Hear the latest geo-political commentary from our investment team.

Market performance cannot wholly rest on the outcome of geopolitical events. In this month’s Core Offerings, having harvested the positive returns associated with a likely emerging US-Iran peace deal, we take the opportunity to further trim risk. The next three to six months are increasingly likely to be a more challenging environment for markets; there is a (macro) price to be paid for persistent elevated energy prices. Despite this, we are not in favour of underweight equity positions from a multi-year perspective, and continue to advocate a focus on building medium-term resilience into portfolios (both adapted to this multi-polar world and able to capture returns across key thematics).

In this month’s Core Offerings, we also take the opportunity to dig deeper into one of the asset classes that ticks many of the boxes for building such medium-term portfolio resilience, namely private markets. Yes, we’re aware that the idiom is an ‘open and shut’ case (not an ‘open and closed’ case, as we’ve titled it). But our play on words relates to open- and closed-end funds. We’ve regularly discussed the evolution and proliferation of these so-called evergreen funds, and the extent to which this innovation has significantly broadened exposure to private markets for private clients. But the increasing options across open (and more traditional closed-end) funds now raises the broader question of how a portfolio should balance the inclusion of both these types of structures.

Over the past month, equity markets have continued to focus on the improving prospects for progress in the US-Iran conflict, and in particular, the opening of the Strait of Hormuz. Without doubt, the constraints that should force a deal have been rising on both sides. For US President Trump, there is the issue of rising oil prices (and a mid-year inventory ‘crunch’ that will drive prices even higher), while for Tehran, the US naval blockade is crimping Iran’s revenues. In the background, risks of a softening economy in China are likely leading China’s President Xi to encourage Iran to the table, and quickly. The likelihood of a ‘peace deal’ that lifts passage through the Strait of Hormuz has risen (even if that deal lacks a longer-term resolution around Iran’s nuclear ambitions – a key sticking point for both sides).

Yet, market performance cannot wholly rest on the outcome of geopolitical events. Over the past month, our conviction that the next three to six months will be a more challenging environment for markets has also risen. There is a price to be paid for the persistence of elevated energy prices and its impact on the global supply chain. The macroeconomic backdrop remains constructive, albeit not to the extent we expected. Our forecast late 2026 demand-led inflation uplift is giving way to a supply shock induced mid-2026 inflation impulse. It is unlikely the global oil price will revert to USD 60 per barrel (p/b) any time soon. There is also increasing evidence current inflation pressures are threatening previously well-anchored inflation expectations. Central banks, still smarting from their lagged (or arguably late) response to post-COVID inflation, are no longer in the mood to hold or cut rates, but are poised to hold or hike.

Without doubt, our tactical positioning has benefited from the equity market’s positive response to the prospect of a peace deal (given our overweight equity stance) as well as the bond market’s increased concern about inflation (given our global bond underweight). Arguably, markets continue to follow the geopolitical playbook we have successfully implemented over the past two years. Still, the emerging ‘stagflation-lite’ environment in H2 2026 warrants some caution, even if only for a time. Equity valuations (after easing through March) have rapidly returned to being ‘rich’, central banks have turned more hawkish, bond yields have risen. While equity markets – post a peace deal rally – may continue to grind higher, there’s reason to expect an element of complacency may lead to choppier returns in both equities and fixed income markets. Moreover, a less buoyant backdrop may also prompt a drawdown that proves advantageous for renewed deployment ahead.

This month we take the opportunity to make some further moves to trim risk (as we did in April), returning cash from underweight to neutral. It’s also a time to ensure the recent strong equity market performance hasn’t rendered tactical equity positions in portfolios excessively above target.

Specifically – and as discussed further across pages 9 and 10 inside – we are moving from +2 to +1 equities (building on the move from +3 to +2 in April). We retain our preference for developed market equities (Japan and US) over emerging markets (where we are neutral) and domestic equities (where we are underweight). We no longer view Europe as preferred given the renewed energy headwinds and a central bank that is likely to lift interest rates from next month.

Despite this trimming of risk, we are not in favour of underweight equity positions on a one to two year perspective. But we believe a more neutral stance on a three to six month outlook is warranted, as is deploying more cautiously into a less than cheap market, while also retaining more cash on the sidelines than we did this time last year (where we were -2 relative to our now neutral stance). Globally, we remain mildly overweight equities relative to fixed income (and hold the opposite position for Australia, where recent hikes may slow the economy much more than expected).

