Outlook 2026

Rate cuts, reflation and the race for AI dominance

A wave of caution has swept over markets as 2025 draws to a close. And there's little doubt that this year has embodied much of the ‘disruption' as well as the ‘opportunity' we identified in last year's outlook piece, "Navigating disruption, discovering opportunity".

A wave of caution has swept over markets as 2025 draws to a close. And there's little doubt that this year has embodied much of the 'disruption' as well as the 'opportunity' we identified in last year's outlook piece, "Navigating disruption, discovering opportunity". Post the shock of Liberation Day, a cavalcade of geo-political events have largely proved 'surmountable', with trade deals struck, (some) global wars resolved and US bills and budgets passed. As forecast, tariffs have not been the inflation threat many thought, and with a much more moderate slowing in growth than expected, markets have delivered stellar returns in 2025. The opportunity has been to be remain constructive.

As we look ahead to 2026, battling questions around the longevity of artificial intelligence's (AI) dominance, we anticipate geo-political volatility will persist, but take a backseat to more macro factors. While global activity faces further slowing into early 2026, as trade disruption weighs, we forecast a cyclical credit-led growth recovery to emerge by mid-year that brings an end to central bank rate cuts - a more reflationary environment that initially supports equity markets higher through H126, but turns more challenging as the threat of liquidity withdrawal resurfaces.

Reflecting this, we further position for reflation as 2026 gets underway, looking through the recent market jitters to add some additional equity risk - and move underweight fixed income - for the immediate period ahead. Few would deny the complex market we face, where active management and truly diversified portfolios will earn their keep. Even those sold on the AI revolution should ensure portfolios aren't over-exposed. Equally, building in additional inflation protection for the next couple of years ahead should be paramount for those who value portfolio resilience.

Elevating 'reflation' to our base case…but it's more 'growth' than 'inflation'

Charles Kindleberger's "Manias, Panics and Crashes", while penned in the late 1970s, reached the peak of its fame in the wake of the 2007-2009 Global Financial Crisis. His historical framework analysed periods of speculative excess - or bubbles - from the 1630 Tulip Mania to the 1929 Great Depression. His enduring thesis was that while many forces can fuel a speculative upswing, there's ultimately only one force that ends a bubble, namely, the withdrawal of liquidity.

The performance of markets and economies as we traverse 2026 is likely to be intimately impacted by the durability of the AI thematic, from the performance of companies to the impact on economic growth of its unfolding capex pipeline. Judging the AI thematic's path with confidence is near impossible (albeit watching semi-conductor margins for pressure may provide some warning).

