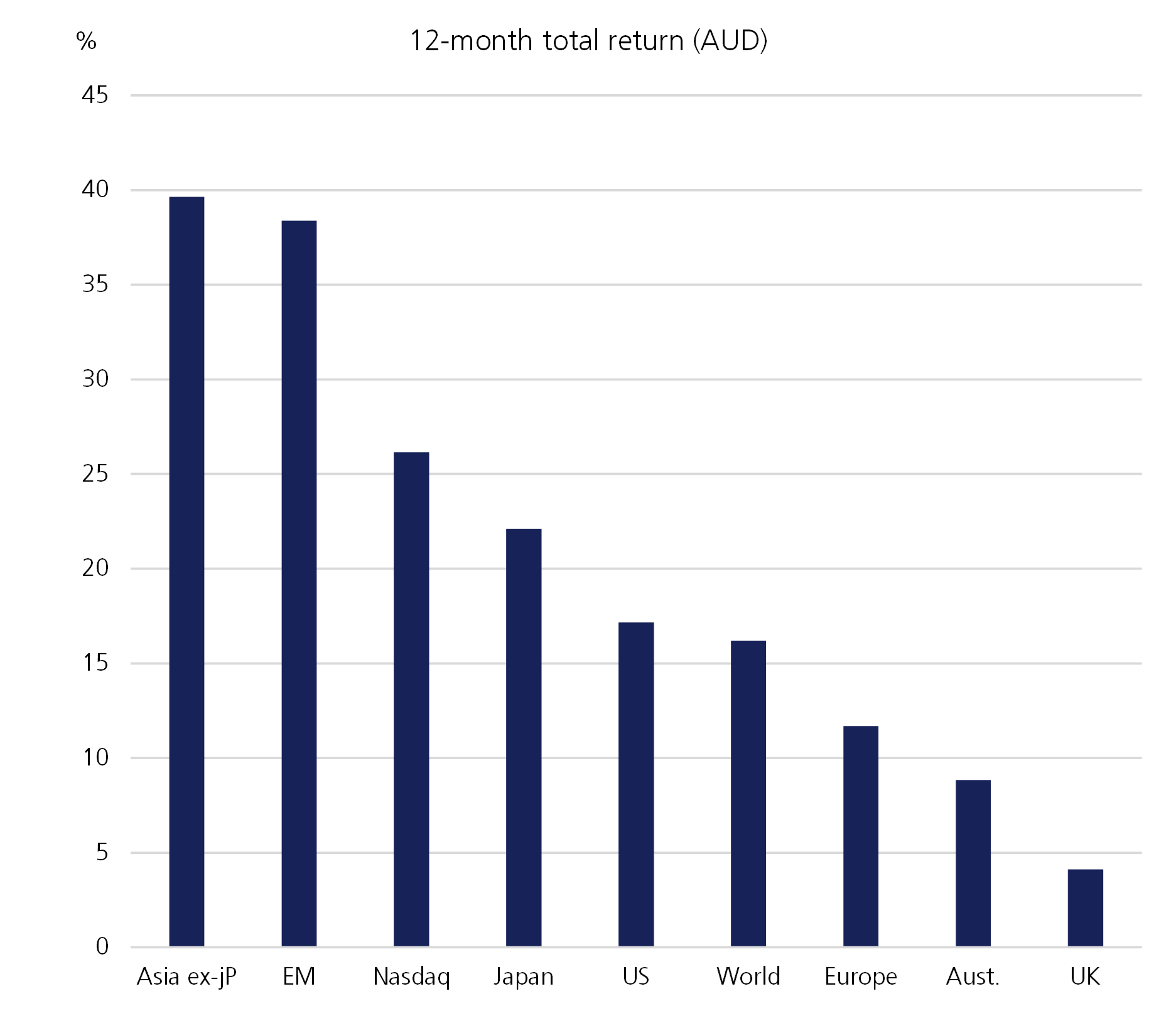

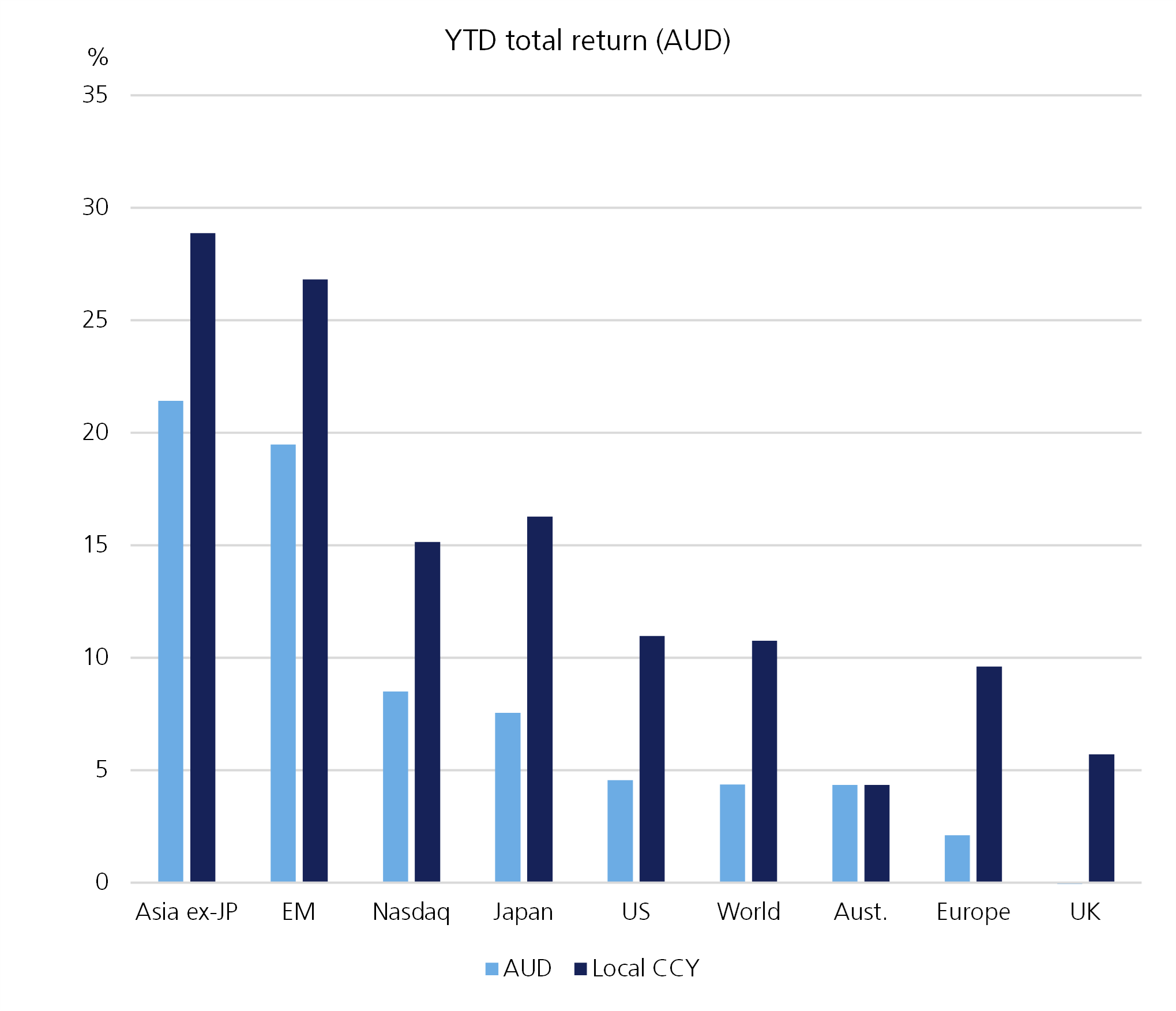

Although Australian equities have delivered an almost 10% total return over the past 12 months, this performance has materially lagged that of equity markets in major developed and emerging economies. In aggregate, Australian equities have underperformed global equities by more than five percentage points in Australian dollar (AUD) terms. However, even this significantly understates the underperformance, which has been significantly masked by the appreciation of the AUD. In US dollar (USD) terms, global equities are up 25% over the past 12 months. Year-to-date (YTD) performance for Australia is also similarly weak.

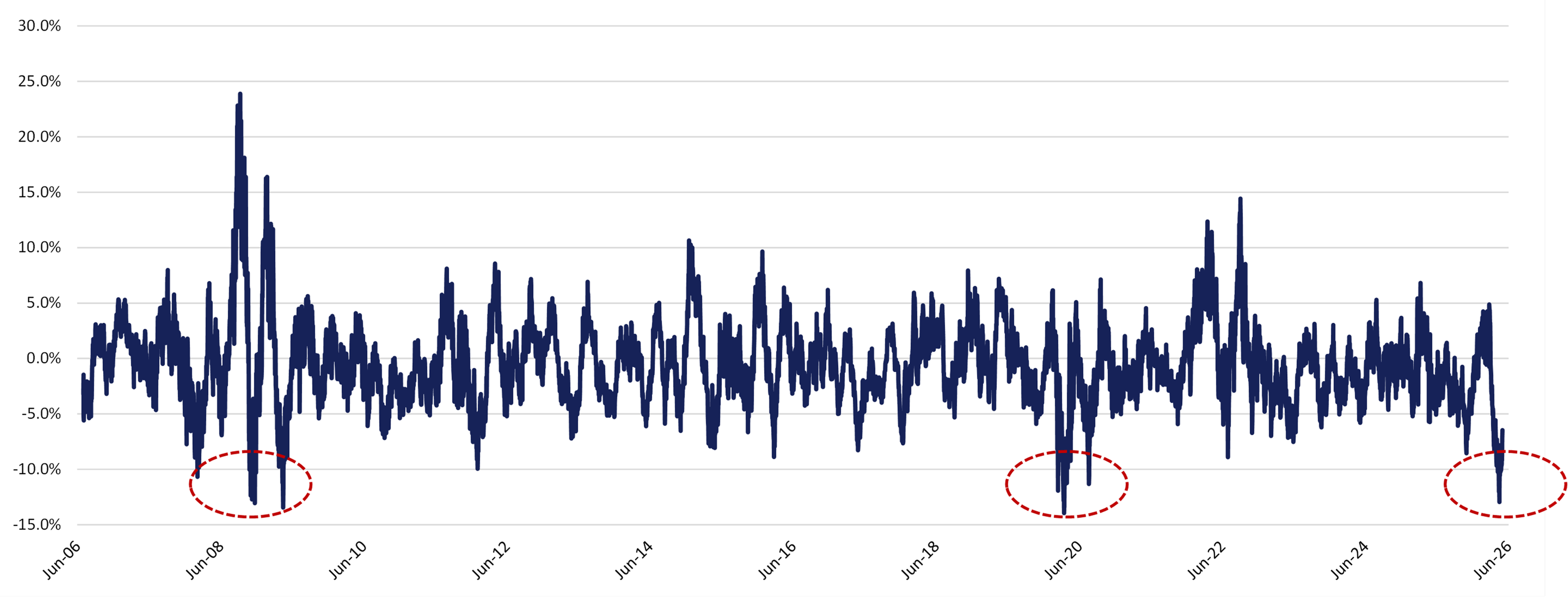

More recently, performance has deteriorated further, with Australia's 60-day rolling performance versus global equities at levels seen only twice over the past 20 years: the global financial crisis (GFC) and COVID-19. Neither coincided with global equity markets at all-time highs like investors are witnessing today.

While both those periods were characterised by extreme uncertainty and global recessions – with global central banks and governments embarking on unprecedented global easing and fiscal support – Australia’s policy mix is adding to the headwinds facing domestic equities at the current juncture.

This has left Australian equities at an 11% discount to global equities, not far removed from the 15% discount that has marked the lows in the post-COVID period.