Finally, we continue to advocate a focus on building medium-term resilience into portfolios. This should reflect the ‘common ground’ between two key drivers, namely adapting portfolios for a multi-polar secular outlook and harvesting returns in the bottle-neck thematics:

In this month’s Core Offerings, we take the opportunity to dig deeper into one of the asset classes that ticks many of the boxes for building medium-term portfolio resilience, namely private markets. Below, we examine how investors should navigate the balance between traditional closed-end unlisted alternative investments and the relatively new ‘evergreen’ or open-ended opportunities.

There are fundamental differences between the two investment structures. Yet – and in keeping up with the legal case rhetoric – it still often feels like the new evergreen contingent plays the role of the defendant, whilst the closed-end funds play the plaintiff. That is to say, that evergreen funds are often viewed negatively in certain circles, which we think misses their most compelling features. So, let’s start there and then take a look at their closed-end siblings.

A closed-end unlisted alternative fund structure has a fixed pool of capital for a set term. Investors usually commit money upfront, cannot freely redeem, and get capital back when assets are sold or the fund winds up. |

An open-ended unlisted alternative fund structure allows investors to enter and exit over time. The fund issues or redeems units based on investor flows, typically using periodic valuations and available liquidity. |

As we’ve repeated tirelessly over the past year or so, inbound liquidity remains the most important innovation and feature of the evergreen (or open-ended) fund. Put simply, this is the ability to deploy capital immediately (and into a diversified portfolio) and have it managed professionally on an ongoing basis. Contrary to popular opinion, outbound liquidity, or the ability to get funds back, is not the primary feature of the evergreen structure, and shouldn’t be wholly relied upon. This inbound liquidity feature is also the most fundamental difference of an evergreen fund relative to a closed-end fund, and it plays the most important role in portfolio construction.