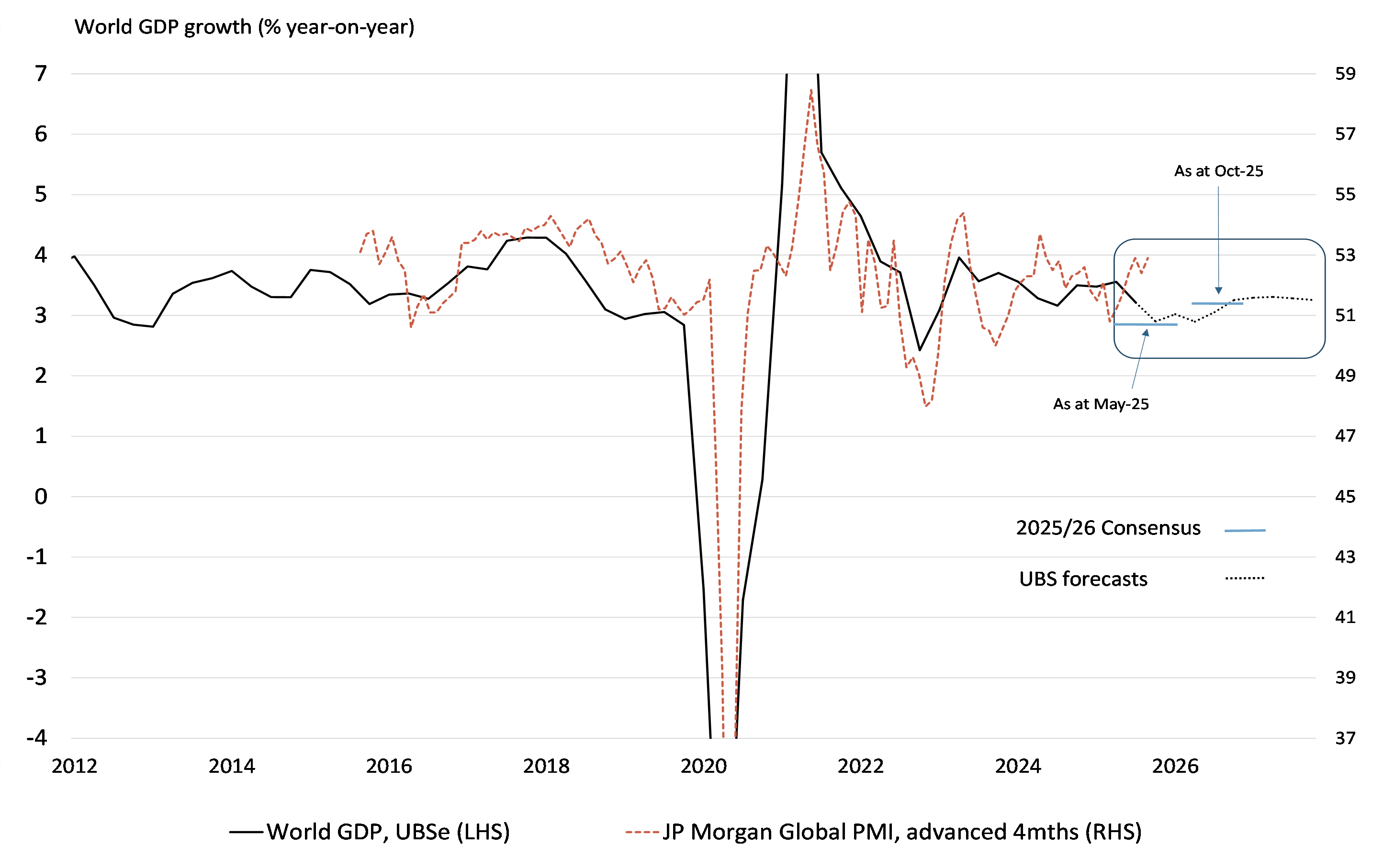

Figure 1: Slower growth into early 2026 - but slowing has been much less austere than expected.

Yet the ongoing macro backdrop of benign inflation and lower central bank rates, gives us some comfort that liquidity withdrawal - through Kindleberger's lens - is not in our immediate future. However, it is now a risk we see emerging as we move beyond the middle of next year.

In our October Core Offerings, "Reflation risks rising", we reaffirmed our central case preference to remain constructive on markets. As we wrote, "markets should be able to continue navigating higher as global growth slows (but doesn't collapse), inflation stays benign (at least outside the US) and central banks trim rates just a few more times". While the risk of a more sinister disinflationary shock wasn't entirely dismissed, we took the opportunity to up-weight our perceived risk that over the coming year we may enter a period of 'reflation' - more growth and less disinflation.

As 2026 comes into view, we now elevate 'reflation' to our central case for the year ahead. While economists typically view reflation as a period where economies are recovering from below target inflation (or even deflation), financial markets more commonly see it as any period where growth is accelerating, and inflation is rising (from virtually any starting point). As discussed below, we see a period during H126 where the reflationary impulse is driven mostly by a moderate credit-led growth recovery. However, there is then a risk this gives way to a period where liquidity is no longer being added (rate cuts end), and the longevity of the upward market cycle becomes a focus.

