The latest observation by Kaajal Prasad, Head of Family Advisory at LGT Wealth Management Australia, explores the implications of the 2026 Federal Budget for family groups.

As the dust settles on the 2026 Federal Budget, many family groups are concerned about the impact of the tax-related Budget announcements on their corporate structures. In combination with the recent ‘Division 296’ changes to superannuation legislation, these tax-related Budget changes have cause panic for investors.

For high net wealth families, the opportunity now is to look through the immediate tax noise and focus on long-term wealth preservation, structuring and intergenerational objectives.

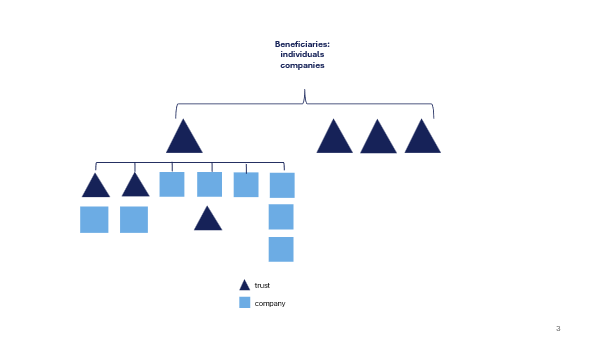

High net wealth families and private groups in Australia have organisational structures that consist predominantly of private companies, discretionary trusts (including family trusts and testamentary trusts), and self-managed superannuation funds. The make up of these structures and the purpose and use of each entity largely reflect the tax landscape that prevailed up until Budget night.

Typical family structure diagram

Alarmist post-Budget commentary suggests that the use of this structure, and discretionary trusts in particular, should be phased out, seemingly to make the tax system fairer for more Australians. However, we are of the view that, particularly for high net wealth families, the underlying strategic and multi-generational aspects of these structures remain largely intact.

Investors now have a real opportunity to think strategically about the structuring of their wealth. Rather than taking a knee-jerk reaction to the tax changes, this is the time to act strategically and thoughtfully. But acting doesn’t necessarily mean making wholesale changes to the fundamental basis of a group structure.

If a family ‘pulls money out of super’, vests its trust, or winds up its company to achieve a certain tax outcome, that tax outcome, as we have seen in this Budget, can be later precluded. Tax, in isolation, is very rarely the reason to do (or not do) something. Investors are therefore encouraged to look beyond the siloed aspects of managing family wealth and instead focus on the purpose of that wealth and the role the family plays in achieving that purpose.

In the case of many family groups, wholesale action is not needed. This Budget and its fundamental changes to the tax landscape give a good excuse to reflect, reset and refocus and ask the following questions:

Does our asset mix and entity structure enable us to fulfil our purpose?

What do we need to change in order to optimise our wealth map for future generations?

How do we ensure that we are properly set up for the next phase of protection, preservation and growth of the family’s wealth portfolio?

Tax may be one consideration in answering these questions, but it certainly shouldn’t be the main consideration.

Succession planning should never be tax-led. Succession planning should be led by the family and its needs, wishes, and vision. The changes that the Budget introduces do not alter this approach. A tax approach encourages transactional, short-term behaviour and, while that may be necessary for specific assets or specific events within a family group, it will rarely provide the most optimal long-term outcome with future generations in mind.

Take, for example, a family with large business operations in Australia. The founders are aged in their 70s and thinking about succession.

Their holdings have expanded beyond the core family business and include property, investments and a share portfolio. All assets are ultimately held in a group of discretionary trusts.

This structure is typical of family group holdings. The Budget’s tax changes have raised concerns for this family about its ‘trusts at the top’ structure.

This is a critical time for the founders to obtain updated tax advice and undertake a broader strategic review in relation to their wealth. Beyond tax concerns, the founders wish to preserve their assets across the generations. Achieving a balance between this goal and tax efficiency will therefore be important.

While many of the tax advantages associated with trusts have now been removed or reduced under the Budget changes, discretionary trusts continue to provide the highest level of asset protection. For this high net wealth family, the long-term economic impact of the Budget changes may ultimately be relatively modest when considered against their broader objectives of preserving wealth for their children and grandchildren.

Any action in relation to changes to group structure and wealth planning will require the expertise of a range of specialists, including tax, legal, and estate planning practitioners. We encourage you to talk to your Investment Adviser and our Family Advisory team about the strategic aspects of your multi-generational wealth.

Receive ongoing access to LGT Wealth Management’s insights and observations - a curated stream of thought leadership, market perspectives, and strategic updates designed to inform sophisticated investors.