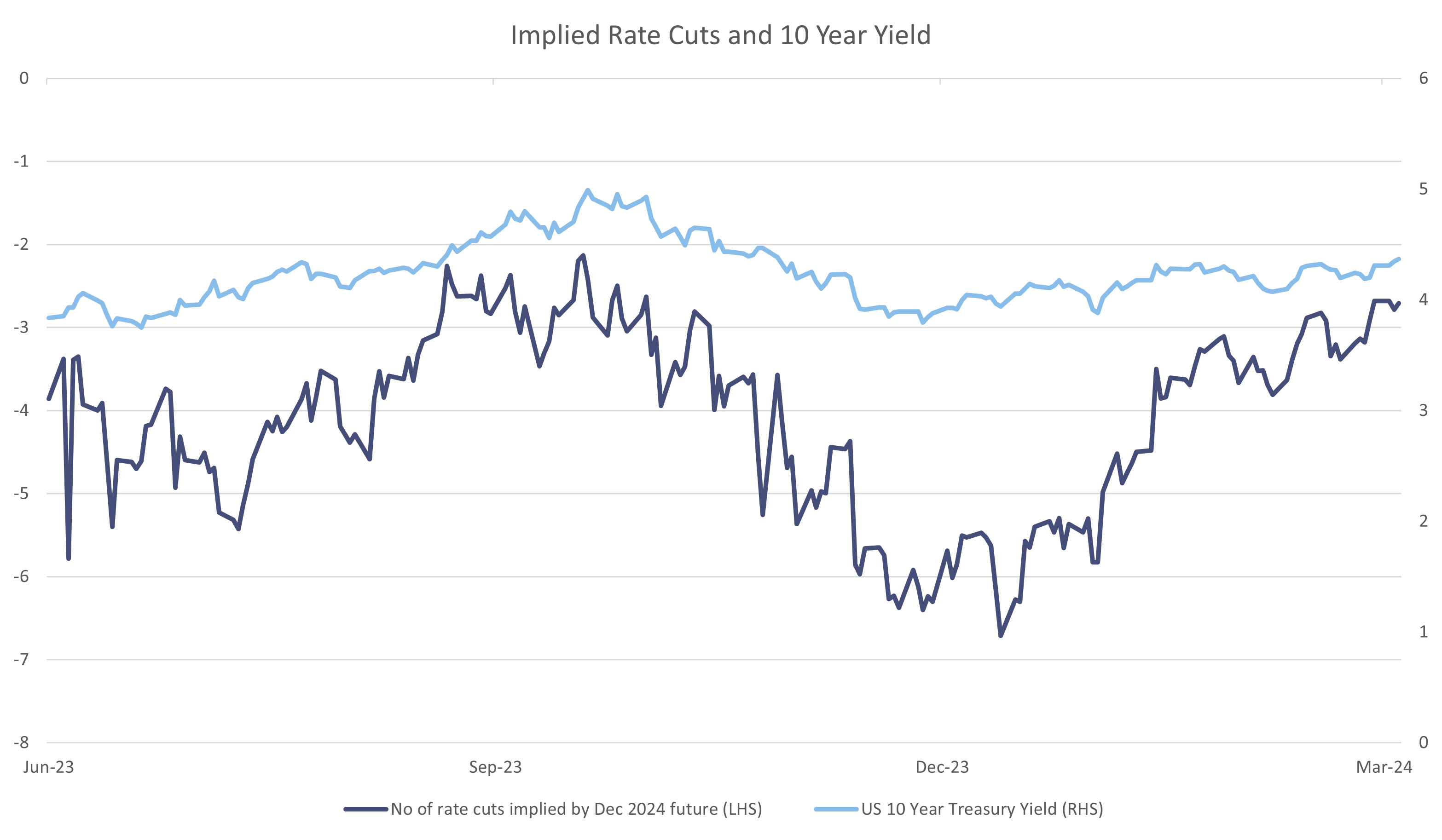

In the first quarter, bond and equity markets decoupled as investors pared back the number of expected interest rate cuts this year, driving a fall in bond prices. When developed market central banks signalled rate cuts are due this summer despite stronger economic and inflation data, equity markets continued to rise.

