Institutional investors have long been enamoured with infrastructure as an asset class. Resilient business models with competitive moats and monopoly-like market positions have meant that investors can benefit from these assets’ stable cashflows.

Like other asset classes, infrastructure has been a beneficiary of a low interest rate and low inflation environment. Pre-pandemic, investors turned to infrastructure as an alternative, given the relatively low returns offered by cash and traditional fixed income. But as interest rates rise, inflation increases, and we enter a period of increased geo-political risk, what does the future hold for infrastructure?

In this Observations piece, we examine the benefits of investing in infrastructure, the role it plays in investment portfolios, and whether higher interest rates are expected to impact valuations.

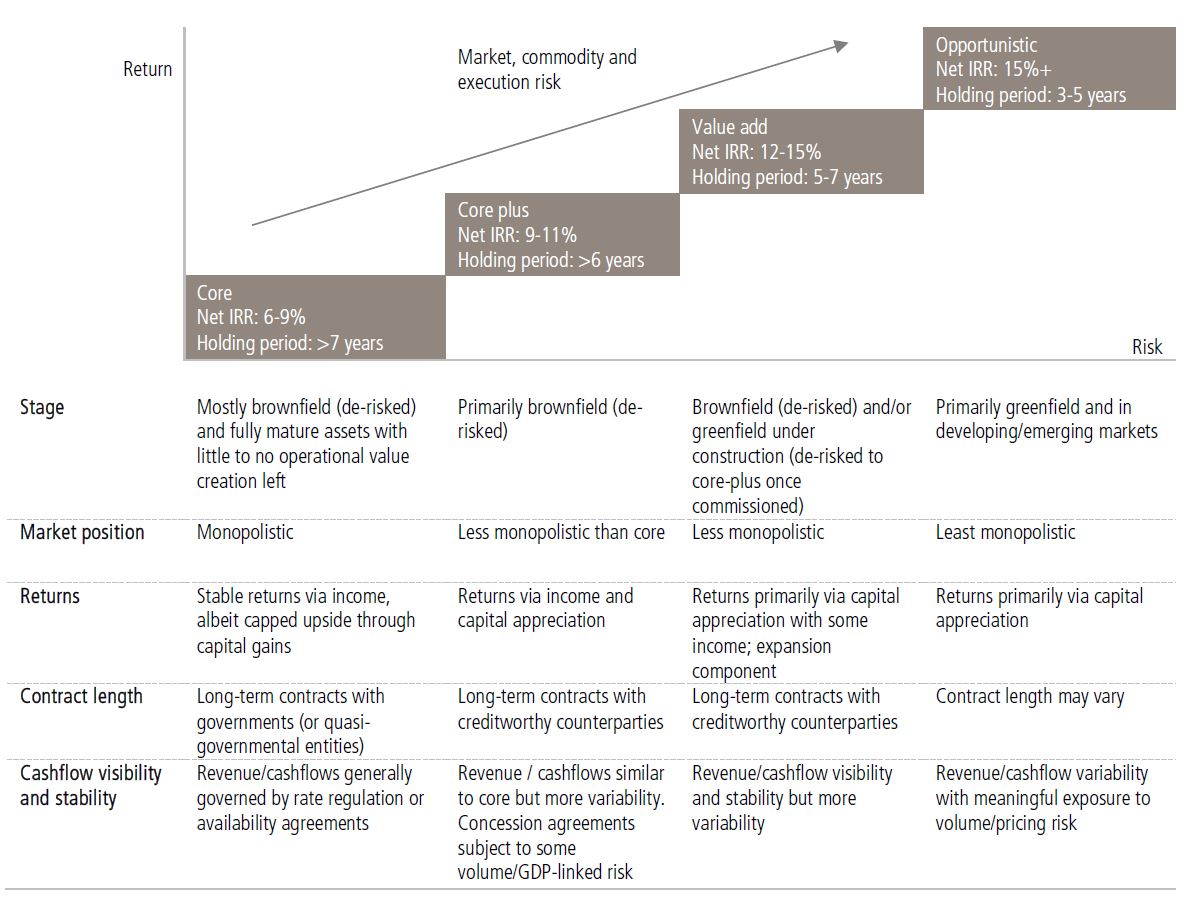

Core infrastructure assets include essential services, such as airports, seaports, and toll roads, power generation plants and networks, water and waste management works, and gas distribution networks. They generally hold monopolistic positions in the industries they operate, and benefit from long-term contracts with utilities, corporates or governments, therefore providing very stable cash flows.

Core-plus infrastructure assets have a slightly higher risk and return profile than core infrastructure. They typically provide an opportunity to add value from an operational or growth perspective, given their revenue linkages to GDP growth and higher exposure to market prices.

Value-add and opportunistic infrastructure assets have a risk-return profile that is more akin to traditional private equity. These assets are typically less mature and benefit from significant development, operational improvements, restructuring or market positioning.

Core infrastructure assets hold monopolistic positions in the industries they operate, and benefit from long-term contracts with utilities corporates, or governments.

Due to the monopolistic-like qualities of these assets, prices tend to remain relatively stable through the cycle. And because of their long-term contracts with credible counterparties (as well as operating in transparent regulatory environments), their cash flows are generally highly predictable. This makes infrastructure a compelling addition to a diversified portfolio. Infrastructure also provides diversification benefits, as returns are generally uncorrelated with equity investments. By investing in unlisted infrastructure, an investor can diversify their portfolio across asset types (energy, transport, water, and utilities), development stages (mature or growth), regulatory frameworks (uncontracted, contracted, or regulated), and geographic regions.

