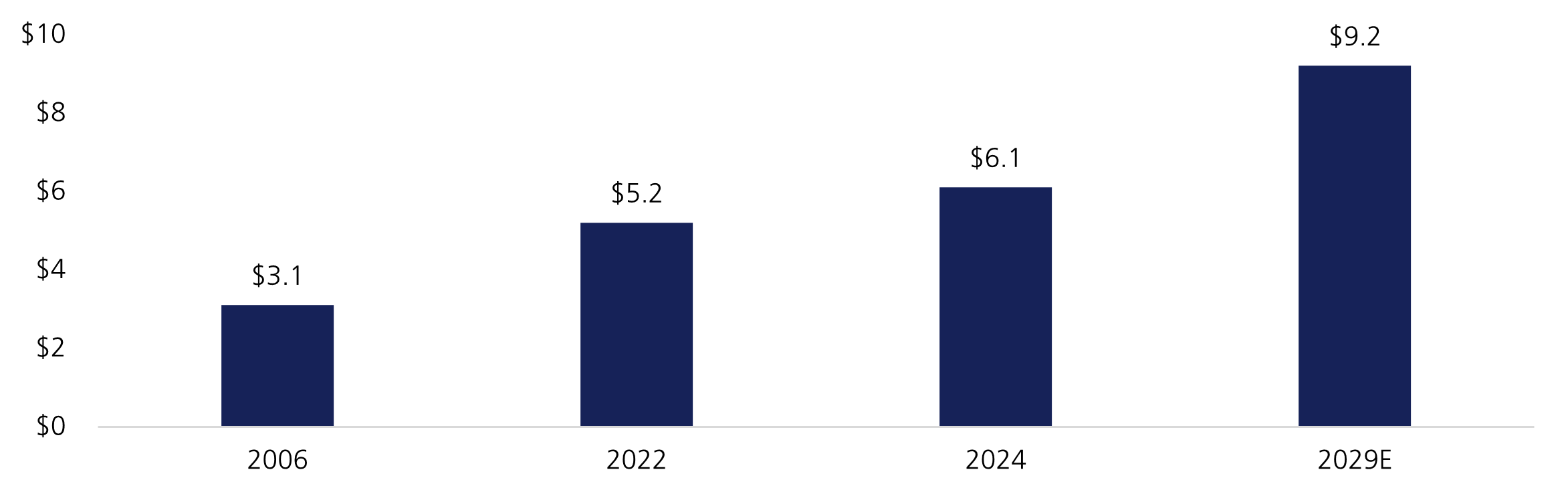

Asset-based finance (ABF) is emerging as one of the most compelling investment opportunities in private credit today. While direct lending has dominated institutional allocations over the past decade, ABF – the practice of extending credit secured against diversified pools of financial or hard assets – now represents a market exceeding $5 trillion globally and is projected to surpass $10 trillion by the end of the decade. Despite this, private capital accounts for only approximately 5% of the investable ABF universe representing a structural multi-trillion-dollar deployment opportunity set for experienced asset managers.

Asset-based finance now represents a market exceeding USD $5 trillion globally and is projected to surpass USD $10 trillion by the end of the decade.

At its core, ABF is a form of credit investing where each investment is backed by large, diversified pools of assets: financial assets such as consumer instalment loans, small business financing, or hard assets such as aircraft leasing, industrial equipment leasing, residential mortgage and commercial mortgages. Many describe this practice as financing Main Street (the real economy) whereas more traditional direct lending tends to be associated with financing Wall Street (corporations).