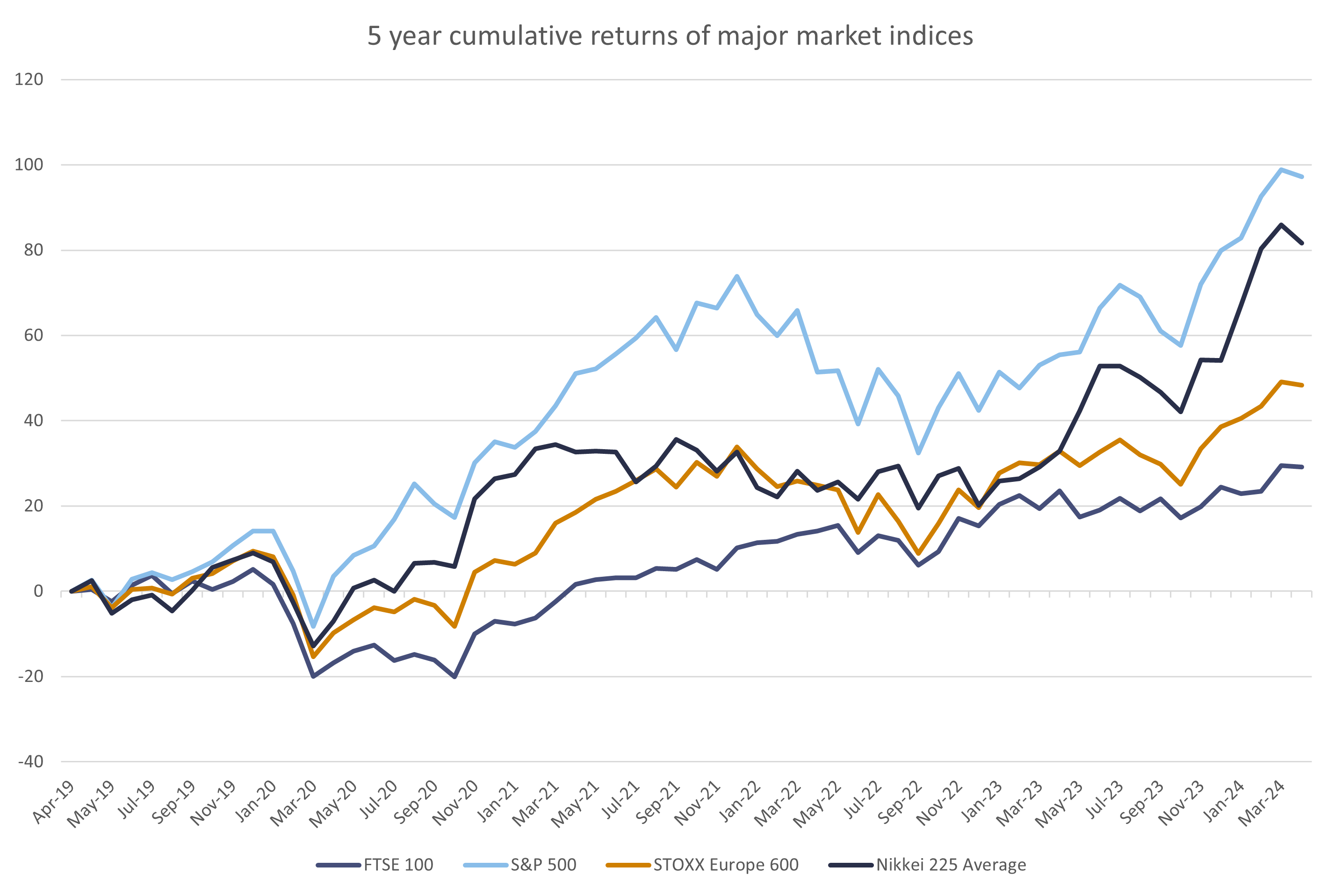

Markets gained confidence throughout the quarter that the Federal Reserve (Fed) had successfully engineered a soft landing, which propelled the S&P 500, Nikkei 225 and the MSCI All-Country World Index to record highs in March.1 Technology stocks benefited from strong fourth quarter earnings, along with soaring optimism surrounding artificial intelligence (AI). The exception was China, as mounting pessimism around its industrial and property sector weighed on index performance. However, recent data indicates the government’s stimulus will likely help activity.

Coming into 2024, investors were pricing in rate cuts of between 1.50% to 1.75% by year-end, compared to the Fed’s own projections of a decline in interest rates of 0.75%. Data continued to show US economic resilience, along with challenges bringing inflation down to the 2% figure, as the rate of disinflation slowed. This prompted material moves in bond markets, and investors priced in fewer rate cuts as the quarter progressed.

Markets are currently pricing in that the Fed will begin cutting rates in June. They will likely want to distance themself from any perceived political interference in what will be a highly charged election year in the US, as President Joe Biden will face Donald Trump in a rematch this November.

Despite this, equity markets motored ahead, as the enthusiasm for AI showed no signs of slowing down. Facebook-parent Meta experienced a historic $197 billion gain in its market capitalisation following its earnings.2 It was the highest single-day market cap increase ever, only to be surpassed three weeks later by Nvidia, which added $277 billion in market cap, bringing its total market value in excess of $2 trillion by the end of the quarter.3 While technology companies led the way, the equity market rally broadened out, with the S&P 500 Equal Weight Index gaining 7.9% and the Russell 2000 up 5.2%.4 This fervour spread to the corporate bond market, with investment grade and high-yield bonds touching multi-year lows.

