Hear the latest geo-political commentary from our investment team.

Absolutely nothing! Investors around the world will surely agree, as they deal with ongoing market volatility and the global oil supply shock from the United States (US) and Iran conflict. Near-term uncertainty remains elevated. However, as we noted in our various Special Reports over the past month, there are increasingly clear signs that we may have passed peak geo-political uncertainty – a critical inflection point that allows markets to check an enduring bottom (as happened during the Liberation Day sell-off last year). Indeed, we have seen global equity and credit markets retrace most of their losses in recent weeks, with the US S&P 500 Index marking fresh record highs in April.

As inconceivable as this may seem, there are fundamentally sound theoretical and empirical underpinnings driving this ‘heartless’ market rally. Below we reiterate our constraints-based assessment of the situation in the Middle East. The recently announced ceasefire in Iran and Lebanon backs our view that the material constraints were pushing all parties towards de-escalation before the disruption of the Strait of Hormuz triggered a catastrophic global recession. If the ceasefire holds and the oil starts flowing again soon (this is now the key variable, not military strikes), we see a narrow but navigable path for the global economy to avoid a worst-case scenario. In support of this, we retain our overweight positioning in global equities, while staying alert to the risks and opportunities that may arise in coming weeks and months.

While we may not be out of the woods yet, in this month’s CIO Monthly, we take a step back and consider some timeless lessons that this shock has delivered for astute investors. From a long-term strategy perspective, geo-political shocks often present buying opportunities for bold investors, an investment framework for navigating geo-politics is no longer optional, and ultimately, it never pays to bet against the human race. From a portfolio management perspective, the more volatile world we are now in requires more thoughtful cross-asset diversification, including the use of alternative assets, and emphasises the value of having dry powder to respond opportunistically in times of high stress.

The global economy and financial markets have endured another testing period of volatility and extreme policy uncertainty, almost exactly a year on from Liberation Day’s market turmoil. Over the course of March, the kinetic and rhetorical conflict between the US, Israel, and Iran continued to escalate, while the physical oil supply shock from the disruption of the Strait of Hormuz has continued to raise angst and uncertainty across the real economy worldwide.

Through this period, we have remained steadfastly focused on our constraints-based framework, which told us with increasingly high conviction over the course of the month that (1) US President Trump had hit the limit of his constraints (elevated domestic energy prices and bond markets) and would be open to a deal, and (2) that Iran faced constraints of its own, primarily that it cannot keep the Strait of Hormuz closed indefinitely in the face of growing global consternation.

Based on this analysis, we believe that we may have reached a peak in local uncertainty, likely marked by the 8 April ceasefire (that admittedly followed Trump’s threats of “civilisational” damage to Iran). The near-term road remains highly uncertain, with clear risks on both the downside and the upside, and the global economy may require months (or longer) to adjust and recover from the physical oil shock. However, just like in April 2025, the inflection point where uncertainty stops increasing is the most important point for financial markets, which move off the second derivative, not the first. As investors experienced both last year and during the COVID-19 sell-off, markets don’t need to see that things are getting better to bottom. They just need to see that things have stopped getting worse.

If our assessment is correct and a deal is reached to re-open the Strait of Hormuz and avoid a longer-term energy availability crisis, the backdrop for the global economy remains upbeat. The echoes of prior monetary and fiscal policy easing are still supportive for activity and markets, at least outside of Australia. Meanwhile, both household and corporate balance sheets in the US remain in rude health, providing a fundamental backstop that should moderate the impact of any near-term technical recession. Further, while there remains uncertainty around the disruptive impacts of artificial intelligence (AI), we are also seeing increasing real-world evidence that the roll-out of AI is translating into new earnings and revenue streams across the economy. Within the software sector, which has been hit by indiscriminate selling this year, we are also seeing a recovery as the very best firms lay out plans to adapt their business models for an AI future.

