Our minds have turned to the 'next big (beautiful)' thing, or more accurately, that which is 'unexpected' that could materially influence asset markets ahead (we acknowledge that, predicting the 'unexpected' is by definition paradoxical).

As we set sail into the second half of 2025, many (though not all) of the geo-political head winds we flagged just a few months ago-across peak trade uncertainty, a heated Middle East and the One Big Beautiful Bill-have somewhat calmed. Equity markets have responded favourably (and bond yields have not spiked), a helpful backdrop to our still constructive portfolio positions. In calibrating the compass for the period ahead, we've chosen to maintain our modest overweight to equities and have added risk in fixed income via investment grade credit. Yet, the outlook is not without angst, particularly in the US, leaving us favouring non-US global equity markets, while anticipating steeper bond curves and persistent volatility.

Our minds have also turned to the 'next big (beautiful)' thing, or more accurately, that which is 'unexpected' that could materially influence asset markets ahead. Tariff-induced inflation risks are arguably well considered, while central banks poised to further trim policy rates suggests a recessionary surge in unemployment is a bridge too far. In this month's Core Offerings, we ask whether the next year could witness a disinflationary shock (despite a structurally higher trend). US tariffs are forcing exporters to trim prices or ship elsewhere, while China's recent export surge may intensify competition with emerging Asia production. While not the worst 'shock' for market risk, it could heighten regional and sector dispersion.

Disinflation refers to a slowing in the rate of inflation - it means that prices are still rising, but at a slower pace than before (and is not "deflation", where prices are falling outright).

Many of the signposts we canvassed in our June Core Offerings, Where to now for the global economy, have pointed more positively over the past month (despite numerous episodes of heightened volatility). Renewed US tariff imposts as the 9 July negotiation deadline passed (extended to 1 August for some) have not exceeded the 'shock' rates of Liberation Day, supporting our thesis that we have now passed peak trade uncertainty. President Trump's One Big Beautiful (tax) Bill was also enacted without excessive bond market reaction. While arguably less 'irresponsible' than first thought, the greater near-term fiscal easing ahead of delayed (and dubious) tightening has been embraced by equity markets.

Moreover, threats of nuclear and oil price instability were also relatively swiftly dispatched as Trump summarily forced Iran to 'stand-down' and negotiate before an Isreal-Iran war was able to threaten a wider conflict. Indeed, the return of US 'deterrence'-with actions that were both impactful (bombing Iran nuclear facilities) but also avoided the US getting bogged down in a drawn out conflict-has allowed the US to retain its 'optionality' and signal it's lack of willingness to permit other potential geo-political hotspots to flare, including China's dalliance with Taiwan (and Russia's delay in ending its Ukraine war).

Recent data has also confirmed a subdued global inflationary environment before any tariff impacts have passed through to US goods prices, increasing the willingness of the US Federal Reserve (US Fed), and other central banks, to 'look through' the initial (hopefully one-off) price shock (before weaker US demand comes to bear in H2 2025). The market is expecting central banks to cut a further 0.5-1.0% over the coming year, and there's little in the recent macro data that argues against this.

Yet, while markets have clearly been buoyed by an emerging window of seemingly geo-political calm, there remains some significant challenges on the macro and markets front that have impacted the way we are positioning our portfolios for H2 2025.

Finally, in contrast to past periods of severe economic distress, the current environment has the advantage of being underpinned by relatively strong consumer and corporate balance sheet positions that limit their vulnerability to shocks (and still above average interest rates in the US, Australia and UK). Housing sectors globally are not goosed on rampant credit growth, and thus less vulnerable to collapse, and investment opportunities across thematics such as climate, defence and supply-chain logistics all argue a relatively low risk of a global growth collapse.

We've chosen to maintain our modest overweight to equities and added risk in fixed income via investment grade credit.

Reflecting these constructive developments-and a positive start to our tactical attribution as the new financial year gets underway-we've chosen to maintain our modest overweight to equities and have added risk in fixed income via investment grade credit.

Yet, while markets have clearly been buoyed by an emerging window of seemingly geo-political calm, there remains some significant challenges on the macro and markets front that have impacted the manner in which we are positioning portfolios for H2 2025. These challenges also suggest renewed volatility is unlikely to be long-absent over the coming year. Should some of these concerns rise to the markets' 'surface' over coming months, we stand ready to deploy capital into any 'risk-off' period, in line with our still constructive medium-term outlook.

Over recent weeks, both Europe and Japan have secured trade deals (at 15% tariffs) ahead of the 1 August deadline, toward the lower end of expectations.