European stocks also experienced a strong first three months of the year, with the EuroStoxx 600 rising 7.9% in the quarter. The FTSE 100 posted strong performance in March, benefiting from rising commodity prices, but only rose 4% in the quarter.5

In the UK, Chancellor Jeremy Hunt’s spring budget was a non-event, despite Conservatives using it as a platform to entice their electorate. The UK economy is poised to recover as headline inflation fell to 3.4% in February and is forecast to fall closer to 2% in the second quarter, which should pave the way for the Bank of England (BoE) to begin its own interest rate cutting cycle.

The most noteworthy central bank action in the quarter came from the East, with the Bank of Japan (BoJ) abandoning its negative interest rate policy and recalibrating its asset purchase programme. The hike was well telegraphed, given strong wage growth data. However, the dovish tone from BoJ members meant that the yen remained weak. Local equity markets continue to experience a resurgence, with the Nikkei 225 reaching an all-time high in March, surpassing the previous high in 1989.6 Enthusiasm for stock exchange structural reforms and increased domestic participation helped equities perform strongly.

China continues to adopt a strategy of targeted fiscal loosening and outlined its optimistic 5% growth targets, which failed to convince investors. Economic data remains mixed as the economy suffers from property malaise. However, given lower valuations and strong rhetoric from Chinese officials, Chinese and Hong Kong-listed equities pared earlier losses in the second half of the quarter.

Throughout the first three months of the year, investors gained confidence that inflation will move closer to target levels without triggering a deep global recession. This in turn lifted equities and corporate bonds. Risks remain that a rate cutting cycle will be pushed further out, thus keeping borrowing costs elevated and weighing on profitability. We therefore retain our preference for quality companies with resilience business models, low debt levels and positive cashflows.

[1] Bloomberg

[2] Bloomberg

[3] Bloomberg

[4] Bloomberg

[5] Bloomberg

[6] Bloomberg

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.