All dollar amounts are in AUD. Fixed income contributions from Alex Nikolovski.

Treasurer Chalmers delivered the Government’s fifth federal budget on 12 May 2026. As flagged prior, this year’s budget contains a raft of significant revenue raising measures, headlined by substantial cuts to the National Disability Insurance Scheme (NDIS) and reforms to capital gains tax (CGT), negative gearing, and taxes on discretionary trusts. These measures are expected to improve the bottom line by $45.9 billion over the next five years. However, rather than attempting to engage in true tax reform, these additional revenues are being spent on healthcare, defence, housing, and minimal additional income tax relief to working Australians. As a result, forecasts for 2025-26 and for the next four years reveal ongoing persistent deficits of around $30 billion per year (or around 1.0% of gross domestic product [GDP]). The continued strength in the jobs market (and elevated commodity prices) have continued to boost the budget bottom-line to the tune of $37 billion over the five years to 2029-30.

From a fiscal perspective, deficits of a little over 1% compare favourably to offshore, especially to the US (closer to 6% of GDP) and even Europe (at 3%). That said, most of the savings in this budget come in the out-years, with the near-term fiscal impulse still stimulatory (albeit mildly so at 0.2% of GDP). Needless to say, this will only further complicate the Reserve Bank of Australia (RBA)’s challenges in bringing domestic inflation under control. Furthermore, it is with great disappointment that Australians should view this latest ‘attempt’ at tax reform, which essentially amounts to raising taxes further across the economy (and particularly raising taxes on aspirational Australians), in order to spend more on the Government’s chosen policy priorities. The lack of a genuine redistribution of the tax structure, the lack of true reforms targeted at improving productivity, and the lack of focus on repairing Australia’s structural deficits unfortunately threatens to condemn our lucky country to a B+ lifestyle of mediocrity and government dependence.

Coming into this year’s budget, the Government stressed its focus on reform and hard decisions to address generational inequity. The pre-budget announcements of changes to the NDIS, CGT, and negative gearing (none of which were flagged prior to last year’s election) presaged a substantial revenue-raising exercise. The key question for many Australians and investors was, what did the Government intend to do with this additional revenue? Embark on genuine tax reform to structurally shift our unbalanced tax base, perhaps redistributing the increased tax take via personal income and/or corporate tax reform? Genuine productivity measures to help Australia compete in an increasingly uncertain and volatile multi-polar environment? Or more cost-of-living and vote-buying spending?

Unfortunately for investors and Australians, the Government chose the latter, with the savings spent on healthcare, defence, fuel security, and housing, alongside minimal additional tax relief for Australian workers (which will be trivial for individuals but will still cost $6.8 billion over the forward estimates). The 2026-27 budget forecasts a deficit of $31.5 billion (1.0% of GDP) for 2026-27, a modest improvement from the Dec-25 Mid-Year Economic and Fiscal Outlook (MYEFO) forecast of $34.3 billion. This is driven by a more resilient economy that delivers $9.3 billion to the bottom line, offset by cost-of-living spending of $6.5 billion. Off balance sheet spending masks an even greater fiscal deterioration – over the next four years, the cumulative headline cash deficit is expected to be $94 billion worse than the Government’s preferred underlying cash deficit measure.

Thereafter, out to 2028-29, the bottom line is little different, with the deficit stable at 1.0% of GDP before a modest improvement to 0.7% in 2029-30. Effectively, increased revenues and savings are being re-allocated to new spending until the NDIS savings start ramping up from 2029-30 and beyond. The reforms to this program may end up being a silver lining over the long-term, with CBA estimating they could save up to $170 billion over the next decade – potentially providing a future, braver Treasurer (or one seeking re-election) with a war chest to embark on genuine tax and productivity reform (or simply spend more).

As flagged prior to budget night, there are four key pillars behind the Government’s revenue-raising initiatives for this budget, highlighted by significant reforms to the NDIS, CGT, negative gearing, and trusts. Combined, these four measures are expected to add $45.9 billion of revenue over the next five years, with revenues increasing further over time.