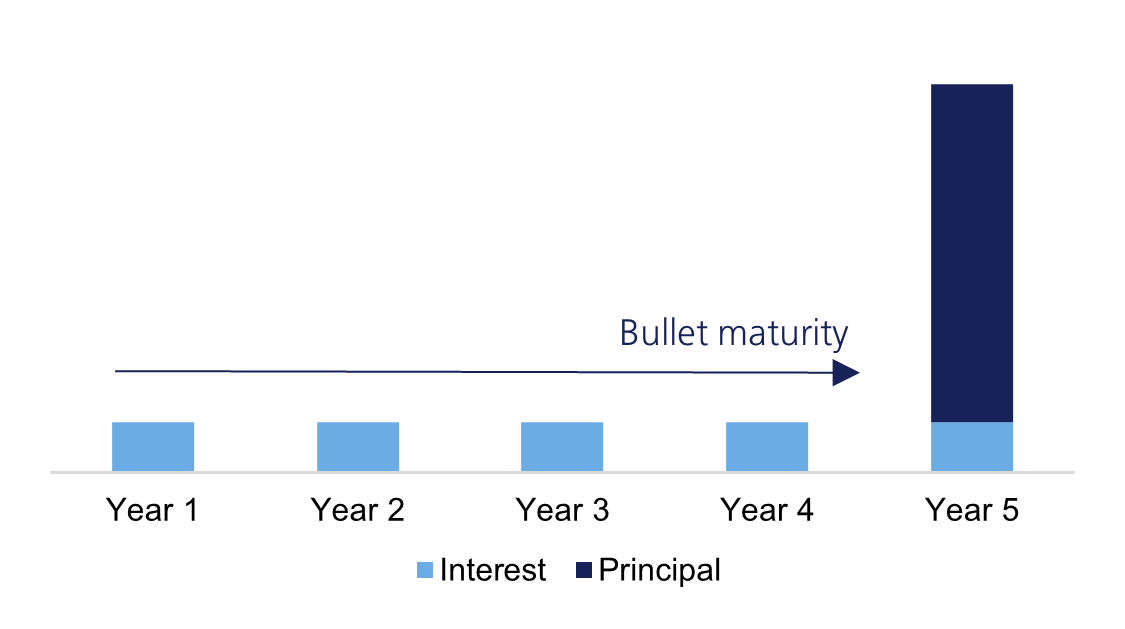

The key difference between corporate direct lending and ABF lies in the profile of the loans and repayment sources. In direct lending, the lender underwrites an individual company’s ability to generate future operating cash flows sufficient to service the interest and repay principal via a single or bullet maturity at the end of a five to seven year term. In ABF, repayments flow from the underlying asset pool itself – the contractual cash flows generated by thousands of individual mortgages, auto loan payments, lease receivables, or equipment rental streams.

| Feature | Direct lending | Asset-based finance |

| Credit risk | Enterprise / corporate risk | Asset-level / pool performance risk |

| Collateral | Enterprise assets | Segregated financial or hard assets |

| Repayment source | Company operating cash flows | Asset pool collections / contractual cashflows |

| Typical tenor | 5-7 years | 1–3 years (revolving/amortising) |

| Loan pricing | Predominantly floating rate | Predominantly fixed rate |

| Amortisation | Bullet or minimal amortisation | Self-amortising with underlying pool |

| Covenants | Leverage, coverage, capex, dividends | Delinquency, loss rate, concentration |