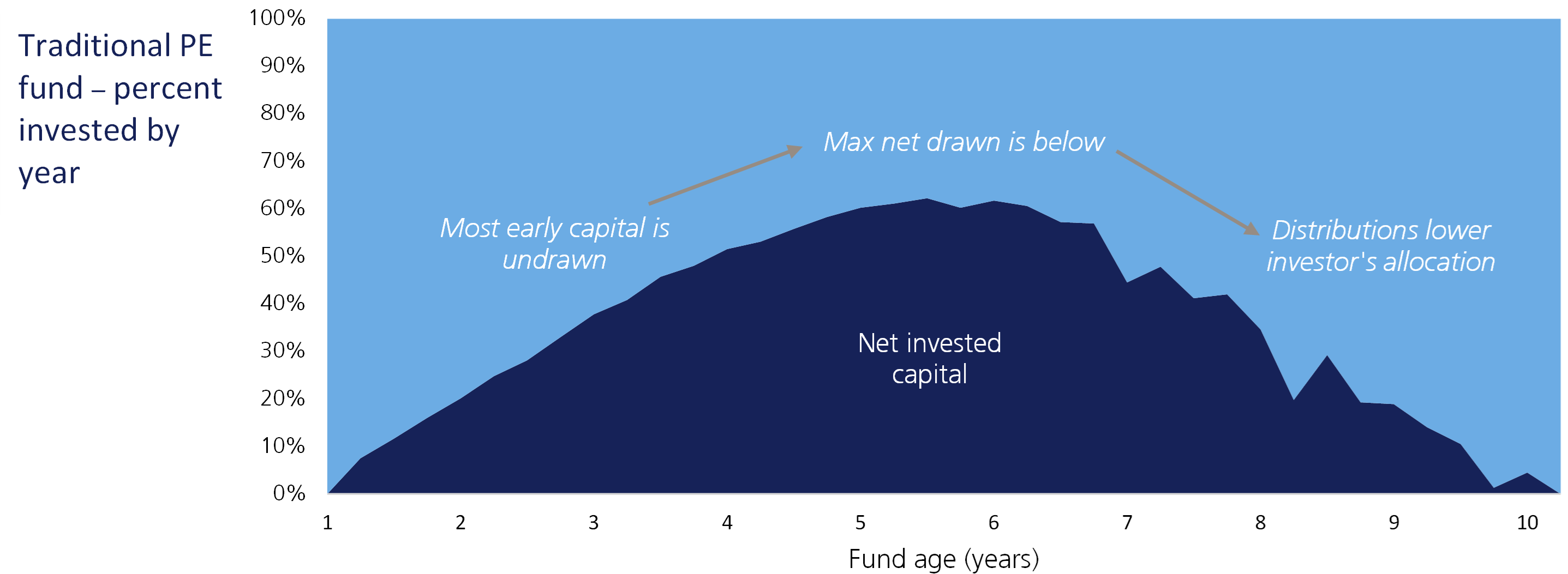

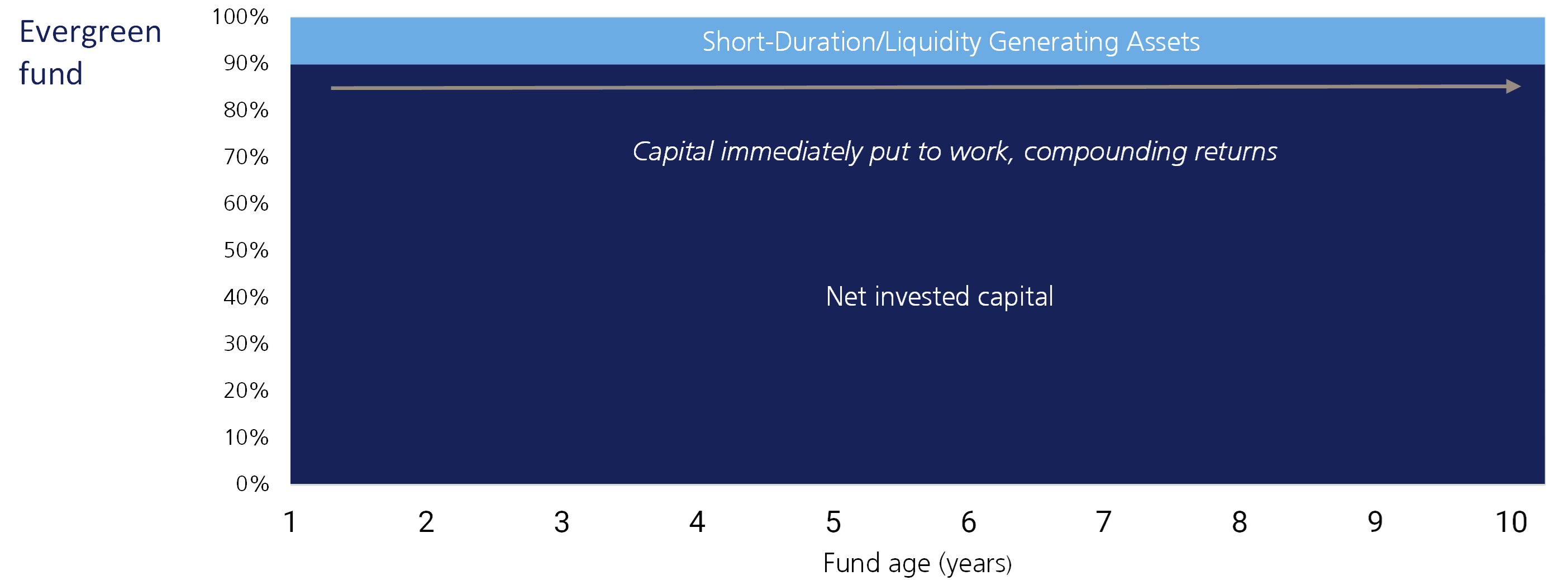

Figure 1: 10-year representative exposure of a traditional and evergreen private equity fund

Take a look at Figure 1, which depicts a 10-year representation of a traditional and then evergreen private equity fund. In the former, capital is drawn down over numerous years and gradually gets returned as underlying investments are realised. Whilst this is illustrative, net invested capital only reaches about 60% of the commitment or target (before distributions start to impact). In the case of the evergreen, around 90% is immediately invested in private assets.

