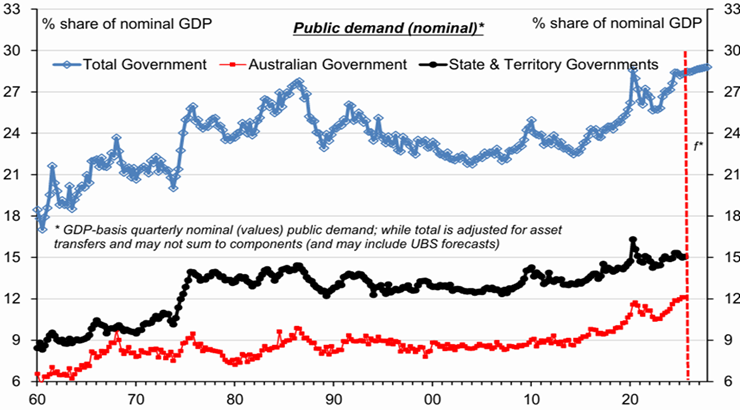

The recent rise to a record‑high share for government activity in growth (see Figure 3) largely reflects structural expansions in health, disability and aged‑care programs, a sustained public‑infrastructure and energy‑transition pipeline, higher defence outlays. The relatively weak private sector – both investment and consumption – over the past few years until mid-2025 has also contributed.

It might be argued that a larger ‘state’ is a necessary response to ageing, climate and security challenges and at least previously, acted as a stabiliser where the private sector was in recession. However, it’s also hard not to be more concerned about crowding‑out of the private sector, lower productivity (and its consequences for trend growth) and rising fiscal risk.

Ahead of this year’s May budget, the government is facing increased calls to slow the pace of its spending. Government revenue in the first half of this budget year is up 5%, led by 7% growth in personal income taxes. However, of concern, as noted by UBS, is that government spending has “mega-boomed” to be running at 15% y/y, its fastest since the COVID-related peak in 2021.

If there’s one structural issue that keeps coming up in our discussions about Australia, it’s housing. It’s no longer just a social challenge – it has become a macro headwind. We’ve had very strong population growth, particularly post COVID, for which housing supply has been unable to keep up. There is an argument that too much capital has gone into bidding up the price of existing dwellings and land, and not enough into building new stock or funding more productive business investment.

While debated, it’s likely the tax system has (modestly) reinforced that bias – in particular, the combination of negative gearing and the 50% capital‑gains tax discount makes leveraged investment in property relatively attractive, so a large share of household savings ends up chasing the same finite pool of established housing rather than being directed toward new, productivity-enhancing projects. This is likely squeezing household budgets, lowering labour mobility, and weighing on productivity and trend growth. It also means that rents and new dwelling costs keep showing up as some of the most persistent elements of inflation, even as other prices start to cool.

The policy debate is gradually converging on three big levers. First, the need to improve planning and zoning so it’s easier to build more homes – especially medium‑density – in the suburbs where people actually want to live and work. Second, whether we should rebalance tax and policy settings to encourage new supply and other business investment (with the 50% CGT discount a potential target in the upcoming Federal Budget). And third, the need to build capacity in the construction sector so that when demand picks up, more dwellings arrive rather than just higher prices.

As discussed last month, we expect global markets to continue to navigate the current geo-political noise. Globally, we are in the first phase of our three-phase macro outlook, namely ‘benign growth’, ahead of anticipating a re-acceleration of cyclical growth through mid-2026 that still provides a constructive backdrop for markets. Reflecting this, we continue to lean into risk, and remain tactically overweight equities relative to fixed income, with a bias to non-US markets.

In contrast, Australia appears to have landed more quickly into phase three of our macro outlook, where stronger growth leads to a moderate acceleration in inflation, and ultimately sees central banks turning their attention to removing liquidity and tilting rates higher. Reflecting this, our positioning in Australia is now overweight fixed income relative to equities (the opposite to global).

