In June, we published “A familiar shock, different markets: Oil and the Israel-Iran conflict”, noting that while the “12 Day War” in June 2025 raised memories of Russia-Ukraine and the 1970s oil shocks, there were two key differences: no major oil infrastructure was targeted, and Iran had not closed the Strait of Hormuz, the 21-mile-wide shipping lane that carries 20% of global oil daily. At the time, US objectives were narrowly focused on limiting Iran’s nuclear capabilities, which helped contain market impact.

The situation has escalated, with strikes on energy infrastructure and a blockade of the Strait. Yet even amid heightened tension and short-term volatility, investors can draw reassurance from dynamic global energy markets, diversified supply chains and the long-term strength of high-quality companies.

The US-Israeli-led air and missile strikes against Iran, which began two weeks ago, continue to target military sites and regional infrastructure. The Strait of Hormuz remains closed, despite the White House offering insurance and escorts to tankers, and China, Iran’s top trading partner, calling for all sides to protect the shipping lane.1 In response, on 11 March, the International Energy Agency coordinated the largest strategic oil reserve release in history, with 400 million barrels expected to reach the market, equivalent to around 20 days of supply through Hormuz.2

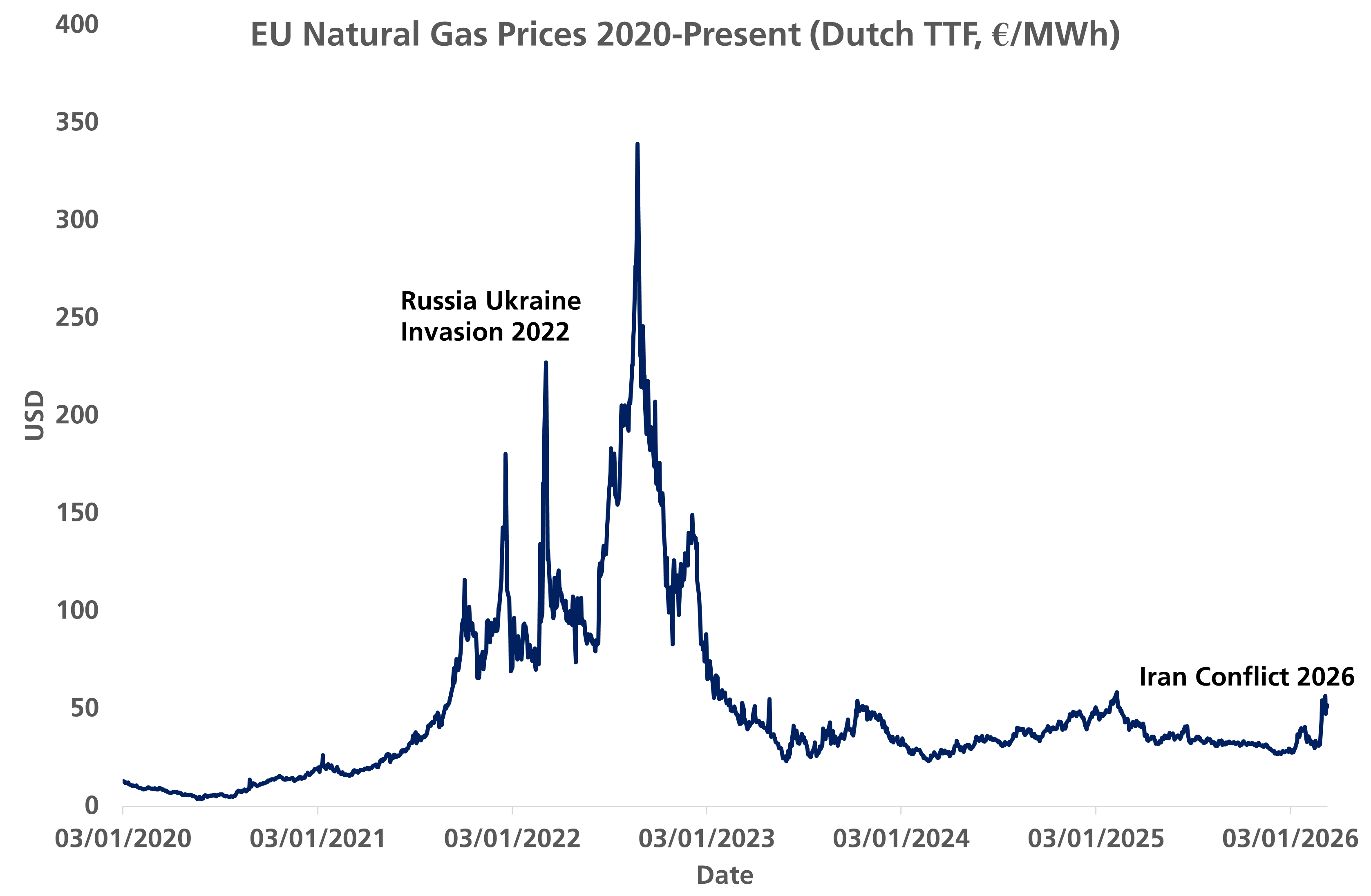

Iranian infrastructure strikes are more disruptive in the short-term than long-term, with the most notable attack on Qatar’s LNG Ras Laffan facility, responsible for 20% of global LNG supply. It has suspended operations since last week, driving gas prices in Europe up by over 60%. While much remains uncertain, it is clear the longer the conflict continues, the greater the risk to critical oil infrastructure in the Gulf.

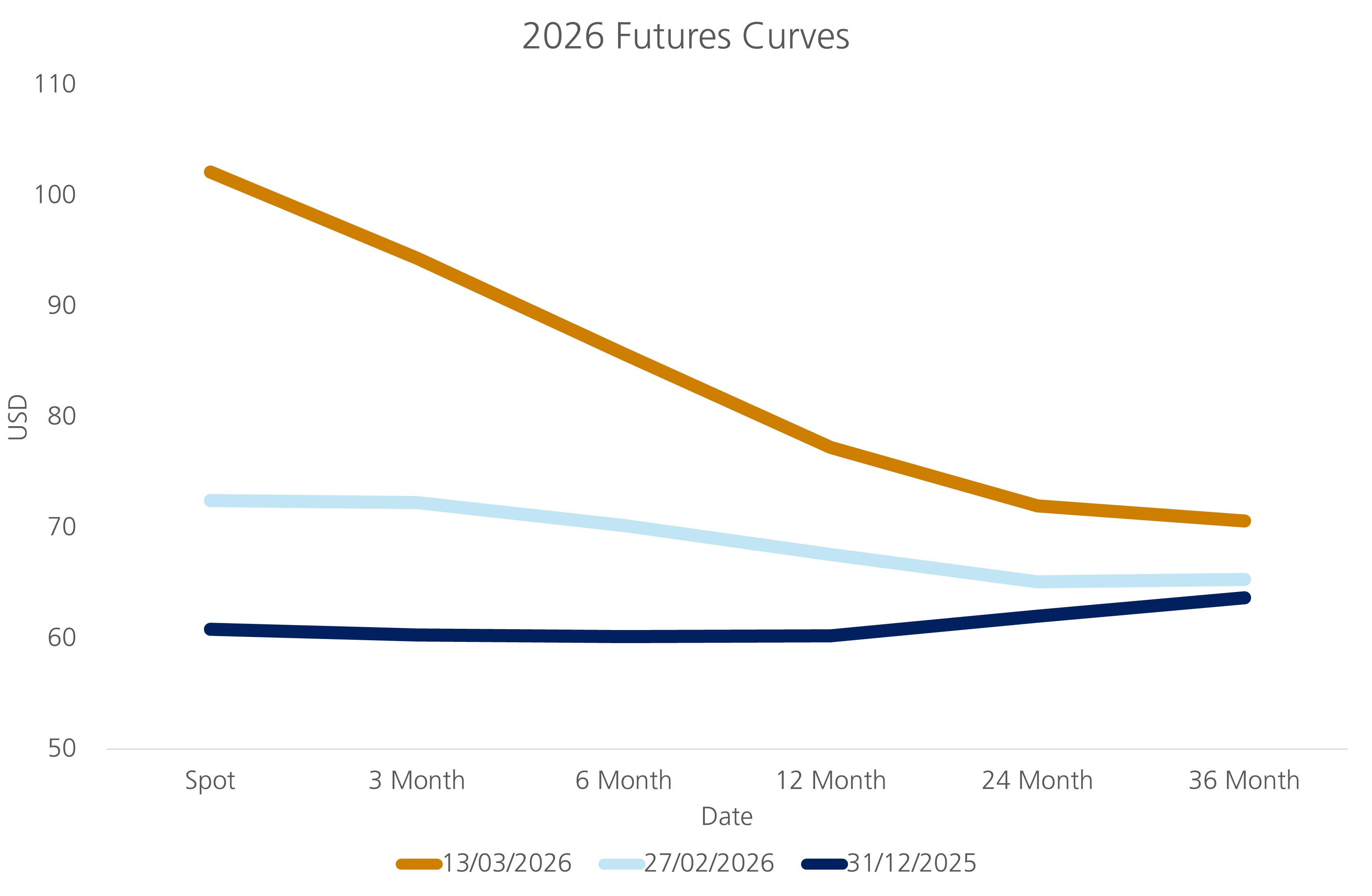

The scale and impact on oil markets have already eclipsed last year’s 12 Day War. This is evident from Iran targeting neighbouring Gulf states and blockading the Strait of Hormuz. Oil prices have risen from $62 per barrel at the start of the year to $72 the Friday before the conflict began, and now $102 as of writing.