Why is this so important? Well, it means that 90% (of target) is invested and compounding from day one, as opposed to zero in the case of a closed-end fund. In most cases, evergreen funds are already meaningfully diversified whether in the case of a multi-manager (allocator) offering or a single manager solution. They also seek to maintain that diversity and level of invested capital across each vintage year, which is of critical importance and leads nicely on to what it takes to build the equivalent (portfolio) on the closed-end side.

The drawdown profile of a closed-end fund depicted on the previous page shows that investors never actually reach their targeted exposure for a single fund position, and the same applies even if you include underlying asset growth. Practically, this means that to build a portfolio and actually reach the target portfolio weight, investors need to consistently allocate to new closed-end funds vintage (year) after vintage to grow and maintain exposures as distributions accelerate. At the outset of a program, investors also need to over-allocate (i.e. commit more than intended to invest) to expedite the journey towards the target portfolio weight.

This is only one complexity to navigate; we also need to consider what appropriate diversity looks like given closed-end funds are typically far more concentrated (by portfolio companies) than public market peers. There are also a lot of factors to consider when diversifying, whether they be geography, sector, market-cap, investment stage and even outright asset class (private equity, private debt, venture capital, real estate and infrastructure all use closed-end funds).

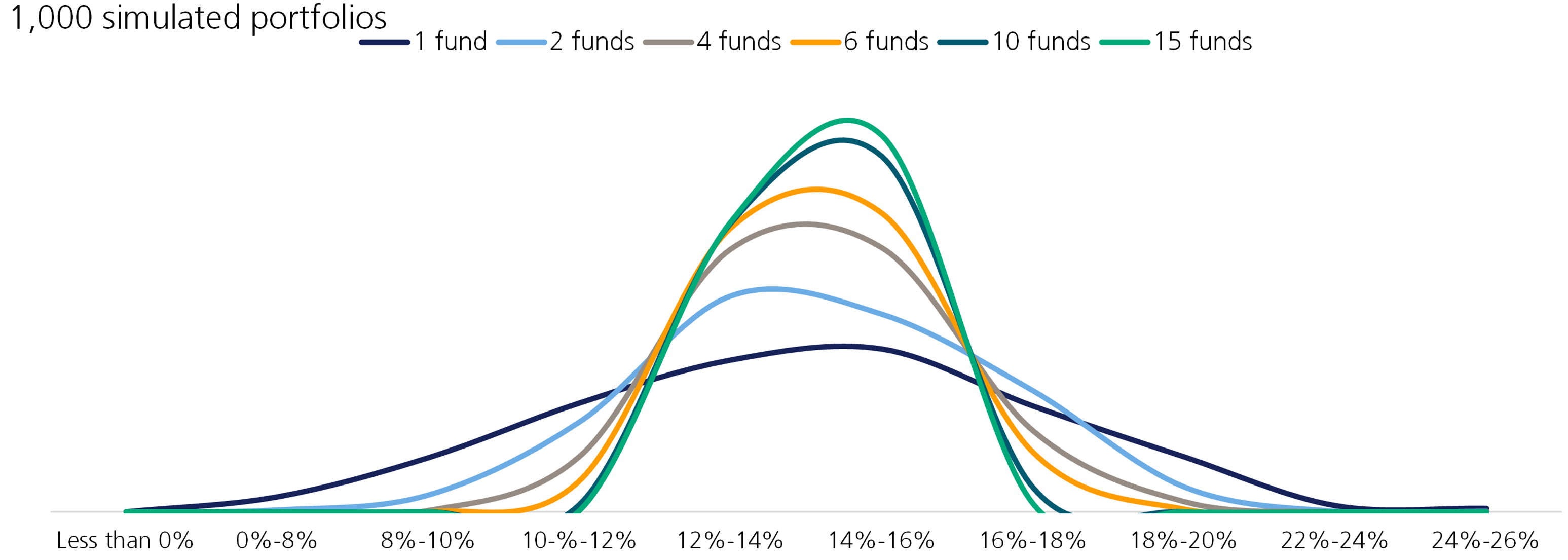

Figure 2 shows a normal distribution of returns by number of funds for a given vintage year. In essence, it’s showing that allocating to one or two funds in a given year can result in a higher likelihood of outsized returns on the right, but also a higher likelihood of weaker returns on the left. We call these ‘fat tails’. As an investor adds more funds, the probability of outcomes narrows, whilst also collectively edging to the right. We call this positive skew, and it is positive in this context. The key takeaway here is that diversifying across numerous funds each year is a sensible strategy and improves outcomes. Here’s the rub: this is particularly true in asset classes (such as private markets) where the dispersion of returns (and thus the risk of poor manager selection) is far greater compared to public equivalents (like listed equities and bonds).