| Obligor count | Single / concentrated | 100s–1,000s (diversified pool) |

| Duration risk | Moderate-high | Low–moderate |

| Market stage | Mature, competitive | Growing, less crowded |

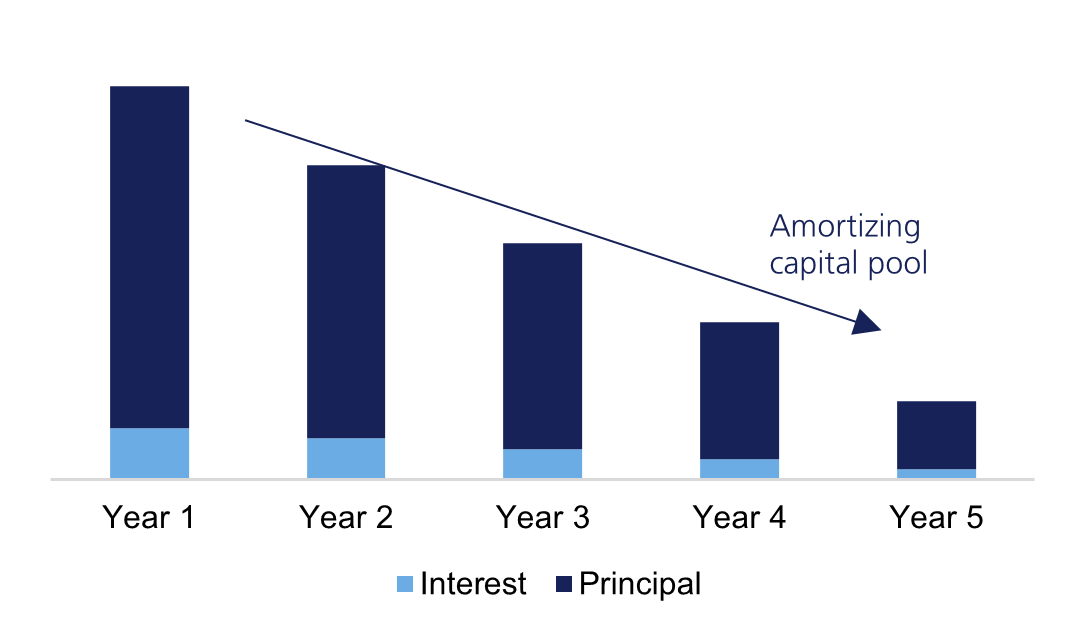

The critical structural feature of ABF investments is the self-amortising nature of the pools of assets. Every payment will be a combination of principal and interest, as with a typical mortgage payment, over the life of the pool. This is very different to direct lending, where the entire principal amount will only be returned as a lump sum upon maturity of the loan. The amortising profile of ABF investments inherently reduces the risk as positions age, resulting in a naturally lower credit duration or sensitivity for ABF portfolios relative to direct lending. Additionally, many ABF transactions are fixed rate, providing investors with greater cash flow certainty compared to floating rate direct lending.

The amortising profile of ABF investments reduces risk as positions age, resulting in a naturally lower credit duration or sensitivity for ABF portfolios relative to direct lending.

ABF spans a wide continuum of underlying asset types, each with a diverse set of risk drivers, return profiles and macro sensitivities. The specialist nature of many non-bank origination platforms has opened many new industries to ABF investors, allowing them to benefit from greater sector and industry diversification as a result.

Consumer finance | Consumer finance covers pools of credit extended directly to individuals, including personal instalment loans, point-of-sale financing, credit cards, and auto loans – all generating predictable, contractual cash flows from large, diversified borrower pools. Examples include a forward-flow portfolio of prime consumer instalment loans originated by a fintech lender receiving monthly principal and interest payments from tens of thousands of individual borrowers. |

Small business finance | Small business finance encompasses credit facilities extended to small to medium enterprises (SMEs), including term loans, revenue-based financing arrangements, merchant cash advances, and invoice/trade receivable facilities secured against business income streams. |

Fund finance | Net asset value (NAV) lending extends senior credit facilities to private equity or private credit fund managers, secured against the aggregated net asset value of a fund's underlying portfolio rather than any single asset. A practical example is a non-bank lender providing a $500 million NAV facility to a mid-market buyout fund — secured against a diversified portfolio of 15–20 private equity (PE)-backed companies — allowing the fund manager or general partner (GP) to manage liquidity, fund follow-on investments, or accelerate distributions to investors or limited partners (LPs) without forced asset sales. |

Equipment leasing | Equipment leasing finances the acquisition of mission-critical industrial, medical, or technology assets — such as manufacturing machinery, MRI scanners, data centre servers, or agricultural equipment — via lease structures where the equipment itself serves as hard collateral with tangible residual value. A practical example is financing to a hospital network against its fleet of diagnostic imaging equipment under a long-term fixed monthly payment agreement, with the equipment's replacement cost providing downside collateral protection. |

