An update from LGT Wealth Management Australia's Chief Investment Officer Scott Haslem, Nicola Williams and Martin Randall

The outlook for the global economy has entered a period of extreme uncertainty. In late February, the US and Israel began a series of co-ordinated military strikes across Iran. With hostilities extending to the Straits of Hormuz – a vital energy route – global energy prices have risen sharply, while both listed equity and bond markets have also fallen. The conflict is ongoing, and by mid-April there is a risk of non-linear (growth negative) outcomes if we evolve to an energy availability crisis.

Below we briefly discuss our current assessment of this rapidly evolving situation, noting periods of heightened volatility are where truly diversified portfolios across asset classes and return drivers earn their keep. Exposure to unlisted assets is a key aspect of that diversification and in this month’s Core Offerings, we take the time to focus on one of those asset classes, namely secondary investments. We have also reduced risk in our portfolios for a time, trimming our equity overweight and returning our investment grade credit position to neutral.

Secondary investments (secondaries) have moved from niche to mainstream and are now a regular feature in our client conversations. What started as a specialist tool used mainly by large institutions has become a core way of putting capital to work, generating liquidity and reshaping private equity portfolios. Inside, we set out what secondaries are, why they have grown and what this means for portfolios. We highlight why secondaries matter in both closed-end and evergreen structures, why they are more than just a discount story, and why manager selection is critical.

The outlook for the global economy has entered a period of extreme uncertainty. In late February, the US and Israel began a series of co-ordinated military strikes across Iran. In response, Iran has launched a series of retaliatory strikes, targeting US military bases and assets across the region, including in Bahrain, Qatar, Kuwait, Iraq, and the UAE. With hostilities extending to the Straits of Hormuz – a vital energy route – global energy prices have risen sharply, while both listed equity and bond markets have fallen (albeit, arguably only moderately). The conflict is ongoing, and by mid-April there is a risk of non-linear (global) outcomes if we evolve to an energy availability crisis.

Reflecting this, our analysis (albeit with low conviction, but relying on our constraints-based lens) continues to point to a ceasefire emerging by mid-April. However, we are less optimistic on a rapid return to normal flows of energy through the Straits of Hormuz, given disparate military forces and likely residual tension. This has the potential to keep oil and gas prices elevated. How soon the conflict can be de-escalated, and a degree of energy security return, will determine the extent global growth slows, how high inflation pushes and the path of interest rates in the year ahead.

In the scenario where hostilities end before mid-April, and an energy availability crisis is avoided, the outlook for global growth remains upbeat. This reflects the lagged impact of past central bank rate cuts, as well as modest fiscal easing across major economies; pre-war data clearly reveals an emerging credit-led uplift in activity across the globe. Nonetheless, while we expected demand-led inflation to emerge toward the end of 2026 (providing a more challenging backdrop for markets), it increasingly looks like the energy price supply shock has accelerated a more inflationary environment (with faster than expected liquidity withdrawal challenging markets sooner).

This continues to tactically favour equities over fixed income, even with the risk that equity markets deliver more moderate, and potentially choppy, returns over the rest of the year. This month, we have moved underweight Australian equities, reflecting the rapidly emerging risk of a sharp energy availability crisis domestically amid an already-inflationary backdrop and unimaginative fiscal policy support that may put further upward pressure on interest rates. We’ve also trimmed to neutral our investment grade credit overweight. Both decisions reflect a hedge against a more sinister global outcome, and provide firepower to deploy into risk should clarity on the outlook emerge.

For portfolios, ensuring return drivers across a broad range of risk factors, not just equity risk, will be important ahead to ensuring resilience. These periods of elevated volatility and dislocation are both times to trust that our diversified portfolios will weather the market storms, while also seeking opportunities to deploy into those investments consistent with both our multi-polar secular outlook as well as long-lived themes where future demand will exceed supply. These include AI enablers (from picks and shovels and compute to chips and cooling), Energy resilience (from renewables and nuclear to gas and storage), defence and infrastructure (from data centres and real estate to energy).

Private equity is built around long term partnerships, with investors committing capital to specialist managers who acquire and develop companies over several years before exiting. Whilst capital is returned periodically as portfolio companies are sold down, the overall lives of private equity funds ultimately extend beyond a decade. Historically, there was little scope to adjust exposures along the way; private equity secondaries changed this dynamic, and it is now a mature market on its own.