At the beginning of December 2025, we closed our underweight to Australian equities after an extended period of domestic market underperformance relative to the rest of the world. Since then, the local market has performed better. Indeed, as MST Marquee notes, while the February reporting season is not quite finished, to date, “this is currently the 2nd best reporting season” in 25 years. Earnings expectations for the current year have been revised higher by 2.2%, against a historic average decline of 0.7%. A number of factors lie behind that, from the reacceleration of the private sector economy due to the impact of previous rate cuts, to stronger global commodity prices on the back of a better global manufacturing impulse. Cost control has also been a feature.

Despite the recent stronger performance, we retain our neutral outlook for domestic equities, noting both positive and negative influences. The market is experiencing improved momentum in earnings, largely on the back of stronger commodity prices; stabilising net interest margins are a positive for the banks (with a further rate hike likely), and there is strengthening interest in value and dividend as factors in the year ahead, typically favourable for Australian equities. Countering these positives, valuations remain elevated and now higher cash rates and sticky bond yields leave less room for error if the domestic economy starts to weaken on the back of the recent rate hike (with a further hike likely in May 2026). While domestic earnings have been upgraded tidily, those upgrades still appear relatively lacklustre compared with other regions, especially Asia, Japan and the US. Moreover, at 18.4 times forward earnings, valuations are 1.5 standard deviations on the expensive side. Given that, while we believe the outlook has improved, we retain a neutral stance.

The significant reassessment of the outlook for the RBA’s policy rate – from rate cuts as recently as November 2025 to the market now pricing the risk of two further rate hikes this year – has seen Australian government bond yields significantly underperform their global peers. The domestic 10-year bond yield rose almost 40 basis points (bps) since 1 October last year to 4.70% by late February, compared with a fall of 5bps for the US 10-year treasury, which was trading at 4.04%.

We expect the RBA will hike the policy rate one more time (to 4.10%), most likely in May this year post the Q1 inflation data, returning close to the 4.35% mark that led to a significant slowing in the private sector economy during 2024. However, with this more than priced into markets, and the likelihood that consumer and housing activity may slow quickly over coming months – creating the ‘spare capacity’ the RBA needs – we believe this renders Australian government bonds incrementally more attractive, and we have moved overweight the sector this month.

The higher base rate in Australia also improves the relative yield on Australian investment grade credit (with fixed returns on longer duration bonds around 6%) and unlisted credit (where an 8-9% return is achievable), albeit we continue to encourage an increased focus on quality given potential economic weakness ahead.

The Australian dollar (AUD) has averaged around USD 0.75 since it floated in December 1983. However, over the recent past, it has been languishing below USD 0.70 (since early 2023), falling to below USD 0.60 briefly during the pandemic. Indeed, until recently, the currency appeared to ‘miss out’ on the appreciation that many currencies experienced, particularly the euro, with the US dollar on a material downward trend. However, with the sharp revision to the RBA rates outlook, the Australian dollar has jumped to USD 0.71 over recent months.

One of the most obvious drivers of the recent currency moves has been the cash rate. As the chart below shows, the local policy rate has been below the US fed funds rate for the past few years. That has now changed and with the RBA expected to hike as the Fed cuts, upward pressure on the AUD is likely to intensify over coming months. While a rise to USD 0.72-73 appears plausible into mid-year, both UBS (USD 0.67) and CBA (USD 0.63) expect the currency to be lower by end 2026. If the RBA is successful in fighting inflation by slowing the economy, this appears likely.

Staying constructive as markets navigate geo-politics, AI and reflation

Geo-political noise has continued to fill newspaper headlines this month, but markets have continued to navigate these risks. Beneath the surface, however, we are continuing to see significant dispersion across countries and sectors amid differing policy settings and as investors grapple with the positive and negative disruptive impacts of AI. Broadly speaking, we maintain our constructive positioning, recognising that equity markets are expensive and vulnerable to downside shocks.