Aviation | Aviation ABF involves financing the purchase or leasing of commercial aircraft and cargo freighters — tangible, globally mobile assets with deep secondary markets — typically via operating lease structures where airlines pay fixed lease rentals to the asset owner over a contracted term. |

Residential finance | Residential finance encompasses mortgage lending and alternative residential credit products secured against the value of owner-occupied or investment real property, including conventional mortgages, non-QM (non-qualifying) loans for creditworthy borrowers outside agency guidelines, and innovative products such as home price appreciation (HPA) shares that allow homeowners to monetise equity without taking on additional debt. |

Commercial real estate finance | Commercial mortgage-backed securities (CMBS) structures pool commercial real estate mortgages — secured against income-producing assets such as office towers, logistics warehouses, multifamily apartment buildings, hotels, and retail centres — into bankruptcy-remote vehicles. Tranched notes are then issued to investors with subordination and excess spread providing structural credit enhancement to senior classes. |

Estimates vary widely on the total addressable market size of ABF depending on what asset categorisations investors use; some suggest it could be as large as AUD $20 trillion today. However, one thing all estimates agree on is the growing nature of this opportunity set. Despite this, and the attractive structural dynamics of ABF as an asset class, some suggest private capital accounts for only ~5% of the investable universe today.

The past and ongoing rise of ABF as an institutional asset class however has not been incidental; it has been the direct result of structural changes to the banking system triggered by the 2008 Global Financial Crisis (GFC). The regulatory response was comprehensive: the Dodd-Frank Act of 2010 imposed compulsory stress testing and capital planning requirements on large US banks, while the Basel III framework mandated higher risk-weighted capital ratios across the system and continued tightening against securitised exposures. The result has been a significant retrenchment from specialty lending, consumer finance and asset-backed activities. The number of US commercial banks has halved since 2000. Regional banks have become structurally challenged from the higher regulatory costs and capital drag associated with lending to consumers, small businesses and real estate.

Insurance companies, specialty finance platforms, and increasingly asset managers are stepping into this void. Non-bank lenders offer greater flexibility in this context as they are not subject to the same capital requirements as deposit-taking institutions. They can price risk more flexibly and they can provide bespoke financial solutions that banks and public markets cannot efficiently accommodate. They also benefit from longer-term and more patient sources of capital. This dynamic continues to open up new opportunities for private capital across a number of asset-based markets.

At the same time, demand for credit continues to increase across mortgages, auto loans, consumer credit as well as small business financing and equipment leasing. US household debt surpassed USD $18 trillion in 2024, up from USD $8 trillion in 2004. Fintech platforms, marketplace lenders and data-rich specialty finance origination platforms are well placed to step in to provide many forms of credit across financial asset and hard asset categories. Recent periods of credit stress within the banking system such as the collapse of Silicon Valley Bank and the 2023 US regional banking crisis have provided a catalyst for further market share growth of the non-banking sector.

ABF investments are structured with meaningful credit enhancement, including equity buffers, that must be exhausted before any senior or mezzanine investors experience a principal loss. The highly predictable, high cash-yielding profiles of ABF investments provide an additional structural benefit to investors. Given the majority fixed-rate structure of many ABF assets, this can act as a natural complement to a floating rate direct lending portfolio for clients looking for additional diversification. Additionally, the short average lives (typically one to five years) and rapid amortisations structurally limit the interest rate duration sensitivity of most ABF portfolios, reducing market beta risk.

Critically, ABF is fundamentally a non-corporate credit exposure, with returns driven by asset-level performance – consumer payment behaviour, collateral values, delinquency and recovery rates – rather than by corporate earnings or leveraged buyout (LBO) refinancing risks. This results in typically lower correlations to other forms of credit (depicted below), and by extension, equity, which collectively, can help improve total portfolio efficiency.