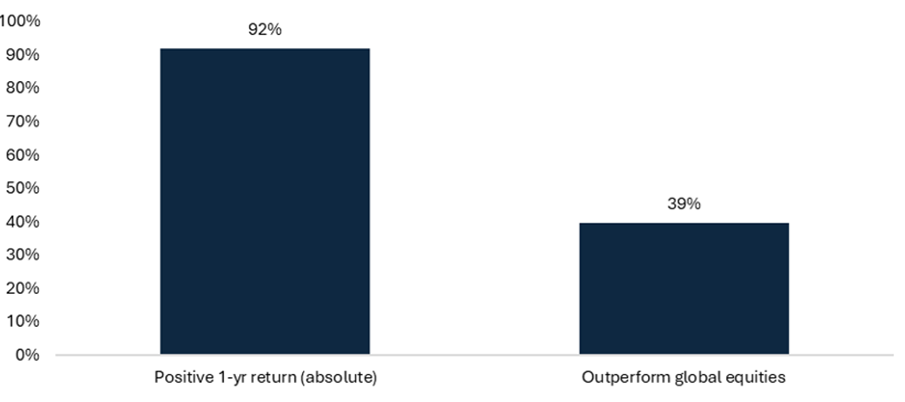

Despite often presaging positive absolute one year returns from such depressed valuation levels, the data is far less compelling in a relative sense. In fact, when Australian equities have traded at a greater than 10% price to earnings (P/E) discount to global equities, they have underperformed global equities on a one year forward basis more than 60% of the time.

Although we are not suggesting outright declines for the ASX 200, we think there are several important issues confronting the Australian equity market that will make relative performance challenged and underscore our tactically underweight positioning.

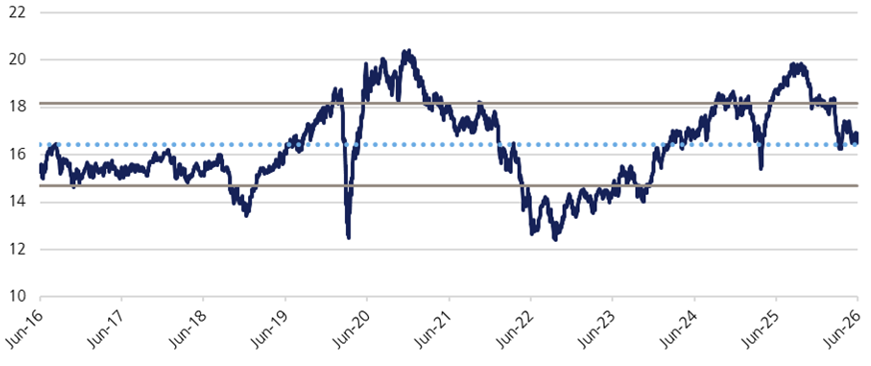

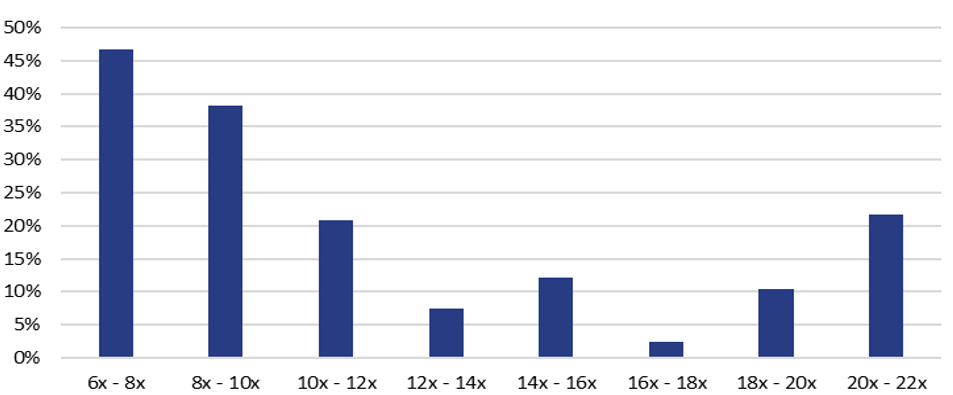

The first and most obvious is that the ASX 200 still trades at approximately 17x one-year forward P/E. Although off the highs from late 2025, it is only at the average of the past decade, and well above levels that definitively marked an improved risk-return tradeoff for the period ahead. With 10-year bond yields at ~4.7%, equity investors are being inadequately compensated for the equity risk they are taking. Median one-year forward returns have historically been their weakest when the starting P/E is in the 16-18x range, as they are now.