In addition, while we must maintain our vigilant watch for downside risks as the US and Iran ‘dance’ their way towards a hoped-for deal, we also cannot discount the right-tail risk: it is well within the realms of possibility that the US and Iran could reach a ‘grand bargain’ that sees a lifting of sanctions and a potential re-integration of Iran into the global economy. With a young, educated, and dynamic population of 90 million, this could be immensely positive for the Iranian and global economy.

Our central case continues to tactically favour equities over fixed income, even with the risk that equity markets deliver more moderate, and potentially choppy, returns over the rest of the year. As such, we re-affirm our modestly overweight position in equities this month, while maintaining a nimble and flexible stance to ensure we can respond to the evolving global environment.

While it is still too soon to chart out the near-term geo-political and economic pathway from here, we highlight below several key ramifications that investors and policymakers will have to consider once we (hopefully) get to the other side of the kinetic conflict:

Trump has exhausted his political capital: regardless of how he spins this, US President Trump will likely be marked down severely by the US voter for this expedition. The US electorate is opposed to the war by a large majority, particularly amongst independent voters, as high gasoline prices fuel community inflation concerns. Betting odds of a Democratic sweep in November’s mid-term elections have risen substantially, and voter sentiment will only worsen the longer the oil price spike continues. As such, unless he can engineer an incredible turnaround in gasoline prices and/or economic conditions, Trump could be looking at a landslide defeat that would neuter the final two years of his administration. It is likely that this exhaustion of political capital will constrain his executive authority and actions until and unless he can turn his polling around.

That said, there is an important counterargument. If a landslide defeat becomes increasingly inevitable, President Trump may become more emboldened, not less, to project the Administration’s ideological convictions abroad. The same political constraints that currently favour resolution could therefore weaken over time: the longer the conflict endures, the closer we move to a point where electoral discipline becomes less binding as a moderating force.

Modern warfare greatly favours the defender: the Russia-Ukraine war has already seen both combatants bogged down into years of stalemate by the advent of mass drone usage and asymmetric warfare tactics. This latest conflict appears to have further highlighted the advantages that a smaller, defending nation has over even a global superpower. Iran’s ability to utilise drones, de-centralised military resources, and asymmetric economic warfare has driven even the mighty US military to an effective stalemate. We think the Great Powers of the world, including China, should learn some important lessons from this. In particular, an invasion of Taiwan would be an incredibly daunting task for even the most modern military to undertake. This does not rule such a scenario out, but we imagine the constraints on such a course of action would be swift and brutal (both economically and militarily).

Oil could be under US$50 a barrel in three years: we are amidst an unprecedented oil supply shock, and investors, policymakers, and the global community are understandably concerned about the prospect of oil prices spiking towards US$150 a barrel or beyond this year. However, we believe that such a spike (if it occurred) would not last long, because of the simple fact that such high oil prices would trigger a global recession, which would naturally reduce global demand and bring oil prices back down again. Looking further out, we actually see a pathway for oil prices to collapse, perhaps to US$50 a barrel or below over the next three years.

In response to the disruption to the Strait of Hormuz, we expect governments around the world to (1) accelerate electrification of their economies, and (2) “drill baby drill” to secure domestic oil supplies independent of the Middle East. Both dynamics would affect the demand and the supply side of global oil markets, and like the US shale boom in 2015, could lead to an eventual oversupply of oil which would trigger a collapse in oil prices.

The United Arab Emirates’ decision to leave OPEC effective 1 May may be an early sign that cartel cohesion is starting to fracture. If producers increasingly act in their own national interest – producing closer to capacity rather than preserving OPEC discipline – the medium-term risk is that today’s supply shock gives way to tomorrow’s oversupply.

Apart from these near-term considerations, we also believe there are a set of timeless, crucial lessons that long-term investors need to take away from this crisis.