Figure 2: Normal distribution of returns by number of primary funds (1,000 simulated portfolios)

Putting this all together, this practically implies that an appropriately diversified, closed-end fund private markets program requires investors to consider allocating to at least five to 10 new funds each and every year to maintain exposure, with an initial period of overallocation. Suffice to say, it’s not a simple task.

To first summarise, open-end funds enable immediate deployment and compounding and put the highly complex task of closed-end fund portfolio management back onto the fund manager(s). The argument for the clear-added complexity of a closed-end portfolio then typically comes back to the performance and the assertion that open-end performance lags closed-end. This argument often ignores the fact that performance calculations across the two vehicles are not strictly comparable, and this would warrant a separate paper comparing money-weighted (internal rate of return, IRR) and time-weighted return methodologies.

What we will say for now is that investors should focus as much on the multiple of invested capital as on either the IRR, or time-weighted return of a closed- or open-end solution respectively.

For those starting out on the private markets journey, whilst not the only route, we typically advocate that evergreen is the first port of call given the immediate allocation and compounding. The investment universe of options is growing, which helps in this regard. But there are some limitations, which we will discuss. There really is no right or wrong answer on the pathway towards (or an entire transition to) closed-end funds so we break down a number of considerations below.

The growth of evergreen funds, principally utilised by private clients, has been rapid. Pitchbook data (US market) suggests that net assets under management totalled USD 457 billion across 486 evergreen funds as at the end of 2025. Over half of these funds were launched in the last four years. When you look at the breakdown of these funds by asset class (below right), it’s clear that private debt (credit) has taken the lion’s share, which is in contrast to the institutional funds’ community (mostly closed-end), and is arguably more balanced with meaningful exposure to private equity and venture. Australia has been less lop-sided with early growth dominated by both global private equity and domestic private debt.

The point to make here is that we have a growing contingent of evergreen strategies across private equity, private debt, (late stage) venture capital/growth equity, real estate and infrastructure, from which we can build portfolios. The following lays out some portfolio construction considerations:

Private debt has most bases covered: With the exception of distressed and more niche credit strategies, evergreen solutions today enable investors to build well-diversified portfolios catering for geographies, company size and debt type. We advocate for investors building principal exposures across direct lending and asset-based finance sectors, with (private debt) secondaries able to play a core and highly diversifying role across sectors and managers.

Large firms and allocators provide the foundation for private equity: Allocators or those firms with hybrid direct/secondary offerings, play the core role in our view given the diversity they can offer across the market. Larger PE firms with multi-strategy platforms with ample deal flow can then be additive, noting that such solutions typically bias towards larger companies.

Further segmentation provides greater optionality: Regionally biased PE strategies have emerged, as has segmentation into pure-play secondaries and lower-middle market strategies which we feel will complement each other moving forward. Late-stage venture/growth options – critically through those with the right platforms – also warrant an allocation.

Single manager, single strategy offerings will likely be challenged: It will remain difficult to get specific with open-end funds as you typically need broad deal flow to make them work. Whilst some single strategy and/or smaller single manager solutions have emerged, there are structural challenges that need to be managed exceptionally to make them viable long term.

Infrastructure is emerging: While allocators and hybrid platforms are structurally advantaged in providing more core (diversified) solutions in our view, highly credible direct fund managers can be complementary and can be utilised accordingly.

A practical starting point for closed-end fund usage

So how does one take a view on a high conviction, capacity constrained, single strategy fund manager, or make a thematic bet on life sciences, or powering the energy and data demands of AI? Closed-end funds can serve this function as a starting point to move away from a pure evergreen portfolio.

We consider three broad categories albeit many strategies can cater for all three:

High conviction: Accessing those consistently top quartile, typically capacity-constrained managers can be used to enhance returns. Sizing still needs to be appropriate, but such managers can certainly be additive.

