Recent market volatility has reminded us of an essential investing rule: don’t panic. If we think back to mid-2024, market consensus would have mostly leant in the direction expressed in our recent CIO monthly titled Staying the course through H2, where our central thesis remains ‘on track’ and we expect lower growth, moderating inflation, and a modest interest rate easing cycle for the next six to 12 months. However, like prior events we have experienced (including those in recent memory, such as conflicts in Russia/Ukraine and Israel/Gaza, as well as the collapse of Silicon Valley Bank), no one can predict these movements of extreme market volatility.

Whilst history can provide a guide to the future, no two events are ever the same, nor are the impacts across different asset classes.

What caused the volatility?

The most recent bout of volatility has been the most extreme since the COVID-19 outbreak in March 2020. What happened is something that may have been broadly identified as a risk, but the impact and timing, along with the magnitude of the market movements, are events that couldn’t have been predicted. Further, whilst history can provide a guide to the future, no two events are ever the same, nor are the impacts across different asset classes.

Initially, markets were unsettled by negative results from 'magnificent seven stocks', followed by softer- than-expected US July non-farm payrolls. This led investors to consider that the risk of recession was greater than previously expected. Added to this was the unwinding of the crowded Japanese yen carry trade. This occurred as the Bank of Japan raised interest rates for only the second time in the past 17 years and signalled an intention to support the yen. This led to further technical selling in equity markets (particularly in Japan and the US), as the cost of borrowing in yen to invest in investments denominated in other currencies (otherwise known as the 'Yen carry trade') rose.

Six business days after the initial market dislocation markets seemed to have calmed. This happened after better-than-expected US weekly jobless claims data was released, suggesting that a recession may not eventuate and the US Federal Reserve may not have to cut rates aggressively, given growth remains robust. So, the market volatility had potentially ended not long after it began. The level of extreme volatility has subsided for now, and for long-term investors, staying the course remains important, not just through the rest of 2024 but well beyond this year. Indeed, signs of slowing US data (as we expected), that will from time to time create market angst, have the potential to foster more frequent bouts of volatility over coming months than may have been the case over H1 2024.

The level of extreme volatility has subsided for now, but for long- term investors, staying the course remains important.

What does 'staying the course' mean over shorter periods and the longer term?

In the short term, we still expect modest rate cuts, so investors should invest as opportunities are presented at both the asset class level and within asset classes. Over longer periods, investors should avoid making investment decisions driven by panic and emotion as a reaction to market movements, and should remain focused on their portfolio’s strategic asset allocation.

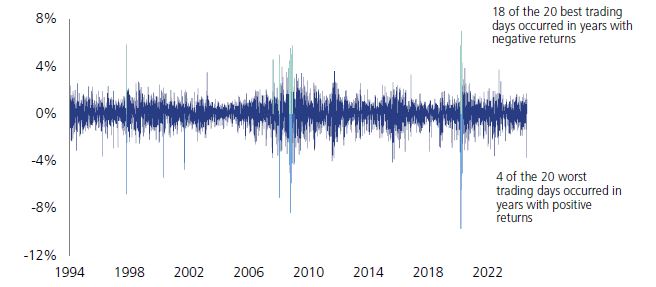

Often, investment decisions based on panic and emotion lead to selling at the bottom of the market, and often these decisions result in the investor failing to reinvest in time to participate in any subsequent market rebound. It can be seen from the chart below that the best and worst trading days occur very close together. The close proximity of the best and worst trading days means that it is difficult to time the market - that means it is difficult to sell at the bottom of the market and buy back into the market before it rallies.

Don’t time the market: The best and worst trading days happen close together

Source: Bloomberg. S&P/ASX 200 Price Index daily returns since 1994. Past performance is not indicative of future returns.

Events over the past couple of weeks remind us of one of the most important investment principles – diversification, particularly across and within asset classes. As equities generally represent the largest allocation (and risk) within a diversified portfolio, this means that investors should ensure there is an adequate allocation to investments that are less correlated to equities. If you have any questions, please contact your LGT Crestone adviser.

This document has been authorised for distribution to ‘wholesale clients’ and ‘professional investors’ (within the meaning of the Corporations Act 2001 (Cth)) in Australia only.