A secondary transaction is the purchase and sale of an existing interest in a private market investment. Instead of committing to a new fund or investment, a secondary buyer acquires a position in a fund or asset(s) that is already part way through its life. The mechanics are straightforward in principle, with the buyer and seller agreeing a price for the given interest, typically expressed as a percentage of the fund’s latest net asset value (NAV). Once closed, the buyer assumes the seller’s remaining obligations, including any future capital calls, and in return, receives all future distributions and any further asset appreciation.

What’s interesting relative to a new fund commitment, is that the buyer has far greater visibility of the fund or assets in question meaning they can review company level performance and form a view on likely exit timing and cash flow profiles. Capital is also typically deployed quicker, and distributions often begin sooner.

Whilst early secondaries were dominated by fund transactions, two broad types have emerged, LP-led and GP-led secondaries, the latter becoming increasingly important. For the avoidance of doubt, LP means Limited Partner, which you can think of as an investor; GP means General Partner, which you can think of as the fund manager.

LP-led secondaries: this is where an existing investor decides to sell one or more fund interests, often to raise liquidity, rebalance exposure or simplify a legacy portfolio. The investor runs a sale process to find buyers, and the positions transfer from one owner to another.

GP-led secondaries: this process is initiated by the fund manager. The starting point is usually an asset or collection of assets in an existing fund that the manager believes still have attractive value creation potential, even though the fund or asset(s) is approaching the end of its life. The firm proposes a continuation vehicle that will hold these companies for longer and existing investors can choose to sell their interests or roll into the new structure; secondary investors provide the capital that funds liquidity for sellers and supports ongoing ownership.

The market’s growth is a direct consequence of the maturing of the private equity market, which has expanded dramatically over the past decade, particularly through large institutions.