The weight of historical experience, especially since World War II, points to the cruel truth that geo-political shocks ultimately present buying opportunities. We see three key reasons why:

Geo-political shocks are exogenous to the macroeconomic system: Like COVID-19, geo-political shocks are external to the economic system. No corporation or economic actor is particularly to blame, and therefore policymakers tend to be much more lenient in their policy reaction functions. In other words, the first reaction of fiscal and monetary policy is to stimulate the economy. We are seeing this already, with the Australian government’s fuel excise cut a clear example of this untargeted, broad-based fiscal stimulus (just like COVID, the effectiveness of such policy decisions is for another time!). If the geo-political situation worsens, we expect significantly more stimulus to come across the globe.

Constraints reveal themselves quickly in war: the reality of kinetic conflict very quickly reveals the true constraints and limitations of all parties. This very quickly condenses the realm of possible outcomes to a much smaller set of probable outcomes.

Markets are not moral arbiters: financial markets do not price human suffering directly; they price the implications for growth, inflation, interest rates, earnings and risk premia. That is an uncomfortable distinction, but an important one for investors assessing geo-political shocks. The humanitarian significance of an event can be profound while its investment significance remains limited, unless it alters the economic transmission mechanism.

An investment framework for navigating geo-politics is no longer optional

The incredible velocity of newspaper headlines, social media hearsay, AI-generated propaganda, and policy announcements has likely given many investors a severe case of whiplash over the past two months. For us, it is yet another clear proof case that to be a successful investor in today’s world, you simply must have a framework for navigating politics and geo-politics.

We have spent the last two years adapting and developing our constraints-based framework, which we detailed extensively in our February 2025 Observation ‘The New Great Game’. It remains at the core of our tactical asset allocation process and serves as a disciplined north star that keeps us focused on what matters while others panic.

Over the long-term, it never pays to bet against the human race

We are acutely aware of the stream of negativity that has permeated investment commentary and the broader media amidst this conflict. There is a sound commercial reason behind this – as Morgan Housel noted in his book The Psychology of Money, “Pessimism sounds smarter and more plausible than optimism… tell someone they’re in danger and you have their undivided attention”.

We believe this negative mindset does long-term investors – and the broader human community – a deep disservice! To the contrary, there is copious empirical evidence that investors should hold a fundamentally optimistic long-term outlook. In other words, it always pays to believe in the human race, and it never pays to bet against humanity. As a species, we have overcome every single existential challenge we have ever faced, and achieved incredible things over our history including:

COVID-19, where we achieved a gargantuan scientific, medical, and regulatory feat in developing, testing, and deploying a novel vaccine within six months of the outbreak.

The Apollo programme, where intrepid humans were walking on the moon a mere seven years after John F Kennedy’s famous “We choose to go to the Moon” speech.

The Marshall Plan, which rebuilt Europe’s shattered economy after World War II, gave new hope to a continent, and ultimately laid the foundations for today’s European Union.

The Ancient Greek Pheidippides, who ran 42 kilometres from Marathon to Athens to deliver the good news of victory, sacrificing his life for the greater good.

There are countless tales of humanity’s great achievements against all odds, and we have no doubt that there will be countless more as we face off against the existential challenges of today: multi-polarity, climate change and the energy transition, populism and societal inequity, and the societal and employment implications of the ongoing AI roll-out.

While pessimistic newspapers may decry these problems as unsolvable, we choose to see them as challenges that will catalyse the next generation of human innovators. Rather than cower in fear at an unknown future, we choose to find, support, and finance these pioneers, and ultimately profit along with greater humanity as we add more achievements to the great book of the human story.

While every crisis is different, as the dust somewhat settles, it’s important to look in the rear-view mirror and assess what worked and what didn’t work, as well as the response mechanism that ultimately shaped how portfolios responded to the environment. Coming into 2026, markets seemed unflappable having navigated tariffs and ‘Liberation Day’ seemingly successfully with equity markets subsequently posting yet another double-digit return. It was a very benign backdrop with potential rate cuts in the US expected to keep the momentum going as inflation remained under control across most of the developed world. This backdrop was also supportive of diversification as cross asset correlations fell significantly through 2025 and into 2026. We saw early signs of higher dispersion in 2025 and this to an extent continued into 2026. The chart below shows the fall in correlations through 2025 compared to past crises over the last 25 years.