This document has been prepared by LGT Wealth Management Limited (ABN 50 005 311 937, AFS Licence No. 231127) (LGT Wealth Management). The information contained in this document is provided for information purposes only and is not intended to constitute, nor to be construed as, a solicitation or an offer to buy or sell any financial product. To the extent that advice is provided in this document, it is general advice only and has been prepared without taking into account your objectives, financial situation or needs (your ‘Personal Circumstances’). Before acting on any such general advice, LGT Wealth Management recommends that you obtain professional advice and consider the appropriateness of the advice having regard to your Personal Circumstances. If the advice relates to the acquisition, or possible acquisition of a financial product, you should obtain and consider a Product Disclosure Statement (PDS) or other disclosure document relating to the product before making any decision about whether to acquire the product.

Although the information and opinions contained in this document are based on sources we believe to be reliable, to the extent permitted by law, LGT Wealth Management and its associated entities do not warrant, represent or guarantee, expressly or impliedly, that the information contained in this document is accurate, complete, reliable or current. The information is subject to change without notice and we are under no obligation to update it. Past performance is not a reliable indicator of future performance. If you intend to rely on the information, you should independently verify and assess the accuracy and completeness and obtain professional advice regarding its suitability for your Personal Circumstances.

LGT Wealth Management, its associated entities, and any of its or their officers, employees and agents (LGT Wealth Management Group) may receive commissions and distribution fees relating to any financial products referred to in this document. The LGT Wealth Management Group may also hold, or have held, interests in any such financial products and may at any time make purchases or sales in them as principal or agent. The LGT Wealth Management Group may have, or may have had in the past, a relationship with the issuers of financial products referred to in this document. To the extent possible, the LGT Wealth Management Group accepts no liability for any loss or damage relating to any use or reliance on the information in this document.

Credit ratings contained in this report may be issued by credit rating agencies that are only authorised to provide credit ratings to persons classified as ‘wholesale clients’ under the Corporations Act 2001 (Cth) (Corporations Act). Accordingly, credit ratings in this report are not intended to be used or relied upon by persons who are classified as ‘retail clients’ under the Corporations Act. A credit rating expresses the opinion of the relevant credit rating agency on the relative ability of an entity to meet its financial commitments, in particular its debt obligations, and the likelihood of loss in the event of a default by that entity. There are various limitations associated with the use of credit ratings, for example, they do not directly address any risk other than credit risk, are based on information which may be unaudited, incomplete or misleading and are inherently forward-looking and include assumptions and predictions about future events. Credit ratings should not be considered statements of fact nor recommendations to buy, hold, or sell any financial product or make any other investment decisions. The information provided in this document comprises a restatement, summary or extract of one or more research reports prepared by LGT Wealth Management’s third-party research providers or their related bodies corporate (Third-Party Research Reports). Where a restatement, summary or extract of a Third-Party Research Report has been included in this document that is attributable to a specific third-party research provider, the name of the relevant third-party research provider and details of their Third-Party Research Report have been referenced alongside the relevant restatement, summary or extract used by LGT Wealth Management in this document. Please contact your LGT Wealth Management investment adviser if you would like a copy of the relevant Third-Party Research Report.

A reference to Barrenjoey means Barrenjoey Markets Pty Limited or a related body corporate. A reference to Barclays means Barclays Bank PLC or a related body corporate.

Investors across the world have endured a testing first half of 2026! We have dealt with presidential kidnappings, US Supreme Court rulings, wars, oil shocks, inflation, central bank regime changes, and ongoing euphoria/pessimism around the artificial intelligence (AI) revolution.

Special reports

Australian equities – recent underperformance is not enough to reverse our underweight stance

Although Australian equities have delivered an almost 10% total return over the past 12 months, this performance has materially lagged that of equity markets in major developed and emerging economies.

Special reports

Geopolitics, technology, and leadership – in conversation with General Petraeus

A June 2026 conversation with General David H. Petraeus on navigating geopolitical disruption, technological change, and investment leadership in a rapidly shifting world.

Stay up to date

Receive ongoing access to LGT Wealth Management’s insights and observations - a curated stream of thought leadership, market perspectives, and strategic updates designed to inform sophisticated investors.