As events continue to unfold in the Middle East, we are reminded how precarious the geopolitical landscape is. Market participants are closely watching Israel’s reaction following Iran’s drone strikes last weekend. Israel, supplied with intelligence from the US, UK and other allies, was able to thwart Iran’s attack. Early Friday morning, Israel launched a missile strike inside Iran. The conflict in the Middle East, along with the war in Ukraine and simmering tensions between the US and China, mean geopolitical risk will remain heightened for the foreseeable future.

While markets have become increasingly jittery over potential escalation, these pockets of volatility tend to fade as potential outcomes narrow and become clearer. Long term, financial markets are more impacted by trade challenges and supply chain issues, which are slow to materialise but become more pronounced over time.

As we examined in our Brief on Chinese and European electric vehicles, China’s dominance in the global electric vehicle (EV) market threatens Europe’s own EV sector. This led the European Union to launch an anti-subsidy investigation into Chinese EV imports and concerns over unfair competition.

It’s not just EU members expressing concern over cheaper Chinese EVs flooding the market. US Treasury Secretary Janet Yellen, a long-time supporter of global trade and cheap manufacturing goods, has changed tack and expressed concern that China is making too many goods which could hurt the US and global economies.1 If Yellen’s warnings fail, and China continues to oversupply markets, this could lead to a new wave of protectionism as the US and Europe defend their local economies by placing higher tariffs on Chinese products. Yellen and the Biden Administration are particularly concerned about the clean energy and semiconductor sectors, two industries supported by US fiscal measures to encourage domestic investment. Despite all the efforts the US has made, it may not be enough to keep up with China, ultimately creating a race of who will dominate these newer industries.2

By attempting to corner the EV market with brands such as BYD, the impacts of China flooding the market are already being felt by Tesla, which announced earlier this week it would be cutting more than 10% of its global workforce, or about 14,000 employees.3 Days after the job cuts were announced, Tesla asked shareholders once again to approve Elon Musk’s record-breaking $56 billion pay that was set in 2018, after a Delaware judge rejected the pay package in January, calling it an “unfathomable sum”.4 This sentiment will undoubtably be shared by Tesla’s employees. Telsa, along with other US heavyweights, has been a poster child for American ingenuity and its challenges underscore the effects of strategic competition. This has important ramifications for investors and perhaps prompted President Joe Biden’s calls for tripling tariffs on Chinese steel and aluminium.5

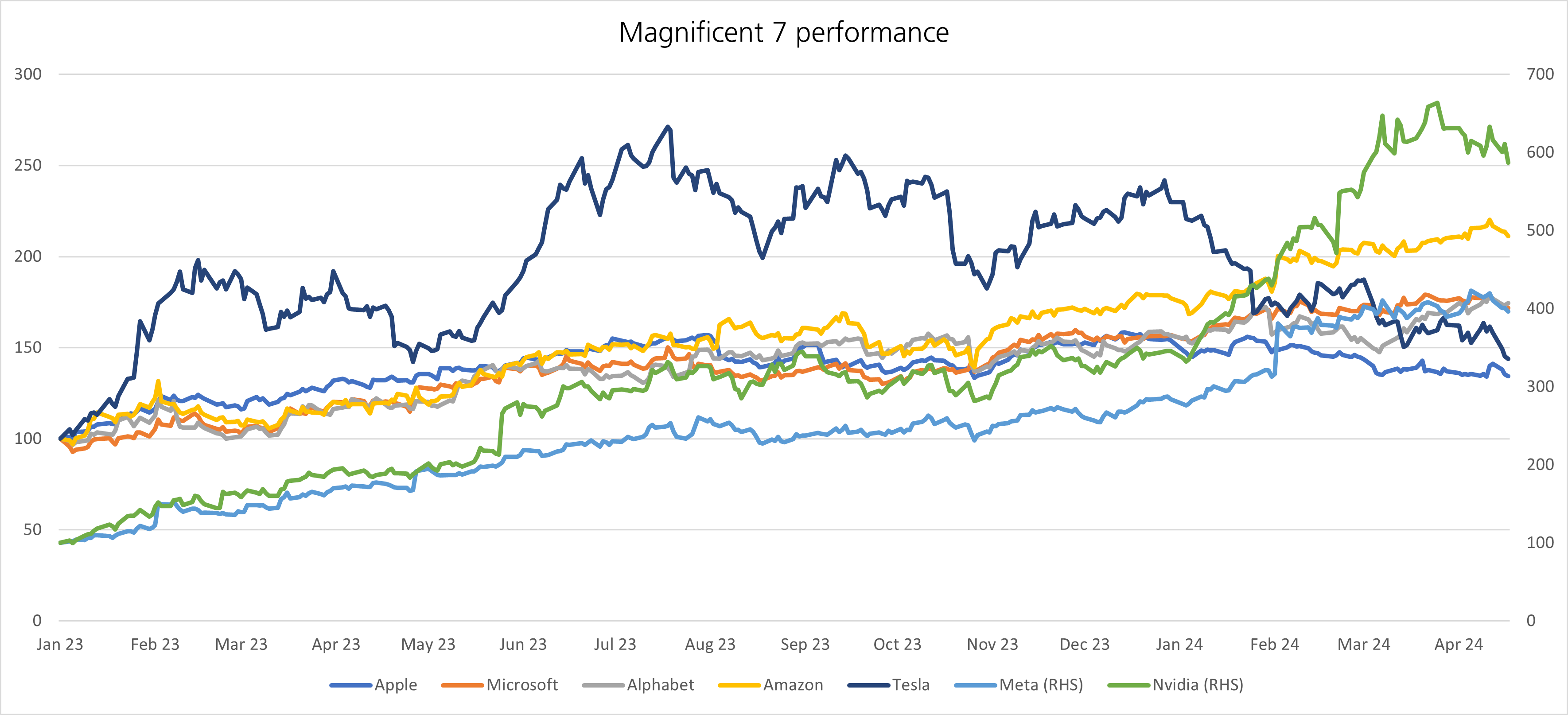

Last year’s meteoric 104% rise for Tesla now seems a distant memory. Shares this year are down 37%,6 and the ongoing pressures facing Musk’s company have left many to question whether Tesla should even be included in the so-called Magnificent 7 stocks.

While geopolitics drive markets short-term, global trade frictions will have a greater impact on investors with a long-term investment horizon. Understanding companies’ barrier to entry, heightened competition, and regulatory developments designed to stimulate domestic sectors at the cost of foreign companies will be crucial. Through our deep, fundamental research into underlying companies, we are able to help build long-term portfolios able to withstand various shocks.

[3] NYTimes, https://www.nytimes.com/2024/04/15/business/tesla-layoff-elon-musk.html

[4] Guardian, https://www.theguardian.com/technology/2024/apr/17/elon-musk-tesla-pay

[5] BBC, https://www.bbc.com/news/business-68838063

[6] Bloomberg

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.