With a supportive cross asset correlation backdrop, portfolios seemed well positioned for any bursts of volatility after a period of strong equity market gains. We had seen the ex-US trade begin to gain momentum, market breadth was broadening through sectors and market cap, and the US dollar was declining. This all gave investors ample opportunity to diversify portfolios after a prolonged period of narrow leadership.

However, the reaction function to a risk-off environment did not necessarily play out as market participants would have expected. There was a meaningful shift in cross asset correlations from February 2026 to March 2026, significantly reversing the trend seen through 2025. A number of the typical ‘safe-haven’ assets did not necessarily behave in a defensive manner which limited the levers allocators tend to rely on in risk off environments. Typical safe haven assets include bonds, the US dollar and gold. This also feeds into the construct of the 60/40 portfolio which is expected to benefit from ‘negative’ correlation primarily between equities and bonds. For an AUD investor, USD exposure provides an additional risk mitigation lever in risk off environments.

The volatility in March saw both equities and bonds sell off as cross asset volatility accelerated, presenting challenges for multi asset investors. A sharp repricing in front end rates and a breakdown in correlations across asset classes saw equities lower, yields higher, oil higher and the USD stronger. Investors’ response was to seek liquidity elsewhere to fund any rebalancing and/or margin calls experienced in other parts of the portfolio which cause even broader cross asset correlations. In short, any investments that had experienced strong momentum driven returns were used as a funding source in response to liquidity stress elsewhere noting bonds are typically the liquidity source in risk off environments. Gold is a good example of an asset with defensive characteristics that experienced a liquidity driven sell off.

The reality is that the relationship between equities and bonds is not that simple and their correlation has not always been negative. Over time, correlations have been volatile and, at times, positive, as was the case in March 2026. Macro-economic factors tend to drive equity/bond correlations and historically, inflation has been highly correlated to this relationship. Periods of moderate inflation are typically supportive of low to negative correlation and subsequently positive in high inflation environments. Recent events in the Middle East resulted in an oil price rally which consequently triggered a sharp repricing of global inflation risks resulting in elevated rates volatility across markets. This also occurred at a time when a number of central banks were eyeing further easing which ultimately exacerbated the selloff/move. Given bonds also tend to be a source of liquidity in risk off environments as investors rebalance portfolios, this caused some chaos as investors sought other liquidity sources within the portfolio.