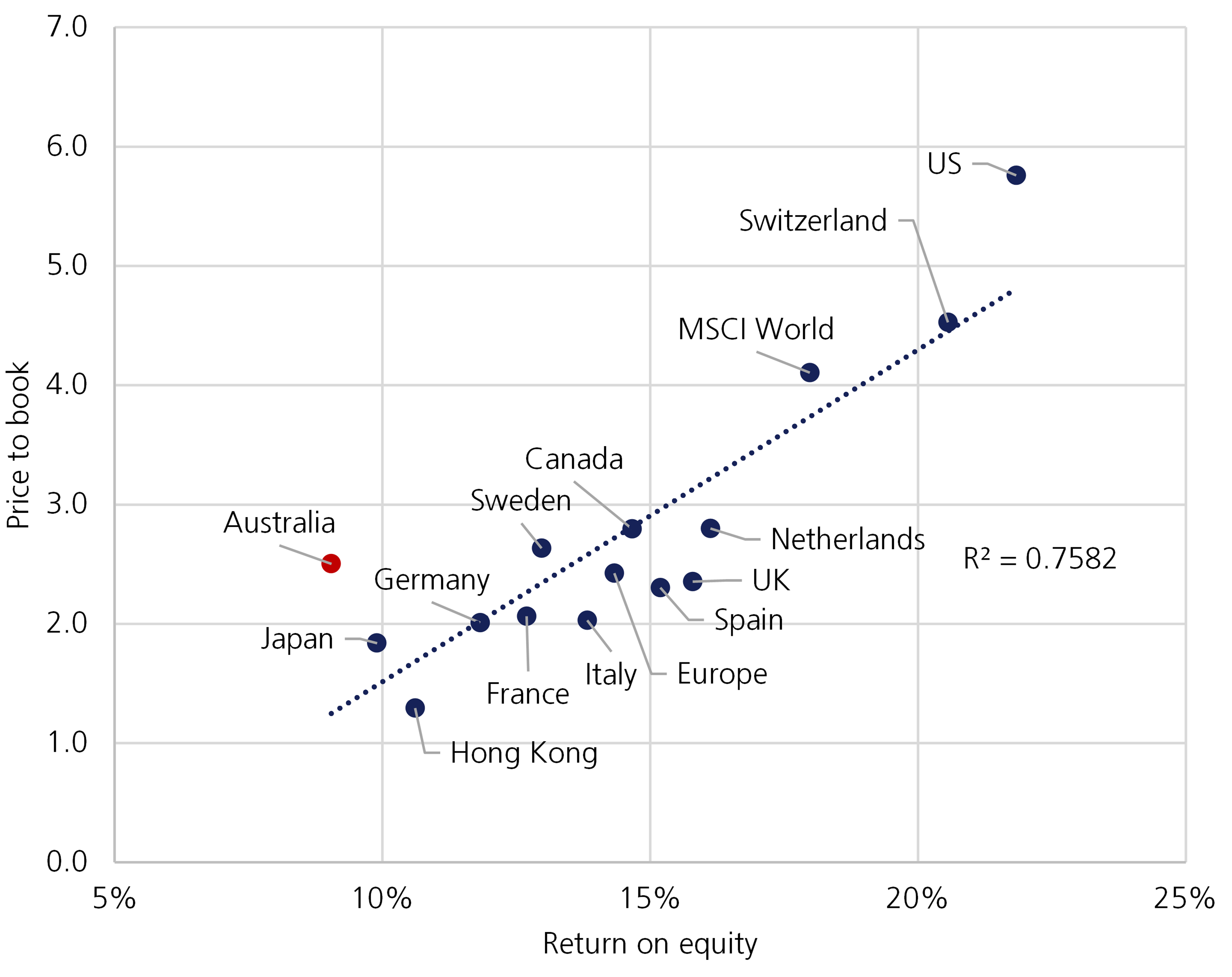

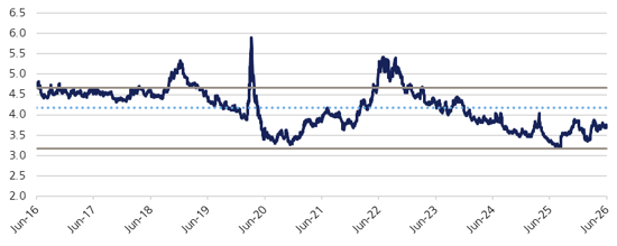

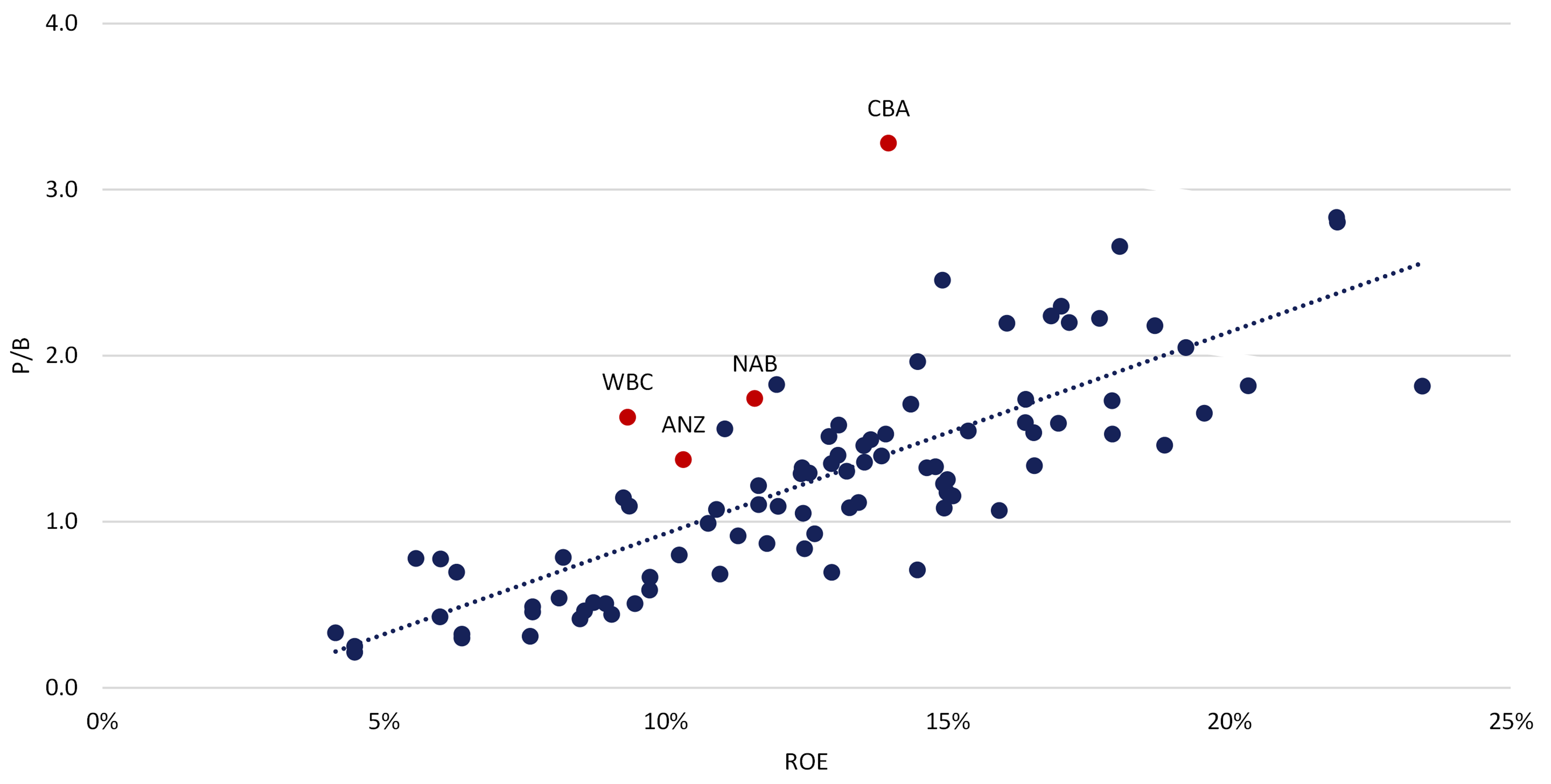

Valuation in isolation means little without accounting for growth metrics, or profitability. On a global price to book (P/B) versus return on equity (ROE) basis, Australia trades expensively relative to other major developed markets. In fact, on this metric, the ASX 200 is more expensive than US equities. Nor is the income on offer in Australia now especially attractive vis-à-vis other markets. The forward dividend yield for the ASX 200 sits at just 3.6%, well below the MSCI World 10-year average of ~4.2%.

Three consecutive 0.25% hikes since February 2026 have taken the Reserve Bank of Australia (RBA) cash rate to 4.35%, and back to 15-year highs. The June RBA decision held rates steady (unanimously), and although Governor Bullock confirmed the Board doesn't need year-on-year consumer price index (CPI) back within the 2-3% target band before easing, only "heading that way," it also made clear further tightening remains possible.