Three macro considerations for the year ahead…

Global growth should slow further into early 2026 - a lack of US data visibility complicates our assessment of the outlook. Nonetheless, the US jobs market is slowing due to still-tight policy, the tariff-induced trade shock has stalled H225 growth in Europe, the UK and Japan, while China has yet to stall its weakening momentum. This is likely to bleed into early 2026 activity, keeping inflation benign, and underpinning further modest rate cuts (in the US, the UK and others).

Growth should reaccelerate beyond Q126 - monetary policy acts with a lag, and with global central banks in 2025 amidst a meaningful cutting cycle (and the US Federal Reserve (US Fed) adding more liquidity in December by ceasing QT), a credit-led recovery in the non-AI economy - led by consumer and housing sectors - is now our 2026 central case. Fiscal easing in the US, China, Europe (having already halved the policy rate to 2%) will also support growth.

Challenges could arise in H226 as jobs markets re-tighten - this would likely forestall any further rate cuts. And should inflation trends deteriorate, tighter monetary policy could eventually follow (as early as late 2026). The evolution to a more inflationary 'reflation' impulse, and reversal of liquidity, could pose challenges for both equity and bond markets later in 2026. Monitoring that evolution will prove a key macro driver for returns as 2026 unfolds.

Three portfolio considerations consistent with reflation…

Cycle shifts and tail risks could drive volatility - as our secular outlook defines, the world is more complex. Markets are also more vulnerable when valuations are 'full'. Risks around an earlier than expected 'checking' of the AI thematic, a Japan carry-trade 'bust' or numerous geo-macro events, could challenge the markets' ability to navigate higher for a time (at any time).

Active management will add defence - we continue to view active management as more likely to be a defence where indices are concentrated and dispersion across sectors and regions remains a persistent theme in the year ahead. Monitoring diversification and avoiding over-exposure to dominant themes (like AI or defence) will also be key to portfolio resilience.

More inflation protection may be needed - in a more reflationary cycle (within an ongoing more inflationary secular outlook), increased exposure to real assets (infrastructure, but also commodities), as well as low-beta hedge funds, should add to portfolio resilience. We now take a more neutral view on fixed versus floating exposures (having previously favoured fixed).

Three tactical decisions we've made for 2026…

Adding modestly to our equity overweight - we are lifting our equity overweight from +1 to +2. Concentration of AI and elevated valuations keep us neutral US equities for now, with our overweight biased to Japan and Europe (where we continue to embrace positive structural themes across growth and earnings). We add to our equity position by closing our Australian underweight, which has performed well over recent months (but reached peak historic underperformance). Being neutral Australia should provide more defence should emerging markets recover strongly - it is also a market with a lower beta to the technology thematic, providing diversification benefits in the event of a correction.

Funding this by trimming high-yield credit - we remain underweight government bonds, a non-consensus view that may detract from performance near-term as growth slows. We move underweight fixed income by trimming high-yield (HY) credit but remaining +1 in (quality) investment grade credit. While we have harvested strong carry in HY, its higher beta to slowing growth (and the end of the rate cutting cycle) makes it an appropriate funding source.

Maintaining only a small underweight to cash for liquidity - recent strong market gains since Liberation Day suggest the risk of a meaningful near-term correction (but not bear market) remains. Reflecting this, we retain only a small underweight to cash to ensure liquidity to respond to future drawdowns. Were US equities to correct sharply over coming months (absent systemic or structure inflation factors), we'd be more inclined to add further to risk.