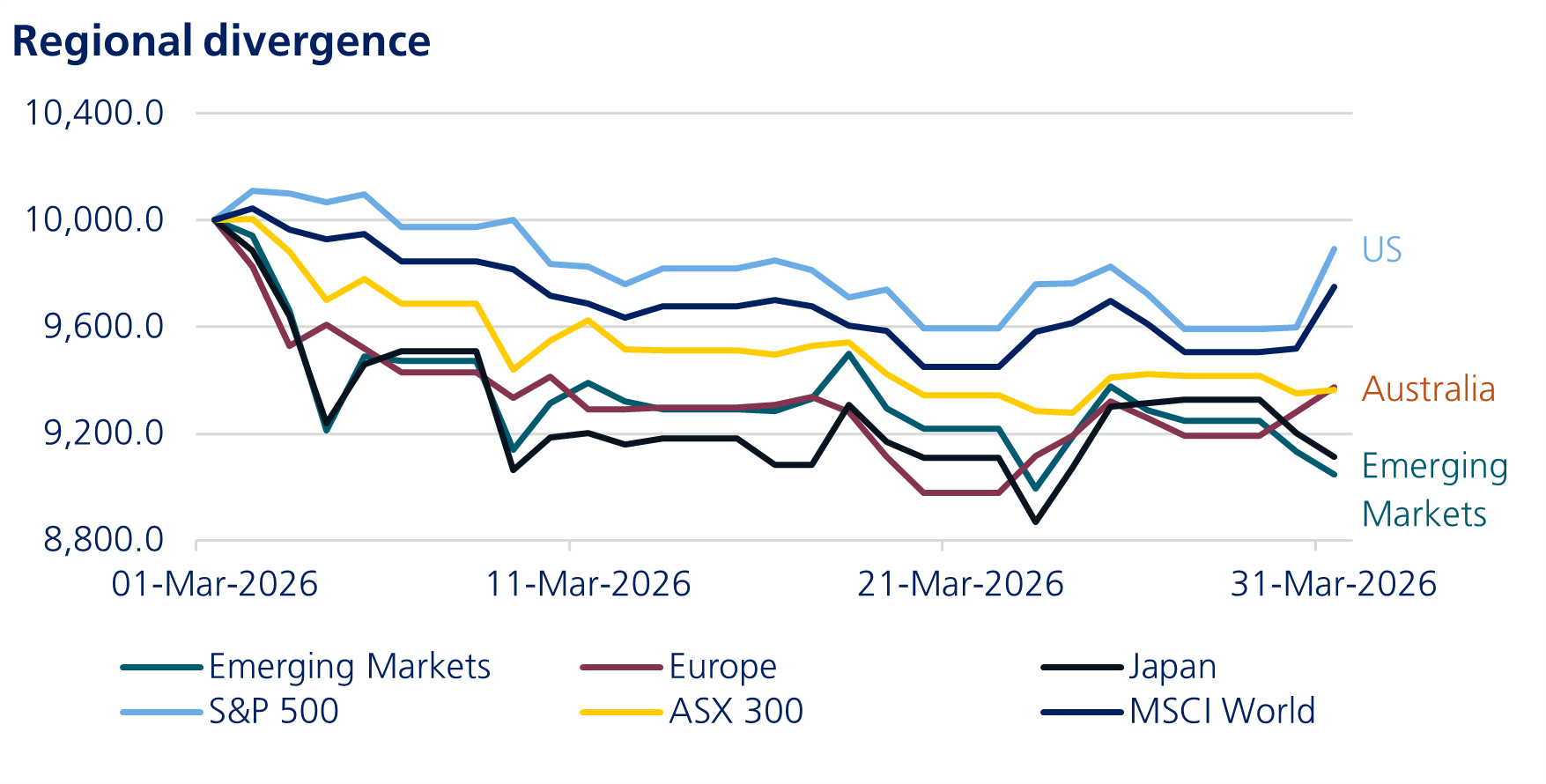

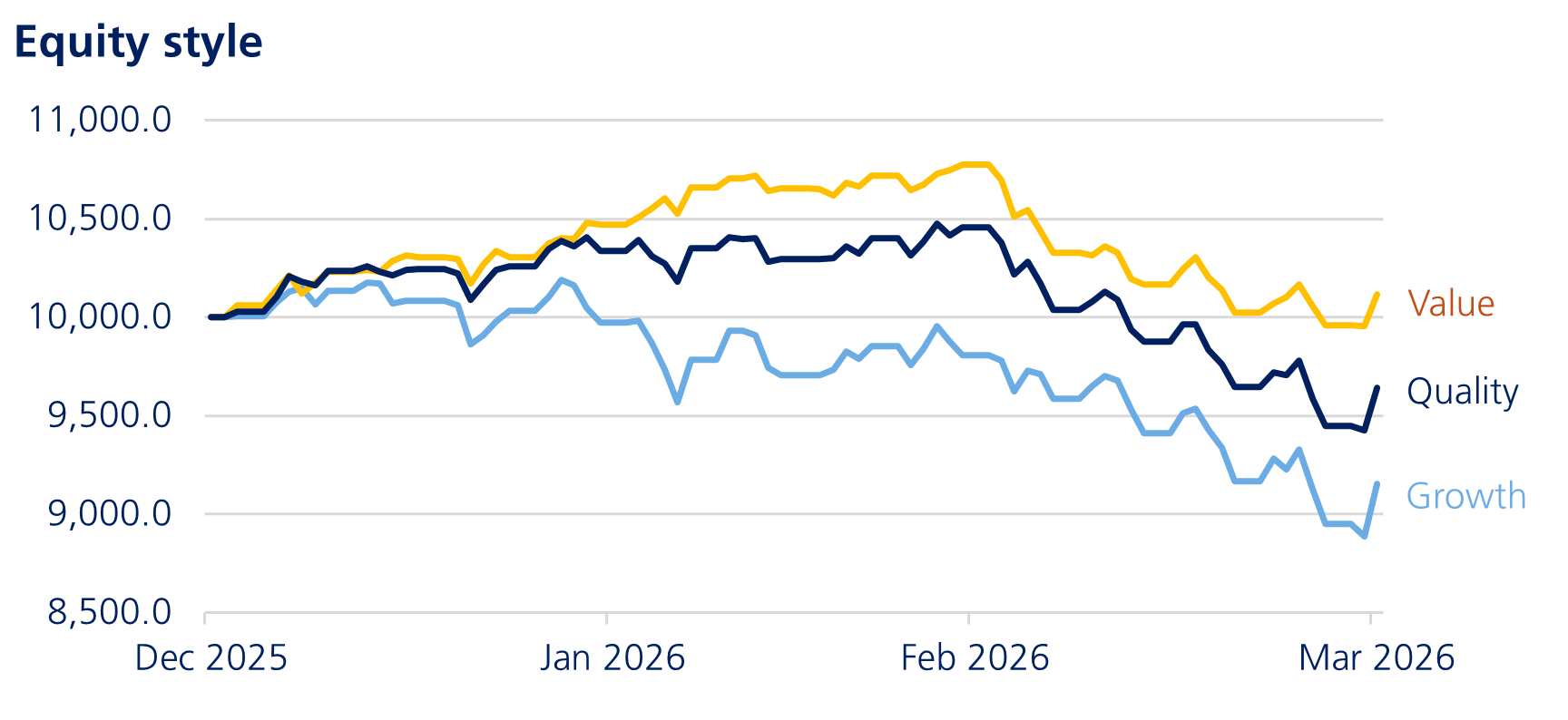

The effectiveness of hedges was tested. While benchmarks were volatile, the moves were even bigger beneath the surface. Significant divergence was experienced across sectors and regions. Within equities as an example, value outperformed growth and quality quite meaningfully. At a sector level, energy materials and utilities were generally positive whilst information technology struggled. Meanwhile regions with a higher dependency on energy imports (Europe) and those exposed to US dollar volatility (EM) were whipsawed, underperforming other regions. At a market cap level, large caps outperformed small and mid caps. After a period of underperformance, the US emerged as the most defensive region given it is a net energy exporter. This was a similar story in fixed income where regional and sub asset class dispersion was high. Parts of the credit market were already experiencing a significant repricing of software risk. While these big shifts within benchmarks made it even more challenging, they did create opportunities to be more selective in allocating and rebalancing.

Environments where correlations are not supportive of diversification are typically where alternatives can be beneficial and provide real return. However, this environment was not necessarily beneficial for all alternatives. A number of hedge funds were caught out by the accelerated cross asset volatility. More specifically, defensive alternatives played a crucial role during the volatility in March, when bond market volatility spiked. Defensive alternatives tend to have more moderate return targets and bond-like volatility profiles and can provide the ballast to portfolios we seek from traditional fixed income with potentially lower correlation.

At LGT Wealth Management, we have embraced defensive alternatives with attractive, reliable and consistent yield to complement the role played by traditional fixed income. As an example, we see opportunities to build long-term core exposures to diversified global infrastructure and private debt as well as investments with limited market and/or economic sensitivity such as insurance/royalties/litigation finance. Additionally, a higher level of dispersion presented opportunities for defensive-orientated hedge funds. Income from some of these strategies presented some dry powder to add to portfolios. Having some liquid alternatives in portfolios is also helpful particularly for rebalancing.

Receive ongoing access to LGT Wealth Management’s insights and observations - a curated stream of thought leadership, market perspectives, and strategic updates designed to inform sophisticated investors.