Disappointingly, despite the Government’s massive parliamentary majority, a fragmented opposition, and no imminent election, this year’s budget contained little in the way of genuine reform in spending or productivity measures. It does, however, include further spending on the care economy, cost of living, defence, and fuel security. This year’s key spending policies include:

2026-27 budget and out-years underlying cash balance

|

| 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 | 5-yr sum | ||

FY26 MYEFO (Dec-25) | $ billion | -36.8 | -34.3 | -36.2 | -36.0 | -52.1 | -195 | ||

| % of output | -1.3 | -1.1 | -1.1 | -1.1 | -1.5 |

| ||

Economic parameter impacts | $ billion | +13.8 | +9.3 | +7.5 | -1.5 | +7.6 | +36.6 | ||

New policy announcements | $ billion | -5.3 | -6.5 | -2.3 | +3.1 | +19.3 | +8.2 | ||

2025-26 budget | $ billion | -28.3 | -31.5 | -31.0 | -34.4 | -25.3 | -150 | ||

| % of output | -1.0 | -1.0 | -1.0 | -1.0 | -0.7 |

| ||

Source: Australian Government, LGT Wealth Management.

What does it mean for markets?

Equities – markets fall in the lead-up

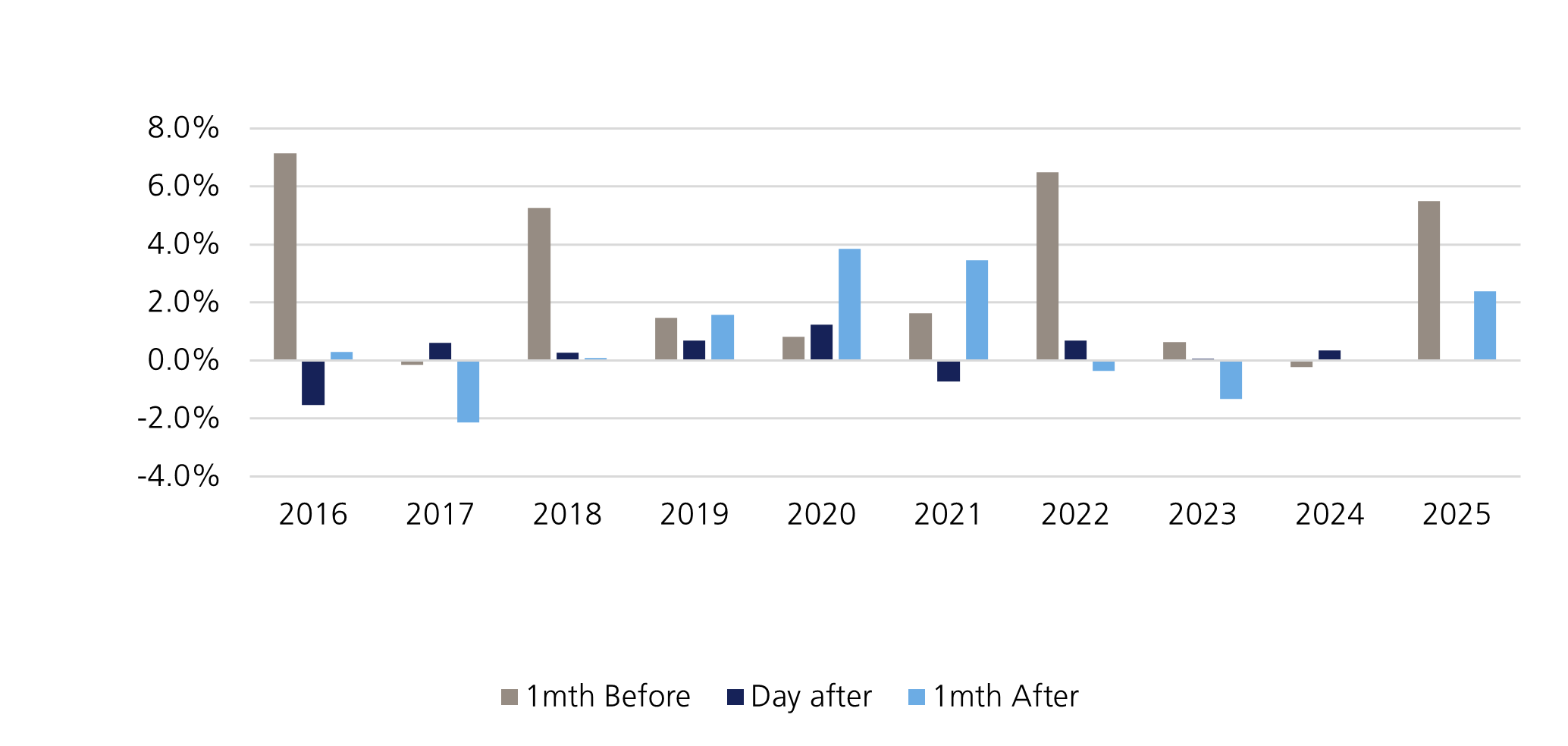

On average, the Australian equities market is typically up almost 3% in the month prior to the federal budget. This partly reflects the fiscal largesse that has historically been flagged or leaked ahead of budget night, particularly where it supports consumer spending, infrastructure, construction or other domestically-exposed sectors. However, this year, the market has bucked that trend, falling over 3%. This is in stark contrast to global equity markets, which have gained ~7% over the same period, condemning Australian equities to COVID-era levels of annual underperformance.

Although impossible to apportion with precision, part of the underperformance likely reflects concern that the reforms to CGT and negative gearing, housing uncertainty and lack of productivity reform could weigh on already fragile business and consumer confidence.

Although last night’s budget was structurally significant – particularly across tax, housing incentives and NDIS reform – its equity-market impact is likely to be more selective than the pre-budget headlines suggest. The stock market is not the economy – Australian Securities Exchange (ASX) listed companies derive only 55–60% of revenue from Australia, and superannuation funds, which are ring-fenced from the CGT changes announced last night, own a large proportion of the listed equity value.

The budget's savings are built around four pillars, however, not all of them are equity-market significant (at a stock or sector level):