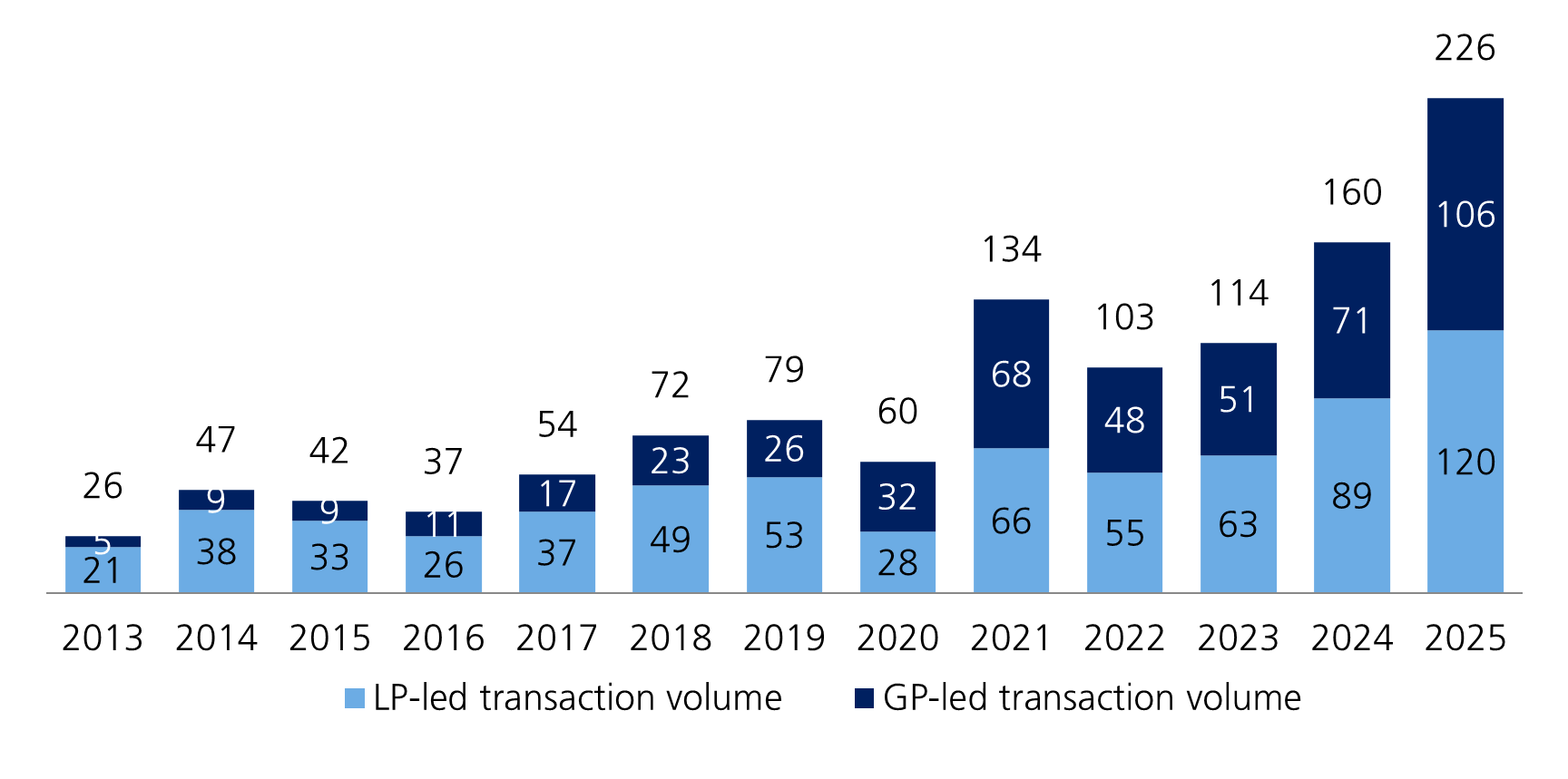

As allocations have grown (2013-2025 as follows), so has their complexity with investors often managing dozens or hundreds of fund/asset positions, each with their own timelines and characteristics, which naturally creates a need for active portfolio management, be it trimming non-core positions, consolidating manager relationships, rebalancing between strategies and adjusting regional exposure. Broader investor circumstances also change whether it be investment team changes, asset allocations changes, regulatory demands or even market swings, which can distort allocations requiring portfolio rebalancing (the so-called ‘denominator effect’). Secondaries are the principal tool for managing invested portfolios in private markets.

From the managers’ perspective, secondaries also address another issue: the mismatch between fixed fund lives and the time needed to create or fully realise value in certain companies. This is where GP‑led secondaries and continuation vehicles (or funds) help bridge the gap.

Secondaries add both flexibility and liquidity to an asset class that is typically neither, and also enables new investors to invest through more seasoned portfolios, with different risk‑return and cashflow profiles than primary commitments – this is particularly relevant to our client segment.

Today, the secondary market is larger, more institutional and more diverse than at any point in its history. Annual global transaction volumes are at record highs, supported by both LP‑led and GP‑led activity. In 2025, there was USD 226 billion in secondaries deal volume globally, up around 40% from 2024 volumes, showing the ongoing growth in the market.