The key risks associated with infrastructure assets include political and regulatory risk, development risk, operational risk and leverage. Additionally, each core infrastructure sector has unique risk factors, highlighting the importance of diversifying across core strategies to reduce volatility.

Looking forward, infrastructure is expected to benefit from significant tailwinds, including rising investor demand and an undersupply of investable assets.

Globally, there is a need for more investment in infrastructure. Much of this is driven by structural themes, such as decarbonisation, digitisation, urbanisation, inter-connectivity, and an ageing demographic. This demand is evidenced by various policies and programs implemented by governments globally:

With government balance sheets currently constrained, there is a limit to how much this demand can be met by governments alone. According to KKR, between now and 2040, an additional USD 15 trillion will need to be invested in infrastructure globally, over and above what governments are expected to spend.

Australian and Canadian pension funds are considered to be leaders in infrastructure investing, with a typical asset allocation ranging from 8-15% at a total portfolio level. However, investors globally are generally under-allocated to the asset class. In 2023, Campbell Lutyens surveyed over 130 investors globally across foundations and endowments, public and private pension funds and found that 48% of respondents were under-allocated to infrastructure relative to their strategic asset allocations. The same survey found that 57% of respondents were looking to increase their infrastructure allocations in the future.

As infrastructure has grown and matured as an asset class, increased interest in the asset class has led to the emergence of a secondary market in infrastructure funds and co-investments. According to Partners Group, from 2016 to 2024, the secondary market has grown six-fold from ~USD 2 billion to USD 12 billion. This reflects a growth in primary infrastructure funds, as well as institutional investors increasingly using secondary markets to manage investment portfolios.

Not only do secondary markets provide investors with earlier distributions compared to the closed-end fund structures that are typically found in infrastructure, but they also provide a means to further diversify exposure to the asset class. Partners Group has identified secondaries in mid-market infrastructure ($500 million to $5 billion) as the most attractive area to invest. This is because this area has the highest amount of infrastructure funds by assets under management but receives the least amount of interest from institutional and secondaries' investors.

Infrastructure investments are a compelling addition to a diversified portfolio, given their ability to provide stable returns through the market cycle.

Over the past 30 years, infrastructure assets have provided investors with attractive risk-adjusted returns and strong and stable income. This has largely been driven by an extended period of low interest rates and low inflation. Although central banks have been increasing interest rates over the past two to three years, the overall performance of infrastructure has held up relatively well. Infrastructure valuers tend to take a long-term view on interest rates due to the assets' longer-term cashflows (which means that interest rate volatility has had less of an impact on valuations compared to other asset classes, such as real estate). Additionally, the negative impact of rising interest rates and higher discount rates has been offset by the positive impact of rising revenues from cashflows that are linked to growth and/or inflation (e.g., toll roads, airports, and utilities). Indeed, recent headline-grabbing infrastructure deals have been among the largest corporate transactions in Australian history -namely, Airtrunk in 2024 (AUD 22 billion), Sydney Airport in 2022 (AUD 32 billion), as well as some smaller deals for minority stakes in Queensland Airports Limited and Perth Airport.

Looking forward, infrastructure is expected to benefit from significant tailwinds, including rising investor demand and an undersupply of investable assets.

Given the long-term nature of the asset class, we believe that an allocation to infrastructure should be considered over a timeframe of decades rather than years. While we don't advocate a 'set-and-forget' approach, we do believe investors can make an allocation to infrastructure, which is independent of market cycles.

Due to the essential nature of infrastructure assets, we believe it is important to diversify broadly across sub-asset classes. During the COVID pandemic, airports (a segment within the transport sub-asset class) performed poorly, as the grounding of planes meant that these assets stopped generating aeronautical income, as well as ancillary income from retail and car parking. On the other hand, seaports (another segment within transport) performed extremely well as volumes in this industry expanded.

When building a portfolio of infrastructure assets, we recommend creating a foundation of core/core- plus assets, then supplementing this with core-plus and value-add exposures that are appropriate for the investor's risk profile. This should ensure that the balance of overall returns is skewed more towards capital growth than income, and that the overall portfolio leans towards a core-plus profile. A core-plus profile is helpful as it means portfolios should benefit from exposure to structural themes, such as decarbonisation, urbanisation, and digitisation. They should also have a higher exposure to smaller assets, which are generally more liquid. This approach is also important from an after-tax perspective, given infrastructure assets' long investment timeframes.

We advocate the use of open-ended (either perpetual or evergreen) infrastructure funds alongside traditional closed-end fund structures that are favoured by institutional investors. However, we also recognise that in some instances, a closed-end fund structure may be the only vehicle available to access certain investments, particularly in value-add and opportunistic segments.

As long-term asset owners, infrastructure investors should not be blind to the future impact of climate change on individual assets, as well as the impact of changes in government policies.

Given the long-term and essential nature of infrastructure assets, along with regulatory and counterparty risks, it is important that investors take a long-term view and ensure the assets are being managed prudently and in a sustainable way. There are three key areas that we believe investors should consider:

As long-term asset owners, infrastructure investors should not be blind to the future impact of climate change on individual assets, as well as the impact of changes in government policies. Climate change risks are generally classified as either 'physical' or 'transition' risks:

To mitigate these risks, investors should carefully assess the resilience of infrastructure assets, consider climate adaptation measures, and invest in low-carbon and climate-resilient infrastructure.

Although infrastructure has traditionally been the domain of institutional investors, it can also play an important role in private wealth portfolios, given its diversifying characteristics, as well as its ability to provide inflation protection and relatively stable returns.

Receive ongoing access to LGT Wealth Management’s insights and observations - a curated stream of thought leadership, market perspectives, and strategic updates designed to inform sophisticated investors.