With elevated fiscal issuance and more 'normal' inflation, a reduced ability for bonds to rally also lowers (but doesn't entirely negate) their diversification qualities, a nod to the need to allocate to defensive alternatives within multi-asset portfolios.

Outside the US, tariffs generally reinforce disinflation. In China, manufacturing overcapacity, weak domestic demand, and demographic headwinds point to continued deflation. Conversely, a domestic upswing and wage growth are driving inflation in Japan.

Our minds have also turned to the 'next big (beautiful)' thing, or more accurately, that which is 'unexpected' that could materially influence asset markets in the year ahead; of course, we acknowledge that, predicting the 'unexpected' is by definition paradoxical. Tariff-induced inflation risks are arguably well considered, while central banks poised to further trim policy rates suggests a recessionary surge in unemployment is a bridge too far.

Instead, we ask whether the next year could witness a disinflationary shock. US tariffs are forcing exporters to trim prices or ship elsewhere, while China's recent export surge may intensify competition with emerging Asia production (a negative impulse to world growth). While not the worst 'shock' for market risk, it could heighten regional and sector dispersion.

For many exporters to the US, the negative impact on demand for their products - as well as pressure from US importers to reduce import prices - may lead to significant changes in the global direction of trade over the next couple of years.

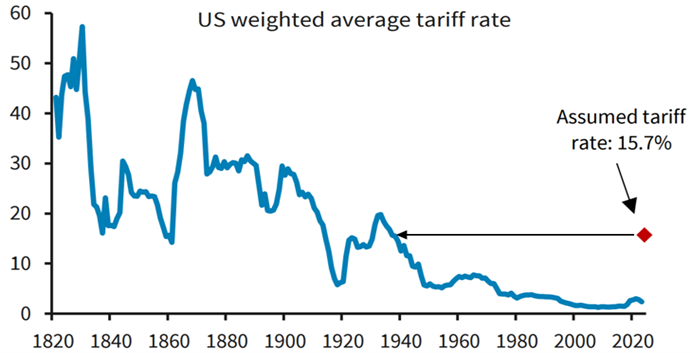

While US tariff outcomes surrounding the 9 July, and then 1 August, deadlines are proving less aggressive than those announced (and then delayed) at early April's Liberation Day, they are nonetheless material. Most analysts are estimating the US tariff average will be 15-20% moving forward, with obviously higher rates for some sectors, such as autos, steel and aluminium. For many exporters to the US, the negative impact on demand for their products-as well as pressure from US importers to reduce import prices-may lead to significant changes in the global direction of trade over the next couple of years. Moreover, there are essentially three key channels through which we expect US tariffs to impart a (potentially mild) disinflationary shock, on average, across the world.

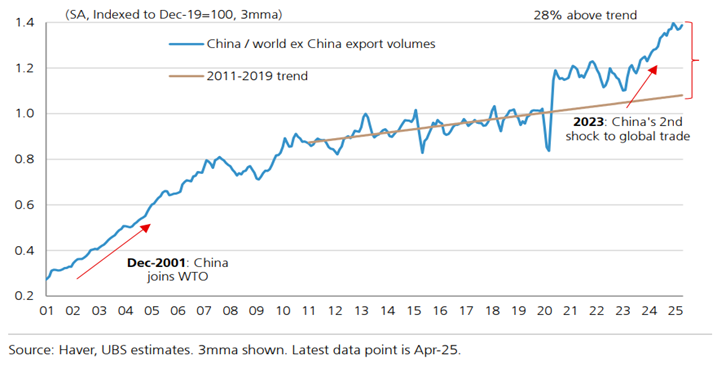

Since 2023, China's export volume growth has accelerated sharply, to be up around 20% (compared with just 6% for the rest of the world). Consequently-and as shown in the Chart below-China's share of world trade has lifted markedly over the past couple of years, and to well above its prior decade trend. Indeed, as UBS notes in its research, "this is China's strongest outperformance since the years following World Trade Organisation accession". China remains an increasing export powerhouse.

Interestingly, the vast majority of the additional exports, according to UBS, are finding their way to emerging (rather than developing) markets. The most significant increases have been to Russia, Africa, Vietnam and Singapore, partially offset by falling exports to the US, Europe, South Korea and Japan. Emerging markets now represent over half of China's exports, compared with only 40% in 2015. Key areas of increasing China export penetration include autos (particularly for Latin America), and household appliances (air conditioners, fridges and laundry appliances), particularly for Asia.

While China has undeniably been successful at re-directing exports to access many developed economies, like the US, via third markets, this absolute strength in exports goes much deeper than any 'trans-shipping' exercise, reflecting the establishment of new sources of demand for China's goods. UBS also argues that surveys suggest the (improved) quality of China's production is playing an increasing role in driving demand from emerging market consumers.