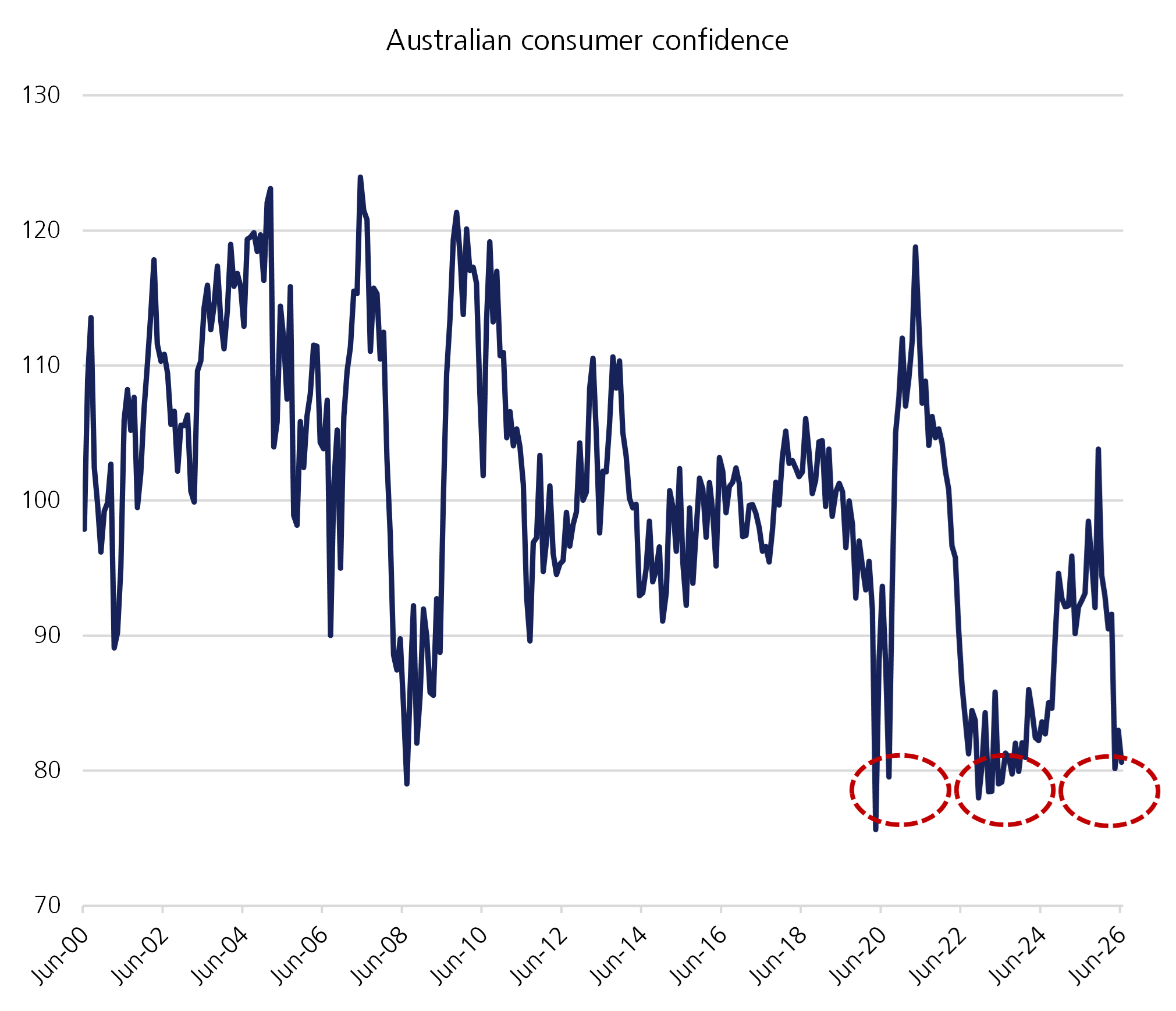

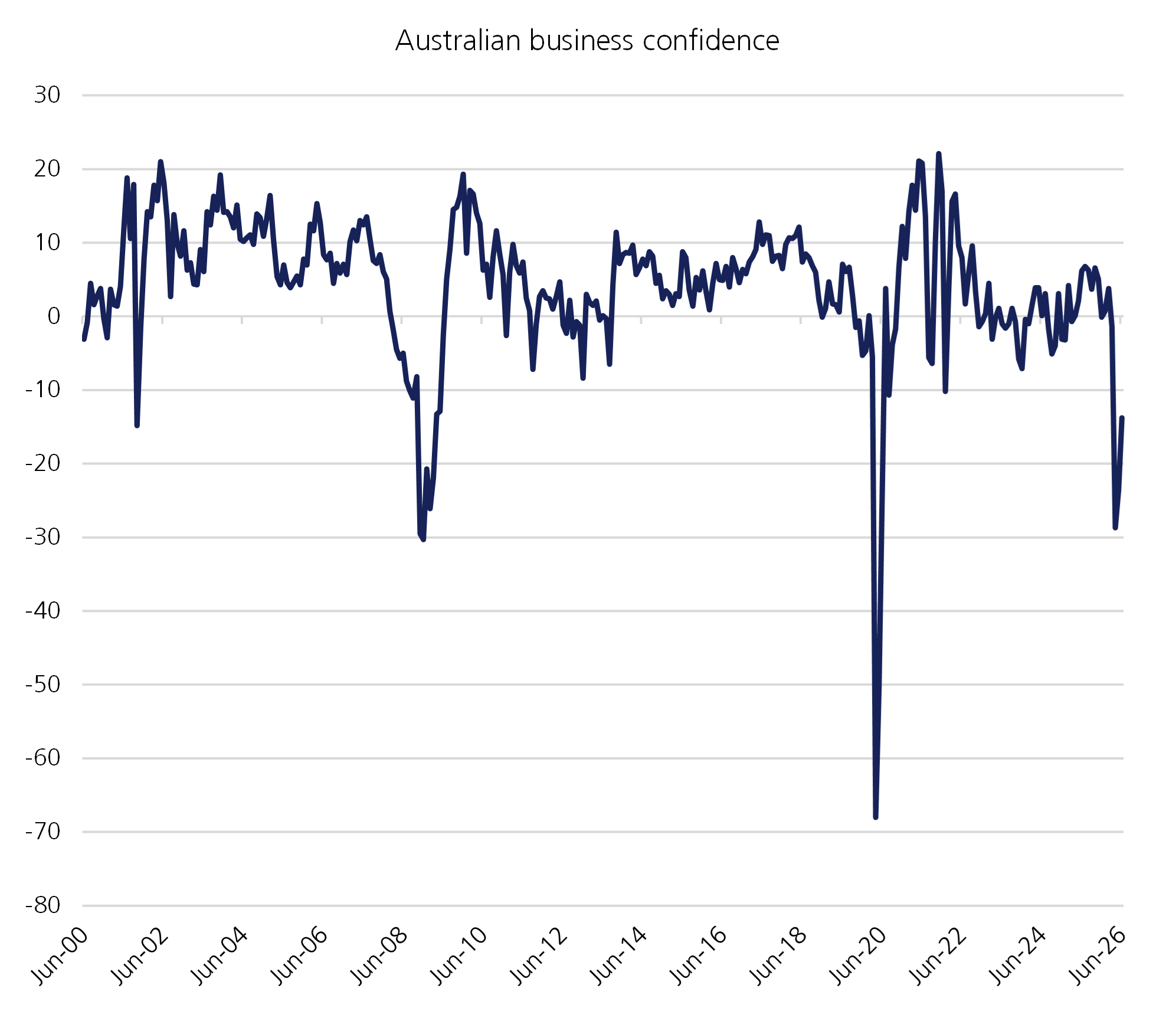

For many homeowners, the most recent rate increases will only feed through to higher borrowing costs in July. Moreover, the economic impact of these three consecutive rate increases is only likely to be felt in 2027, as the lagged impact of tighter monetary policy works its way through the economy. Significantly, cycle high interest rates come at a time when consumer and business confidence are both at readings consistent with previous recessions.

Should the Federal Government’s proposed tax changes be legislated, it’s possible that the outlook for property investment demand changes permanently. Capital gains tax (CGT) and negative gearing changes are an effective increase to the after-tax cost of holding investment property. Westpac’s Consumer Division update in June highlighted the severe (and rapid) impact these proposed changes are already having, with mortgage application volumes falling from approximately 35,000 per month to a post-budget run rate of 27,000, a 23% decline. Mortgage brokers confirm serviceability calculations have been recalibrated, with borrowing capacity reduced by up to 30% in some cases. Investor mortgages represent 55% of monthly mortgage flow and 33% of all outstanding stock for the banking sector. They carry structurally higher net interest margins than owner-occupier equivalents, resulting in a “mix shift” that compounds the already softening volume outlook. This comes at a time when all four major banks are increasing collective provisions to account for an economic outlook they view as deteriorating.