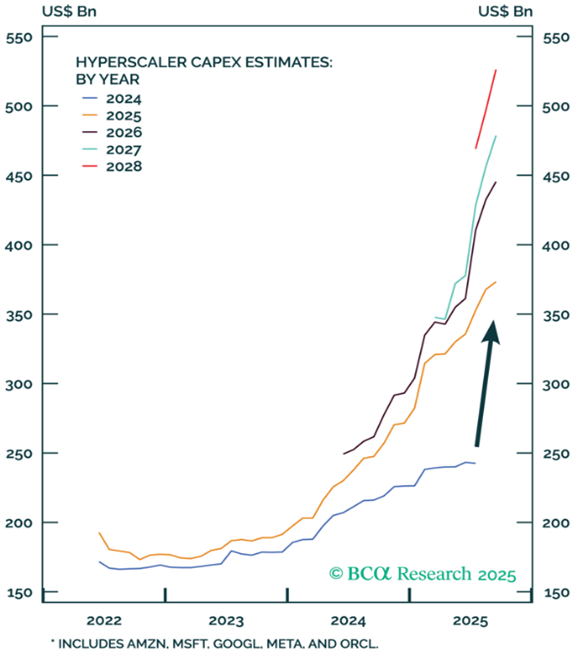

Figure 2: Capex is set to boost economic activity in 2026…could the bullish narrative shift?

Source: FactSet, BCA Research

"We are not yet displaying 'top of a bubble' characteristics. Capex from hyperscalers has been rising aggressively. However, a key difference is the free cash flow available to the big firms today. Their net debt, their margins, and earnings are dramatically different to those in the 1990s. The number of M&A and IPO deals don't suggest euphoria".

UBS Outlook, November 2026

The race for AI dominance

We note the well-founded concerns around AI over-investment, revenue expectations, and whether Large Language Models (LLMs) like ChatGPT can ultimately add enough value to the broader economy to justify their expense. That said, while LLMs are the current posterchild for AI, we are also seeing development shift towards different paradigms, including agentic AI and integration with robotics. Advances in these areas could unlock further productivity gains, while the broader economy is rapidly rolling out and testing the real-world practicality of LLMs in the workplace.

We also see an important geo-political dimension beyond these private sector fundamentals - both the US and China openly view the race for AI supremacy as a key theatre within their broader geo-strategic rivalry. As such, both superpowers have invested heavily in supporting their national AI champions, with recent US government investments into Intel and the recent court ruling preserving Alphabet from break-up two key case studies. As this global race for AI rapidly adopts 'Manhattan Project'-esque urgency, we expect both nations (and perhaps the Eurozone) to maintain a strong level of state support for AI investments over the medium-term, a dynamic which could provide further fuel to the AI 'bubble' and potentially sustain it for longer than might appear rational.

Equities - a year of more measured returns?

With global equities having another strong year - up 19% (14% in AUD terms) - despite a bear market in April, it likely increases the hurdle for a positive outcome in 2026. With AI euphoria having driven significant gains, and valuations full, we are faced with a 2026 outlook that may embody more measured returns. Indeed, if 2026 is to be the fourth consecutive year of positive returns, it would be the first such streak since 2003-07 (five years) and before that 1993-99 (seven years). The recent quantum of returns is also striking. On a rolling three-year basis, the ~80% cumulative return is close to 'as good as it gets' over the past 40 years. This does not preclude another year of solid returns, as seen during the late 1980s, 2006-07 and 2012. But it is also worth noting that investors were forced to confront meaningful drawdowns in the year after.

With investors increasingly focused on AI spending plans, AI financing plans, and AI productivity gains, this arguably sets investors up for a more volatile investment environment. Sure, that may seem hard to imagine given the Liberation Day sell off. But it is worth noting that investors have not seen a 5% or greater drawdown outside of this period since September 2024. For now, equities look likely to embrace numerous tailwinds that remain supportive for future gains - continued policy easing, ongoing AI capex buildout, the end of US Fed QT, record corporate margins, and a broadening of participation, as the earnings 'delta' between equity cohorts narrows e.g., between large cap tech and the S&P 500; between Europe and the US.

At a high level, although we continue to expect the US to remain 'exceptional', it is expected that other regions will, at the margin, become more attractive. Just as higher interest rates removed the TINA trade for equities (There is No Alternative), we think US geopolitical policies - as it relates to China's technological access and European defence spending - has created alternative geographic access points for investors, at a time of record US dominance in equity markets. Japan is now a viable investment destination and although Emerging Markets have rarely seen both Indian and Chinese Equities perform well in tandem, it's possible that both these regions perform better next year. This leads us to a constructive equity market outlook, cognisant and watchful for drawdowns, and looking to allocate marginal dollars to non-US equity markets.