China is already experiencing significant domestic deflation pressure, with flat consumer prices and producer prices falling almost 4% a year in Q2. The bigger issue, however, is the impact on emerging market (ex-China) growth-also significant manufacturers-where there is evidence China's increasing penetration is deflating other countries prices and pressuring corporate margins. Reduced domestic production has the potential to weigh on local employment and activity more broadly.

While China's government has recently announced policies to focus on containing China's 'over capacity', this is unlikely to have a meaningful impact over the coming year, and with China's own policies targeting at boosting Chinese consumption proving slow to impact, there is an increasing chance that China's deflation will spillover in a more extreme manner in the year ahead.

Global equity markets continued to rally over the past few months, surprising many commentators who have highlighted ongoing trade/tariff uncertainty, geo-political volatility, US fiscal concerns, and a slowing US economy. We appreciate these legitimate concerns but also recognise that there are genuine constructive factors driving this rally. Our constraints-based framework helped us identify a peak in US trade uncertainty in mid-April (which we believe still holds) and a peak in geo-political uncertainty in mid-June (when US airstrikes ended the ’12 day war’ between Israel and Iran). If our thesis proves out, this will imply a significant reduction in negative tail risks to global markets and the global economy over the coming year or so.

We continue to believe that tariffs are ultimately disinflationary, particularly outside the US, and that ongoing progress on bringing inflation back to target will allow global central banks to continue modestly cutting rates into the back end of 2025. We also hold an out-of-consensus view that the recently passed ‘One Big Beautiful (tax) Bill’ in the US is more fiscally disciplined than first feared and is broadly balanced over the next 10 years once tariff revenues are included. This should support global fixed income markets, which are offering attractive all-in yields to investors. Resilient corporate earnings and the promising potential upside from the artificial intelligence (AI) roll-out could add another feather to the admittedly extended equity rally.

Downside risks remain, with still-high levels of overall policy and geo-political volatility, and growing signs of underlying frailty in the US economy. While many market commentators remain concerned about stagflation, our view is that the most likely downside scenario is actually a disinflationary negative growth shock. If such a scenario occurs, fixed income should reclaim its role as a portfolio diversifier.

Reflecting our view these negative tail risks have moderated and our conviction in fixed income, we have moved overweight investment grade credit this month, while maintaining our cautiously optimistic overweight to global equities. We have neutralised our US underweight via initiating a small underweight in Australian equities, to reflect the superior earnings growth and potential in the US market. We remain ready to respond to emerging risks and opportunities.

Has policy uncertainty peaked? Our frameworks tell us that trade and geo-political uncertainty have peaked, pointing to moderating (though still-present) tail risks to the global economy.

Tariffs are disinflationary: while we expect to see a mechanical lift in US goods inflation over coming months as tariffs work through the system, we continue to believe that as a tax that weighs on consumer and business demand, tariffs are ultimately disinflationary both for the US and the rest of the world.

Can central banks keep cutting? Progress on inflation and the ultimately disinflationary impact of tariffs should allow central banks to continue the global rate cutting cycle they started in 2024. US policy uncertainty presents a key challenge in balancing downside risks to growth with perceived inflation fears.

Opportunities are ripe for ‘active’ hunters vs ‘passive’ gatherers: the best opportunities will likely lie beneath the broad index level, rewarding more active ‘hunter’ versus passive ‘gatherer’ investors. This has proven particularly true so far this year.

Fortune favours the bold: 2025 is likely to continue to favour investors who can digest and exploit the opportunities that come with market volatility. Prudent portfolio diversification, across both traditional and alternative asset classes, and active management, will be important tools in the astute investor’s arsenal.

Welcome to a multi-polar world: The global community is increasingly realising that we have entered a multi-polar world, an environment that will likely create more volatility and uncertainty, but also present more growth and opportunities for investors.

The energy transition is growing more challenging: Policy uncertainty, cost, energy security, and more extreme physical impacts are likely to complicate an already-challenging energy transition.

The rise of artificial intelligence: AI presents significant challenges and opportunities for the global economy and human society.

Higher base rates increase investor options: We expect interest rates to remain higher-for-longer, particularly relative to the post-GFC zero interest rate policy environment. Higher base rates increase forward-looking returns across all asset classes, giving investors more options to build robust, multi-asset portfolios.

Receive ongoing access to LGT Wealth Management’s insights and observations - a curated stream of thought leadership, market perspectives, and strategic updates designed to inform sophisticated investors.