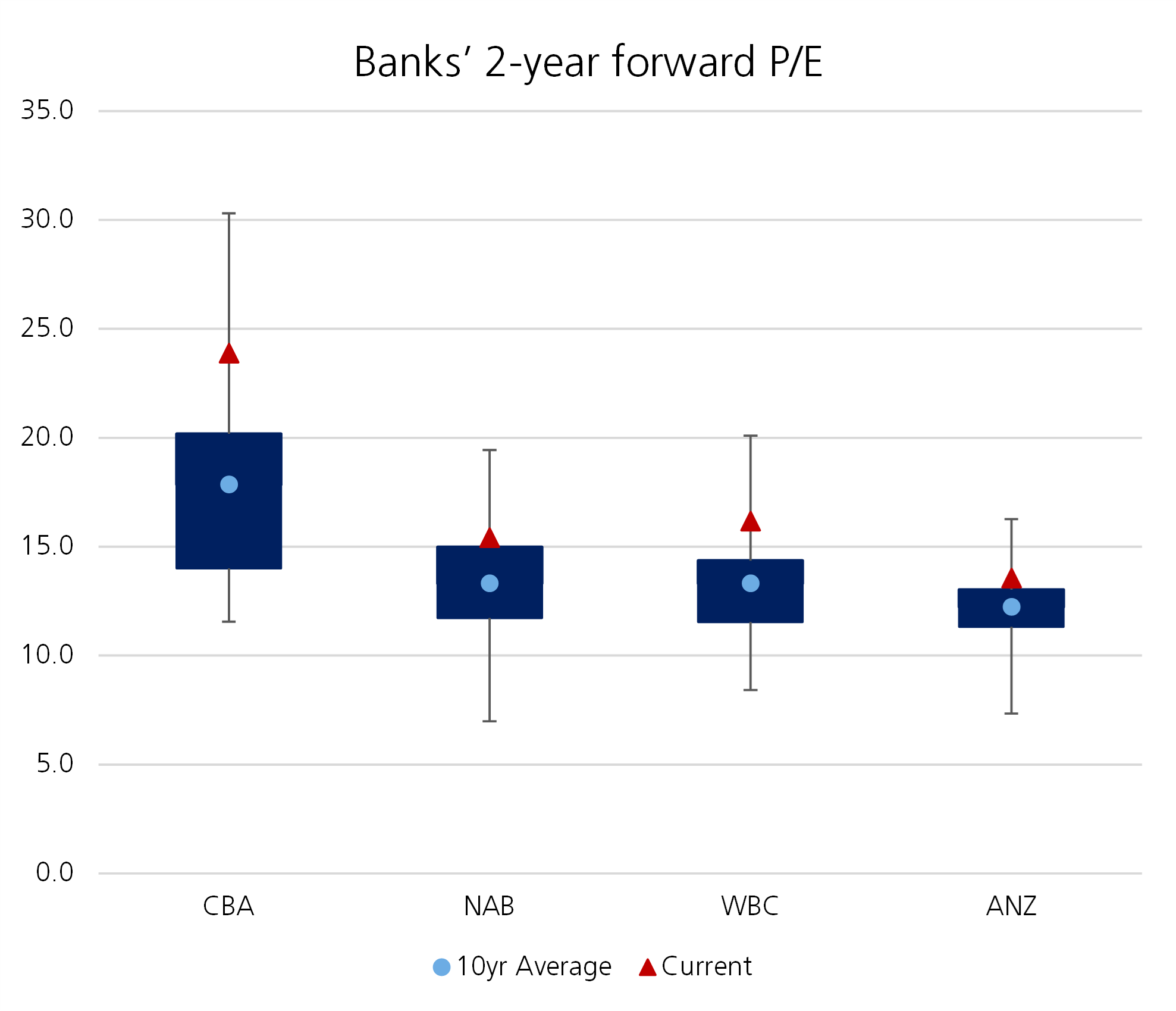

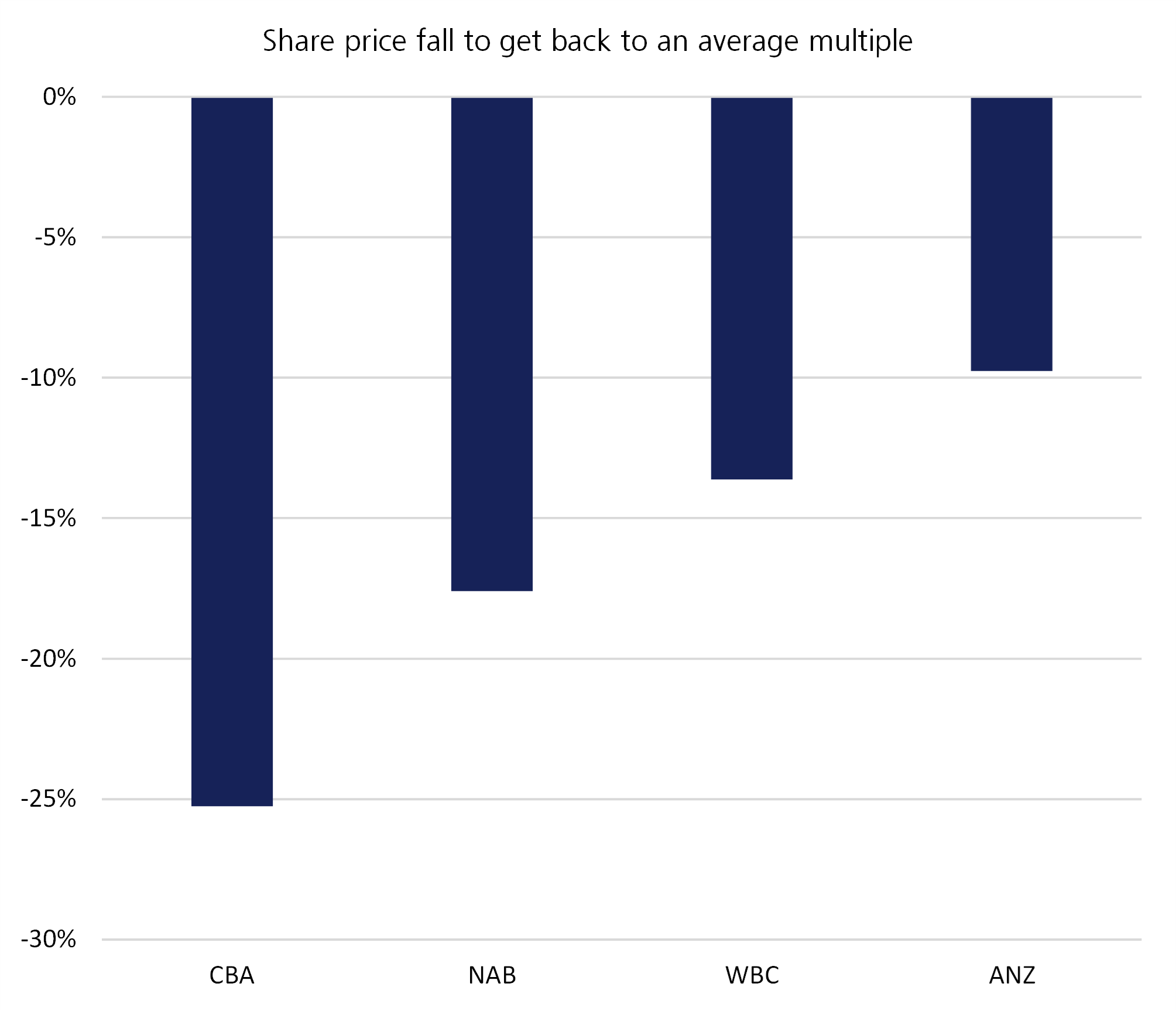

Structurally, this has implications for investors benchmarked to the ASX 200. The sector already trades expensively relative to its own history, and relative to global peers. If major bank valuations were to revert to 10-year averages, it suggests downside could be in the order of 10-25%.