Analysis by Barrenjoey models a 3-4% fall in house prices from the combined CGT and negative gearing changes, equivalent on their estimates to 25–30bps of rate hikes – enough, they argue, to keep the RBA on hold through its August meeting (the market is fully priced for a September hike). Whether that order of magnitude holds is difficult to assess, as the pro-rata grandfathering mechanism will likely create a front-loaded selling incentive for some property investors if they sell before July 2027, rather than after it.

Replacing the 50% CGT discount with inflation indexation removes the simple, highly visible reward for holding an asset beyond 12 months. Investors will instead be taxed more explicitly on real capital gains. UBS argue this shifts relative attractiveness from capital-gains-oriented strategies toward income. We’re reluctant to overplay this impact, although we support the logic, at the margin – we’re not convinced Australian-domiciled investors explicitly targeted a different holding period for longer-duration growth stocks. However, we concur that an increase in capital gains tax may result in shareholders rewarding companies with higher dividend payout ratios and dividend yields, given Australia’s dividend imputation policy remains intact. Ultimately, with the superannuation industry owning a substantial swathe of the equity market and exempt from these changes, any impact is likely to be marginal and orderly.

Restricting negative gearing to new builds should slow investor credit growth – the Parliamentary Budget Office estimated this saves AUD $2bn per year – which weighs directly on loan growth and, at the margin, net interest income for the major banks. A 3-4% fall in residential collateral values would compound the effect, although the transmission mechanism is not credit losses in the first instance, but weaker investor credit growth, softer housing turnover, slower collateral appreciation and more cautious household sentiment. The impact is likely to be modest unless the housing-price effect is larger than expected.

Both CGT reform and negative gearing restrictions could accelerate housing turnover in the near term as investors reassess after-tax returns. That could support listing volumes, and digital property company REA Group has notably outperformed the broader market over the past month. Longer-term, there is a risk that the near-term boost to housing turnover fades as the investor cohort shrinks (higher after-tax costs mean fewer leveraged investors, and fewer investors means fewer listings).