Thematic, tactical, cyclical: Themes, tactical positioning and cycles change, and thus so do investment views and the means to play them. Implementation options are often more concentrated and/or point in time and thus don’t have the depth to warrant an evergreen solution. Strategies such as life sciences, energy transition and AI-linked themes tend to be best played via closed-end funds.

Early-stage and/or shallow markets: Some strategies simply don’t work and/or are harder in an evergreen format. Early-stage venture capital does not work in an open-end format since valuing early-stage companies fairly (for both a buyer and a seller) is notoriously difficult. Some markets are also quite shallow and thus while not impossible, can be challenging to invest into in an open-end format.

Introducing select managers and funds across these strategies fleshes out the private markets investment universe and thus fills structural gaps that we expect to persist within the evergreen fund landscape. Utilising this starting point for closed-end funds, we would suggest that evergreen vehicles comprise at least 70% of a portfolio’s private markets exposure, and higher if the portfolio is biased more toward private debt and yield producing strategies.

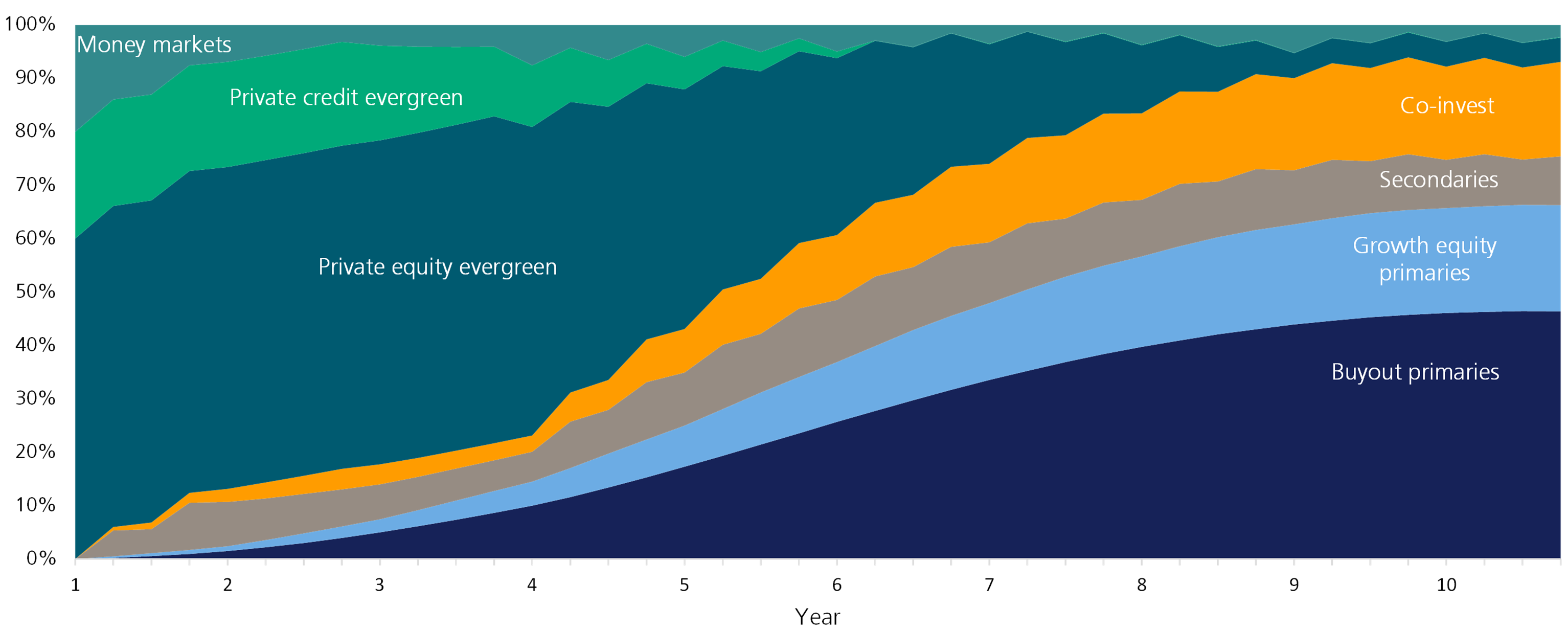

The below illustration provides an example hypothetical (full) transition from evergreen to a self-funding closed-end private equity portfolio over a period of 10 years. As previously noted, there is no right or wrong answer to how far one then shifts further towards closed-end fund portfolios but there are a number of practical considerations.