The Supreme Court’s decision to strike down the Trump Administration’s reciprocal tariffs was yet another clear proof point of the constraints facing the President, as well as a reiteration of the strength of the US Constitution. We are closely monitoring the response of the Trump Administration and US trading partners. As it stands, Trump has made it clear that he wishes to replicate the pre-existing tariff regime via other authorities, though these would remain open to legal challenge.

More broadly, we continue to expect global central banks to maintain a dovish bias in Q1 2026. We expect this pulse of easier monetary policy to support a cyclical recovery for the global economy, particularly in more interest-rate sensitive areas such as the housing and industrial sectors. That said, we do acknowledge the risk that a stronger-than-expected recovery in global growth could impart upside pressures to inflation, forcing central banks to adopt a more restrictive policy stance late in 2026. Australia (with the RBA’s recent hike) may be a bellwether for this risk.

We believe 2026 will be a key proving ground for whether Large Language Models (LLMs) like ChatGPT can ultimately add enough value to the broader economy to justify their expense. We are already seeing increasing dispersion across AI hyperscaler share prices as investors grow more discerning and more insistent on return on investment. We are also seeing widespread volatility across sectors vulnerable to AI disruption, including software and computer services. While we expect significant volatility as investors parse through the negatives and positives of AI, we remain optimistic that AI adoption should support a broadening of the admittedly extended equity rally to smaller and mid-sized companies and to regions outside the US.

In summary, while we acknowledge a pick-up in near-term geo-political shocks amid expensive markets, we continue to see a broadly supportive macro and market environment in early 2026. We believe that investors should use this supportive window to ‘make hay while the sun shines’ and increase portfolio resilience for potential risks that may emerge later in H2 2026.

Policy uncertainty has peaked as a market-relevant risk. Despite the noise and bluster so far the year, our constraints-based framework tells us that trade and geo-political uncertainty have peaked in the near-term as market-relevant downside risks. While this may seem hard to believe, we judge that the triple constraints of bond markets, US Constitutional checks and balances, and voter support (or lack thereof) have and will continue to prevent worst-case outcomes from occurring. Of course, we recognise that new risks can always emerge, and investors should prepare for further potential shocks as the world increasingly comes to terms with multi-polarity.

Central banks may face hiking pressures in H2 2026. While policymakers should maintain a dovish line into Q1, a resilient US economy and rising reflationary risks may leave central banks on hold as the year progresses and the potential for rate hikes may come into the picture later in 2026.

Opportunities are ripe for ‘active’ hunters versus ‘passive’ gatherers: The best opportunities will likely lie beneath the broad index level, rewarding more active ‘hunter’ versus passive ‘gatherer’ investors. An active approach should pay dividends amid increasing market concentration and dispersion risks.

Make hay while the sun shines: The near-term macro back-drop continues to look supportive, with fiscal and monetary policy both in various stages of easing. Still, with potential reflationary storm clouds beyond the horizon, we believe investors should use the current ‘sunny’ environment to interrogate their portfolios and build in adequate resilience ahead of future rainy days. Prudent portfolio diversification and active management will be important tools in the astute investor’s arsenal.

Welcome to a multi-polar world: The global community is increasingly adjusting to a multi-polar world, an environment that should create more volatility and uncertainty but also present more growth and opportunities for investors who understand how to navigate and invest in a multi-polar world.

Are you ready for the ‘Great Recalibration’? We believe global trade, capital, and investment flows are in the process of a ‘great recalibration’ towards a more balanced setting with more active fiscal and consumer spending outside the US. This epochal shift carries significant implications for long-term portfolio design and construction.

The rise of artificial intelligence: AI presents key challenges and opportunities for the global economy and human society.

Higher base rates increase investor options: We expect interest rates to remain higher-for-longer. Higher base rates increase forward-looking returns across all asset classes, giving investors more options to build robust, multi-asset portfolios

Receive ongoing access to LGT Wealth Management’s insights and observations - a curated stream of thought leadership, market perspectives, and strategic updates designed to inform sophisticated investors.