While there is some near-term uncertainty likely for residential property developers, especially combined with higher rates, Citi analysts see some medium-term demand upside as investors shift to new housing to capture tax benefits. We are also likely to see further concentration of wealth in Australians’ principal place of residence (PPR), which remains exempt from all CGT.

The Working Australians Tax Offset (~AUD $6.4bn, equivalent to roughly 20bps of RBA easing and applicable to all wage earnings) and the simplified $1,000 work-related deduction (AUD $1.3bn, applying to 6.2m workers) provide some cash-flow support to lower- and middle-income households, where the propensity to spend is highest (noting that the deduction is not equivalent to a $1,000 cash payment but is dependent on a taxpayer’s marginal tax rate). There are consumer discretionary benefits at the margin, although cost-of-living pressures, and potentially flat-to-negative household wealth effects will likely mitigate any share price relief for the sector.

Across a variety of sectors, there are also several smaller, but at the margin, impactful measures in the budget:

In aggregate, the budget is broadly neutral for Australian equities, with potential ‘flow-related’ tailwinds somewhat marginal and long-dated, and ignoring the second order impacts that the most negatively impacted from today’s budget (banks via housing impacts) are also the largest single cohort in the ASX200. The direct market impact should be diluted by the offshore earnings mix of the ASX, the importance of superannuation and institutional ownership, and the fact that some of the downside appears to have already been priced through the pre-budget underperformance of several sectors.

Australian equities have, on average, gained almost 3% in the month leading into federal budgets over the past decade. This time, Australian equities have fallen ~3%, an almost 6ppt differential to what we had expected. This has been most pronounced in the performance of the economically sensitive parts of the market:

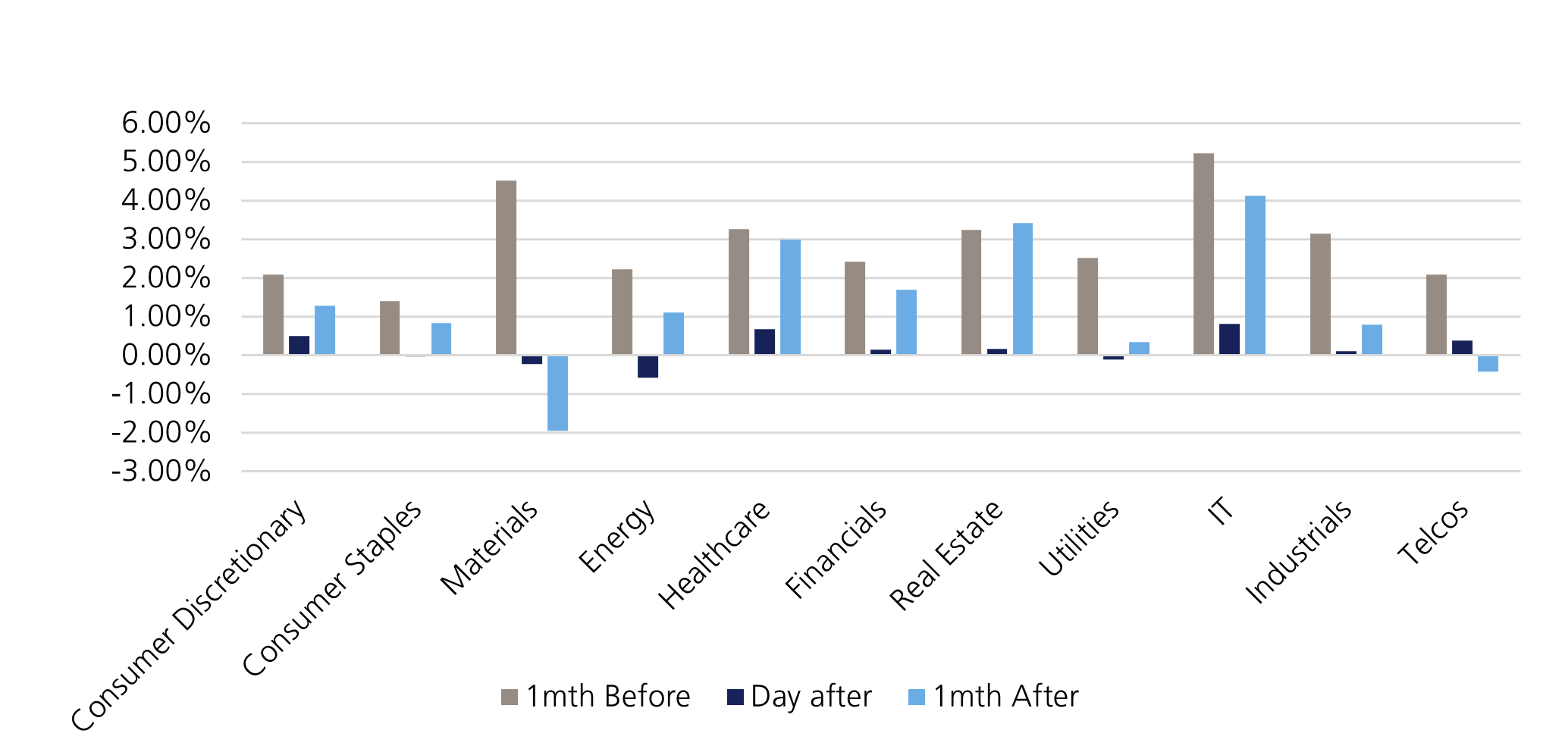

The data following the budget is also instructive at a sector level:

Source: Bloomberg

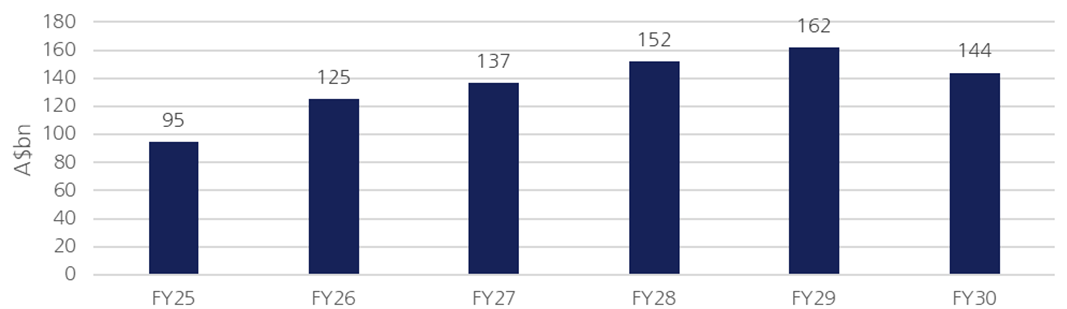

The federal budget points to a modestly larger funding task than markets had expected, with the AOFM likely to announce around $137 billion of nominal Australian Commonwealth Government Bond (ACGB) issuance for FY27, above expectations of $125 billion. Issuance will likely include around $40 billion of syndications in new 2038 and 2057 lines, helping to improve liquidity, and extend the ACGB curve in the 10-year and 30-year sectors, respectively. The balance is expected to be issued through weekly tenders. The budget also implies average gross issuance of around $153 billion across the following three financial years (FY28-30).

The modestly larger issuance profile is likely to place some upward pressure on long-end yields in the near term. Over the medium to longer term, however, we believe the increase in issuance is largely expected by markets, and is therefore unlikely to result in sustained underperformance, particularly given Australia remains one of the few sovereign issuers globally to retain a AAA credit rating. In our view, Australia’s solid fiscal fundamentals should support investors’ capacity to absorb the additional $12 billion funding task.

Source: Australian Government, Barrenjoey

Receive ongoing access to LGT Wealth Management’s insights and observations - a curated stream of thought leadership, market perspectives, and strategic updates designed to inform sophisticated investors.