Where are the downside risks?

If our base case for a reflationary economic backdrop proves too much, and the US economy overheats, it could make long end yields unpalatable for equities. The 'AI bubble' could burst, German fiscal stimulus may disappoint or take longer to permeate the economy. There are also US mid-term elections to navigate in H226, and the US labour market is showing signs of weakness. Some investor unease in credit markets, particularly the burgeoning private credit sector, also bear watching.

Fixed Income - credit should outperform bonds as reflation emerges

Fixed income investors should initially be beneficiaries of the near-term phase of moderating growth and further central bank cuts. Yield curves in major markets such as the US, UK, and Australia are expected to stay moderately steep, as long-term yields continue to respond to fiscal developments. A renewed reflation environment through 2026 could also add upside impetus to long-dated yields. Domestically, the Reserve Bank of Australia (RBA) is expected to remain data dependent ahead, focused on job market weakness to balance recent inflation surprises. The potential for more upside surprises in inflation means investors should not be complacent. Australian government bond yields may continue to underperform global peers, given the RBA's more cautious stance.

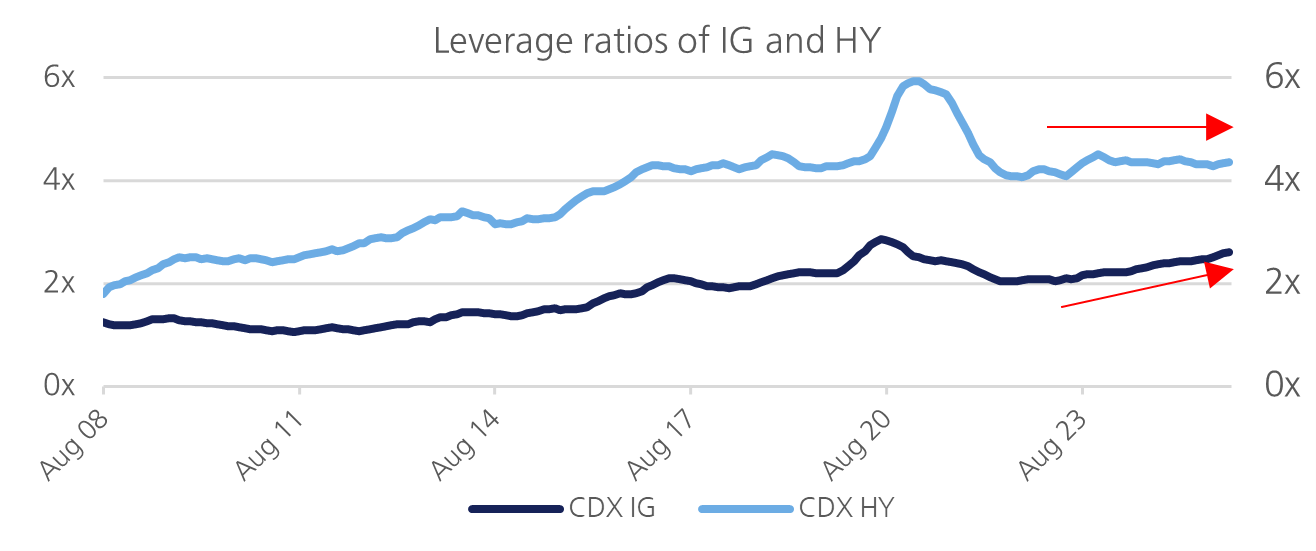

Within investment grade credit, fundamentals across corporate leverage and debt servicing remain healthy, supported by stable earnings. Credit spreads are close to their cycle lows, yet outright yields continue to attract demand. We anticipate robust supply in 2026, as borrowers seek to lock in funding. Floating-rate structures should remain popular, especially as policy rates base. Within investment grade credit, we will be closely monitoring leverage metrics, particularly to assess whether AI-related capital expenditure issuance remains at sustainable levels. We continue to maintain a quality bias in investment grade credit. While spreads may widen should macroeconomic conditions deteriorate, the underlying fundamentals should help protect portfolios. High yield markets present a more nuanced picture, being toward the richer end of history with yields below recent peaks, limiting return prospects. While carry income likely declines as final rate cuts are delivered, a reflationary environment through mid-2026 may benefit credit, generally.