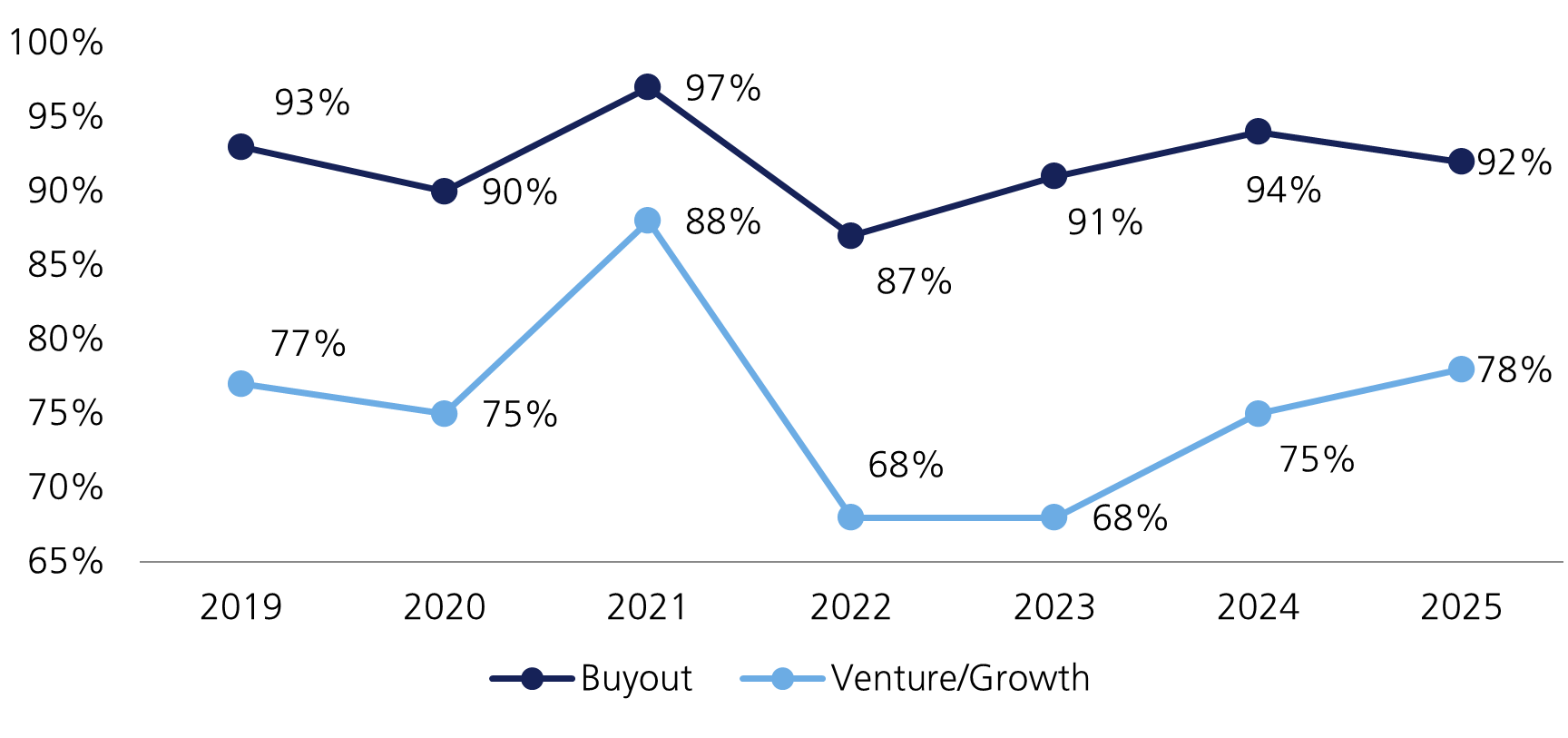

Pricing remains closely linked to the broader macro environment, with secondary transactions generally struck at a percentage discount (or premium) to NAV, reflecting asset quality and risk sentiment in addition to non-investment or complexity factors. In periods of heightened uncertainty, buyers typically demand wider discounts, particularly for older vintages, cyclical sectors and funds managed by less established GPs. By contrast, portfolios backed by high‑quality managers, with resilient cash flows and credible exit pipelines may clear at only modest discounts or even small premiums when competition among buyers is strong. The key point to note here, as shown below, is that pricing can be counter-cyclical, which was certainly evident during the 2022 period (particularly within venture capital/technology) and could come into play should current geo-political tensions continue to heighten volatility across markets.

Beyond LP positions, one of the key shifts in recent years, as shown in Figure 1 (transaction volumes), has been the growing usage of GP-led transactions, a trend that continues to shape how the secondary market operates today. Exit markets have been more muted and primary fundraising more selective with distributions from private equity portfolios running below historical norms. Fund managers seeking to return capital while retaining exposure to their highest conviction assets have made greater use of GP-led continuation vehicles, whether that be a single- or multi-asset (i.e. more diversified) vehicle.

Competition among secondary buyers across the spectrum has intensified in parallel with the growth of the secondary market. Dedicated secondary funds, multi strategy managers and specialist boutiques are all active, bringing sophisticated analytics and deep GP relationships to bear on a much larger opportunity set. For investors, this underlines that secondaries are not a generic, passive exposure; outcomes depend on sourcing, underwriting quality, pricing discipline and governance, and therefore, on careful selection of the secondary managers used in portfolios.

Clearly, secondaries are a very established market utilised heavily by the institutional community, but we think they can play a pivotal role in private client portfolios if done well.

Building seasoned and diversified portfolios

We regularly discuss evergreen funds at LGT Wealth Management, and we often call out that the key innovation is the inbound (not outbound) liquidity, being the ability to invest the desired capital and be fully invested in a diversified, institutionally managed portfolio without the pain it would take to build, and manage, that portfolio using incumbent closed-end (fund) structures.

Here’s where secondaries can play a huge role. In an evergreen or open‑ended vehicle, portfolio managers must balance multiple competing objectives, but primarily, building long‑term exposure to illiquid assets, and managing ongoing subscriptions and redemptions (and appropriate levels of invested capital and cash), the latter within well-defined limits. This requires careful management of investment pacing, diversification and liquidity. Secondaries can help on several fronts:

Accelerating diversification: Secondary portfolios typically span multiple vintages, managers, investment stages and strategies, allowing an evergreen vehicle to achieve broad diversification more quickly than relying on new primary commitments alone.

Smoothing cash flows and NAV evolution: Because capital is deployed into more mature funds and/or assets, cash is deployed (in part) immediately, and distributions often start earlier and are more predictable. This helps reduce cash sitting on the side lines, and in addition to initial discounts (where applicable) results in valuations (NAV) evolving faster relative to new fund commitments or direct asset investments.