Figure 4: Portfolio value mix by portfolio age – example transition portfolio

As highlighted, building an appropriately diversified closed-end fund portfolio requires numerous new commitments each and every vintage year. To facilitate this, investors need to first be able to access sufficient high-quality managers and strategies across market segments. Ideally, this requires building a pipeline multiple years forward, or else a portfolio can become quite eclectic and often biased towards strategies that investors are shown (as opposed to those they intentionally pursued). A focus on co-investment and secondary strategies can help mitigate this requirement (i.e. reduce the volume of strategies) given the breadth that such strategies offer.

Whilst the secondary market is very mature within private equity in particular, the ability to use this market is more constrained within even sizeable private client portfolios. This is due to the fact that commitment sizes are typically smaller (than major institutional allocators) and thus less applicable for active secondary participants. This means that the ability to actively tailor, or generate genuine liquidity, from (closed end) portfolios through the secondary market is limited. A greater focus on portfolio level liquidity requirement is thus more critical as closed-end fund exposures grow.

As closed-end portfolios mature, one of the most complex components of portfolio management is to estimate cashflow profiles across a growing number of funds, including both cash needs (to meet capital calls) and cash returns (from distributions). Maintaining target portfolio weights, particularly as public asset classes shift around private, can be challenging.

For this reason, we would typically advocate maintaining a larger allocation to evergreen (than that depicted in the ‘closed end’ example) across private asset classes to provide more flexibility to adjust exposures over time. In our view, a minimum 30% exposure to evergreen strategies would be appropriate and – as noted in the prior section – more should the portfolio be biased toward private debt and yield producing strategies.

As a final point, appropriately priced margin lending facilities (credit) can play a very valuable role in both optimising portfolio management, and in improving administrative headaches when it comes to managing regular capital call requirements of more developed closed-end fund programs.

From an efficiency perspective, credit can be used to bridge cashflows when rebalancing illiquid assets into liquid assets. Evergreen structures, whilst not liquid in a traditional sense, have structured liquidity parameters that have broadly been able to meet redemption requests during normal market conditions, yet it can still take time to sell down these assets. Practically, during market dislocations or periods of meaningful cross-asset class dispersion, the ability to rebalance into public markets without having to wait for long notice or pricing periods can be extremely valuable.

From an administrative perspective, credit can be used to finance aggregate capital calls meaning that cashflows can be met as part of the portfolio’s typical review and rebalancing cadence (as opposed to ad-hoc per capital call). It also reduces the risk of defaulting on capital call obligations in the case of tight timing, external or portfolio cashflow delays or where unexpected approvals cannot be sought owing to absence.

Key Points

Inbound – not outbound – liquidity remains the most important innovation and feature of the evergreen fund, and is the main difference between these and closed-end funds.

An appropriately diversified, closed-end private markets program requires investors to consider allocating to at least five to 10 new funds each and every year to maintain exposure, with an initial period of overallocation.

Open-end funds enable immediate deployment and compounding, and put the highly complex task of closed-end fund portfolio management back onto the fund manager(s).

There is a place in optimal portfolios for both open- and closed-end funds, albeit noting that performance calculations across the two vehicles are not strictly comparable.

The growth of evergreen funds has been rapid; we have an expanding range of evergreen strategies across private equity, private debt, (late stage) venture capital/growth equity, real estate and infrastructure. These can provide the core of a diversified private markets allocation.

Closed-end funds have a clear role for targeted opportunities, but increasing exposures toward closed-end funds adds complexity around access, liquidity and cash-flow management, which needs to be considered.

We believe a minimum 30% exposure should be maintained for evergreen strategies to allow flexibility to adjust exposures through time. Moreover, that could be as high as 70% should the portfolio be biased toward private credit and yield producing strategies.

Credit can play a valuable role in both optimising portfolio management and improving administrative headaches.

Receive ongoing access to LGT Wealth Management’s insights and observations - a curated stream of thought leadership, market perspectives, and strategic updates designed to inform sophisticated investors.