Figure 3: Comparison of Debt/EBITDA for Investment Grade and High Yield credit - we continue to maintain a quality bias in investment grade credit.

Source: Bloomberg, Goldman Sachs.

Alternatives - a source of portfolio resilience

Private markets are experiencing similar challenges to public markets with some sectors also reporting stretched valuations and demonstrating high exposure to AI market themes. Some examples include investments in energy and data centre assets and technology financing. Alternative investments nonetheless do provide a differentiated source of portfolio resilience via infrastructure and hedge fund exposures.

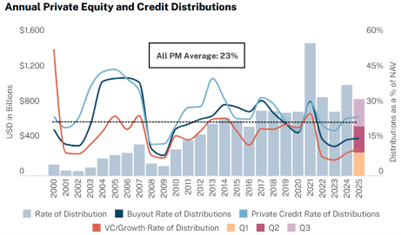

Private Equity - exits remain muted relative to the overall market net asset value. There are however signs of improvement across traditional routes e.g., IPO and trade sales where valuations appear elevated but not grossly over-valued. Secondaries remain our preferred space through 2026 as we like more complex GP-led secondaries relative to discounted LP-stakes. These investments are becoming increasingly competitive amid excessive evergreen capital flows, particularly in the US. Venture capital and growth equity are capturing major AI growth trends outside of the larger public stocks. We expect this to continue but it's not without risk, as paper gains are just that - we will be looking to appropriately diversify to reduce overall risk. Figure 4: In absolute numbers, exits (distributions) are on track to be the second highest on record but as a percentage of Net Asset Value, the level of PE exits (distributions) are only just above GFC levels

Source: Hamilton Lane Data via Cobalt (October 2025)

Private debt - in light of recent global media "noise", we continue to believe that private debt remains incredibly well-positioned for 2026. Despite interest rates and spreads declining, private debt relative to its public counterparts continues to outperform. In the coming year, secondaries are particularly attractive in diversifying exposures and asset-based finance is also an attractive alternative diversifier to corporate debt. Looking forward, manager dispersion is likely to be heightened across all private equity, venture capital and debt, so partnering with the right firm is becoming more imperative.

Private Infrastructure and Real Estate - these are likely to continue to grow in prominence in portfolios. Private infrastructure's exposure to major mega-trends including digitisation and decarbonisation should perform well next year given its clear linkages to AI and underlying inflation-linked revenue streams. Supply constraints across sectors locally combined with increasing tenant demand, points to improving prospects for domestic commercial real estate. Potential future rate cuts and their impact on cap rates is also an upside risk for 2026. We continue to see value in building out core-plus and value-add (infrastructure) exposures via secondaries globally, particularly in mid-market assets that have historically been valued at a discount to large cap assets.

For Hedge Funds - we believe the current environment (close to full equity valuations and tight credit spreads) are increasingly conducive to its core return drivers. JP Morgan referred to the 'end of the alpha winter', quoting higher rates, elevated equity volatility, and high stock dispersion, which are all expected to be in play through 2026. We believe that hedge funds and other diversifying return streams (notably insurance, royalties and litigation) have the ability to deliver attractive risk-adjusted returns that are uncorrelated to traditional markets and will have a more important role in portfolios over the coming year.

This document has been authorised for distribution to ‘wholesale clients’ and ‘professional investors’ (within the meaning of the Corporations Act 2001 (Cth)) in Australia only.