Supporting liquidity and portfolio rebalancing: Distributions from more mature secondary portfolios give evergreen funds an additional tool to manage liquidity, not just for redemptions through the cycle but just as importantly, to redeploy into new opportunities as markets evolve. Targeted secondary purchases or sales can also be used to fine‑tune strategy, sector or regional exposures over time.

While one of the most visible features of many secondary transactions is a headline discount to NAV, it can be tempting to assume that a larger discount means a better deal. In practice, the discount is only one part of the story and can reflect many things from underlying risks (e.g. higher leverage, weaker performance or structural issues in the portfolio), so a deep discount may signal genuine concerns, limited remaining upside or challenging exit prospects. Conversely, narrow discounts or even modest premiums can be entirely rational for funds managed by top‑tier firms, backed by resilient, cash‑generative companies with clear exit paths and conservative marks. The key question is whether the price fairly reflects the quality and risk of the underlying assets and the remaining value‑creation potential.

This distinction matters even more in evergreen funds given initial discounts are typically marked up to NAV on completion. In a closed‑end fund, that benefit is shared by all investors in the vehicle, but in an open‑ended structure, new investors (i.e. post-translation) come in at prevailing NAV and thus do not accrue the discount. Put simply, sourcing and underwriting high‑quality companies that can drive returns post transaction is far more important than an initial discount, which is a bonus, and can certainly play a great counter-cyclical role. Many newer evergreen funds have performed very well owing to early discount mark-ups, but as noted the question from here is whether managers have been buying quality or merely chasing discounts; those involved in the latter will likely face disappointment down the road.

This is why thoughtful secondary investing relies on bottom-up underwriting, not just headline pricing. Experienced secondary managers with strong fund manager relationships can add significant value here, as they typically already know the underlying funds and portfolio companies, giving them an information advantage and making them a preferred partner in both LP- and GP-led processes. As an added note, such (experienced) managers can also adeptly manage the governance challenges arising from GP-led secondary processes given the inherent conflicts of interest transitioning assets between vehicles.

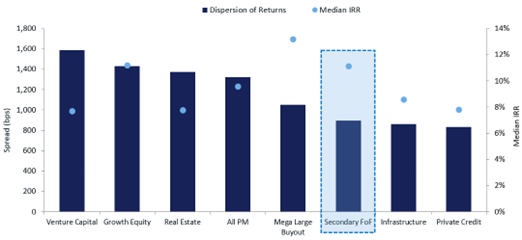

Secondaries have also demonstrated an ability to perform well through the cycle, at or in line with the component parts of private equity, but critically, with lower dispersion of returns (see the chart below). While venture capital and some growth or buyout strategies show a wide spread between top‑ and bottom‑quartile outcomes, secondaries sit towards the lower end of the dispersion range yet still deliver solid median internal rates of return (IRRs). In other words, the gap between the ‘best’ and ‘worst’ secondary managers has historically been narrower than in most other private markets segments, reflecting a more mature market where risks can be evaluated and priced with greater precision (as companies are further along their growth journey).

In an increasingly uncertain investing environment, adding diversity and some potential countercyclicality via an asset class strategy that has historically shown to deliver enhanced risk-adjusted returns is an attractive proposition.

Secondaries have become a core feature of modern private markets, and we believe will increasingly be a particularly powerful tool for private clients. Whether in a closed-end or evergreen structure, secondaries help build diversified, seasoned portfolios, smooth cash flows and support liquidity management in ways that primary commitments alone cannot replicate. Critically, at this juncture, we feel that they provide a means to play offence amidst (1) a private equity market where activity has been challenged in recent years, and (2) a broader market that continues to be impacted by geo-political tensions and other disruptive factors such as AI.

In portfolios, we seek to partner with those (secondary participants) that are deeply embedded in the private markets ecosystem enabling them to appropriately source, underwrite (with an information and execution advantage) and structure transactions across the LP and GP spectrum, whilst also leveraging the secondary opportunity set efficiently alongside both primary and co-investment/direct investments, which is a skill in itself.

While private equity secondaries are the most mature, we are also taking advantage of maturing infrastructure and debt secondaries markets, with the latter an increasingly interesting means to play offence in a private debt market that is coming under increasing scrutiny as discussed in our recent Special Report (Interpreting the private credit cacophony, 2 March 2026).

Receive ongoing access to LGT Wealth Management’s insights and observations - a curated stream of thought leadership, market perspectives, and strategic updates designed to inform sophisticated investors.