Pairwise correlations of Asset-based finance to alternative credit sectors

| US direct lending | EU direct lending | Junior debt | Capital solutions | Distressed | Asia credit | CLO equity | Asset based finance |

US direct lending | 1.00 | 0.93 | 0.94 | 0.91 | 0.83 | 0.76 | 0.79 | 0.42 |

EU direct lending | 0.93 | 1.00 | 0.84 | 0.86 | 0.69 | 0.76 | 0.74 | 0.44 |

Junior debt | 0.94 | 0.84 | 1.00 | 0.92 | 0.90 | 0.78 | 0.82 | 0.49 |

Capital solutions | 0.91 | 0.86 | 0.92 | 1.00 | 0.85 | 0.83 | 0.75 | 0.54 |

Distressed | 0.83 | 0.69 | 0.90 | 0.85 | 1.00 | 0.65 | 0.75 | 0.36 |

Asia credit | 0.76 | 0.76 | 0.78 | 0.83 | 0.65 | 1.00 | 0.55 | 0.69 |

CLO equity | 0.79 | 0.74 | 0.82 | 0.75 | 0.75 | 0.55 | 1.00 | 0.32 |

Asset-based finance | 0.42 | 0.44 | 0.49 | 0.54 | 0.36 | 0.69 | 0.32 | 1.00 |

The ABF market of today bears little structural resemblance to the pre-GFC era that became synonymous with opaque, over-leveraged securitisation. The failures of 2007-09 were categorised by synthetic collateralised debt obligation (CDO) structures that layered leverage upon leverage with no real asset backing, near-zero documentation mortgage underwriting, and rating agency conflicts of interest that assigned investment-grade ratings to deeply subordinated paper.

Under Dodd-Frank risk retention regulations, originators are now required to retain a meaningful economic interest in what they sell, directly aligning their incentives with investors. Underwriting standards across residential, auto, and consumer lending have also tightened materially, with loan-to-value ratios and documentation requirements all more conservative than pre-crisis norms. Leverage within securitisation structures is substantially lower; and the growth of data analytics means that institutional ABF managers today can monitor pool-level performance (e.g. delinquency rates, prepayment speeds and loss severities) in real time. Today's private ABF market is built on direct relationships between specialist lenders and originators, with bespoke structures, negotiated representations and warranties, and ongoing servicer oversight. This is a far cry from the anonymous, commoditised, ratings-arbitrage driven securitisation machine of the mid-2000s.

Asset management’s role in ABF lending remains relatively nascent. As such, it is imperative that investors partner with those that have a demonstratable track record of protecting investors’ capital and producing strong outcomes through multiple cycles. Key to this is deep expertise across origination, structuring and portfolio construction, and a deep bench of expert talent to execute across all of these core areas. Asset-based finance contains some of the most data rich sectors of the economy – data on consumer trends, employment and individual credit quality date back well over 50 years in some instances.

Key to unlocking the insights from this is best-in-class data science resources, likely built in-house with hundreds of thousands, if not millions of data points. This allows managers to demonstrate a strong relative value approach to capital allocation and portfolio construction. Equally important is the quality and exclusivity of originator relationships – the best managers have spent years building proprietary deal flow through captive platforms and forward-flow partnerships that are simply not available to new market entrants. Alongside this, rigorous originator alignment — ensuring those closest to the underlying borrower pool retain meaningful skin in the game — and robust servicer oversight capabilities are hallmarks of managers who have genuinely institutionalised their ABF practice. Finally, disciplined portfolio construction across sub-sectors, geographies and vintage years is critical to ensure the portfolio is resilient to any single macro stress event.

Receive ongoing access to LGT Wealth Management’s insights and observations - a curated stream of thought leadership, market perspectives, and strategic updates designed to inform sophisticated investors.