This document has been prepared by LGT Wealth Management Limited (ABN 50 005 311 937, AFS Licence No. 231127) (LGT Wealth Management). The information contained in this document is provided for information purposes only and is not intended to constitute, nor to be construed as, a solicitation or an offer to buy or sell any financial product. To the extent that advice is provided in this document, it is general advice only and has been prepared without taking into account your objectives, financial situation or needs (your ‘Personal Circumstances’). Before acting on any such general advice, LGT Wealth Management recommends that you obtain professional advice and consider the appropriateness of the advice having regard to your Personal Circumstances. If the advice relates to the acquisition, or possible acquisition of a financial product, you should obtain and consider a Product Disclosure Statement (PDS) or other disclosure document relating to the product before making any decision about whether to acquire the product.

Although the information and opinions contained in this document are based on sources we believe to be reliable, to the extent permitted by law, LGT Wealth Management and its associated entities do not warrant, represent or guarantee, expressly or impliedly, that the information contained in this document is accurate, complete, reliable or current. The information is subject to change without notice and we are under no obligation to update it. Past performance is not a reliable indicator of future performance. If you intend to rely on the information, you should independently verify and assess the accuracy and completeness and obtain professional advice regarding its suitability for your Personal Circumstances.

LGT Wealth Management, its associated entities, and any of its or their officers, employees and agents (LGT Wealth Management Group) may receive commissions and distribution fees relating to any financial products referred to in this document. The LGT Wealth Management Group may also hold, or have held, interests in any such financial products and may at any time make purchases or sales in them as principal or agent. The LGT Wealth Management Group may have, or may have had in the past, a relationship with the issuers of financial products referred to in this document. To the extent possible, the LGT Wealth Management Group accepts no liability for any loss or damage relating to any use or reliance on the information in this document.

Credit ratings contained in this report may be issued by credit rating agencies that are only authorised to provide credit ratings to persons classified as ‘wholesale clients’ under the Corporations Act 2001 (Cth) (Corporations Act). Accordingly, credit ratings in this report are not intended to be used or relied upon by persons who are classified as ‘retail clients’ under the Corporations Act. A credit rating expresses the opinion of the relevant credit rating agency on the relative ability of an entity to meet its financial commitments, in particular its debt obligations, and the likelihood of loss in the event of a default by that entity. There are various limitations associated with the use of credit ratings, for example, they do not directly address any risk other than credit risk, are based on information which may be unaudited, incomplete or misleading and are inherently forward-looking and include assumptions and predictions about future events. Credit ratings should not be considered statements of fact nor recommendations to buy, hold, or sell any financial product or make any other investment decisions. The information provided in this document comprises a restatement, summary or extract of one or more research reports prepared by LGT Wealth Management’s third-party research providers or their related bodies corporate (Third-Party Research Reports). Where a restatement, summary or extract of a Third-Party Research Report has been included in this document that is attributable to a specific third-party research provider, the name of the relevant third-party research provider and details of their Third-Party Research Report have been referenced alongside the relevant restatement, summary or extract used by LGT Wealth Management in this document. Please contact your LGT Wealth Management investment adviser if you would like a copy of the relevant Third-Party Research Report.

A reference to Barrenjoey means Barrenjoey Markets Pty Limited or a related body corporate. A reference to Barclays means Barclays Bank PLC or a related body corporate.

Evergreen funds are becoming a key building block in private markets portfolios because they offer inbound liquidity, faster deployment, and simpler portfolio management than traditional closed-end funds. While closed-end funds still have an important role, especially for more targeted...

CIO monthly

War, what is it good for?

May's CIO Monthly examines the US-Iran conflict, geopolitical risk, oil market disruption, Strait of Hormuz uncertainty, global market volatility, equity markets, fixed income, cross-asset correlations, regional divergence, alternative assets, diversification, liquidity, and long-term investor...

CIO monthly

When coming second makes sense

Secondary investments (secondaries) have moved from niche to mainstream and are now a regular feature in our client conversations. What started as a specialist tool used mainly by large institutions has become a core way of putting capital to work, generating liquidity and reshaping private...

Stay up to date

Receive ongoing access to LGT Wealth Management’s insights and observations - a curated stream of thought leadership, market perspectives, and strategic updates designed to inform sophisticated investors.