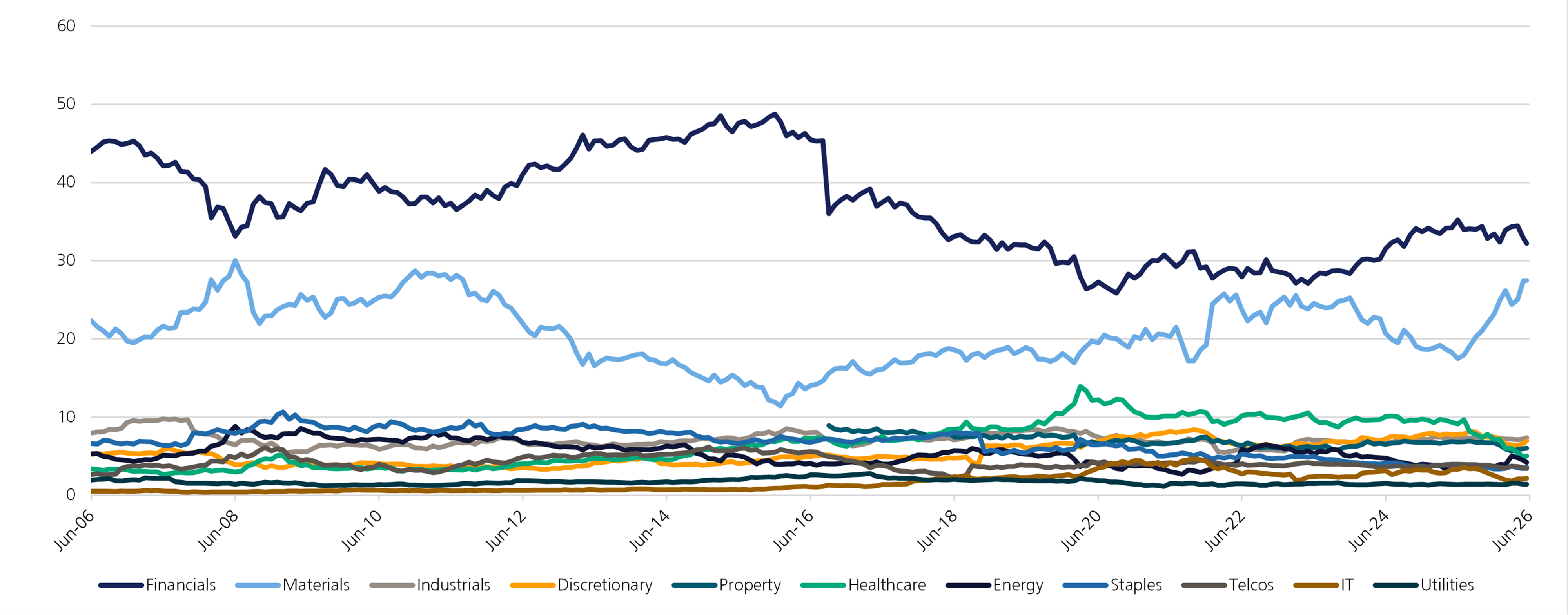

However, the index composition further complicates the economic/budget/valuation headwinds confronting investors in Australian equities. The financials sector remains the largest in Australia, and within that, the major banks are ~two-thirds of the index weight. This creates a compositional headwind for ASX 200 performance, unless the major banks are in an earnings and/or valuation upgrade cycle (which they are now). As the next chart illustrates, outside of the resources sector, all other sectors are comparatively small drivers of overall performance.

Despite this, every sector on the ASX (outside of resources) is now in earnings downgrade mode and is facing macro or idiosyncratic headwinds:

Australian industrials earnings per share (EPS) revisions fell -2.5% in April against upgrades of 3-4% across most developed-market peers.

Consumer discretionary trades at approximately 26x forward earnings with earnings cuts continuing and no rate relief likely before mid-2027. The recent relief rally in discretionary and real estate investment trusts (REITs) (approximately 19x forward P/E) looks premature on both counts. Consumer stocks tend to perform in the final months before the first rate cut in a cycle, but with that event a 2027 story at best, it's premature to call a turn for the sector.

21 of 23 ASX-listed healthcare stocks are in a bear market, facing a combination of valuation, idiosyncratic, business model, and cost-of-living issues.

Resources remain the only sector with positive earnings revision momentum. El Niño, declared by the BoM on 16 June and by NOAA on 11 June, adds an operational tailwind: dry weather improves mining uptime and reduces disruption. Resources may also benefit from rotation within the index as bank flows come under pressure from the budget and credit cycle. That said, performance has been strong. BHP, for example, is witnessing one of its best periods of annual outperformance vs the broader market over the past 20 years.

In aggregate, Australian equities look cyclically and structurally challenged. Although relative performance cautions against staying too bearish, absolute and relative valuations are not supportive, the lagged impact of rate increases is yet to be felt, some economic variables are already at recessionary levels, and the proposed CGT and negative gearing changes add a headwind to a bank-dominated ASX market.

Receive ongoing access to LGT Wealth Management’s insights and observations - a curated stream of thought leadership, market perspectives, and strategic updates designed to inform sophisticated investors.