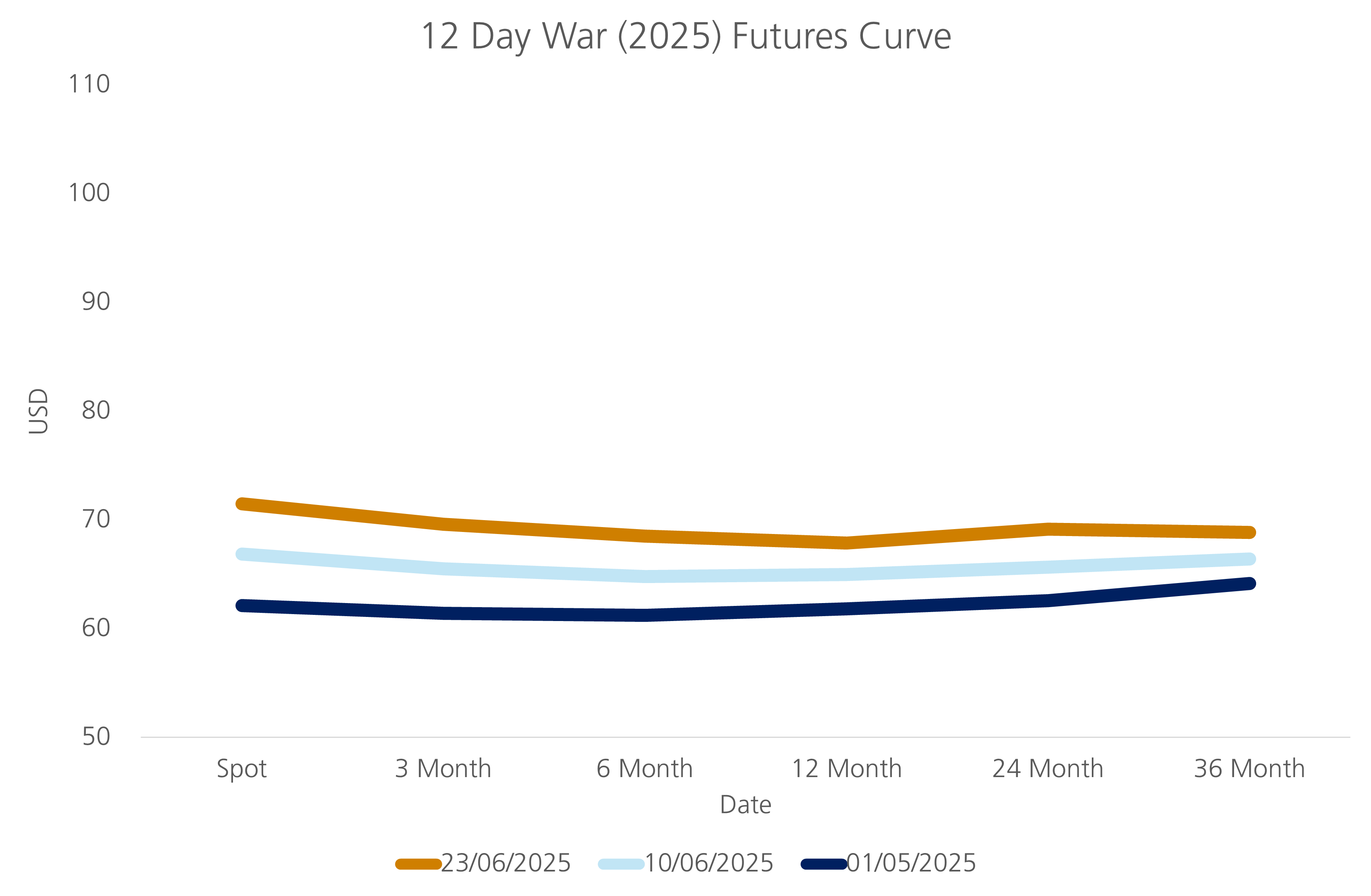

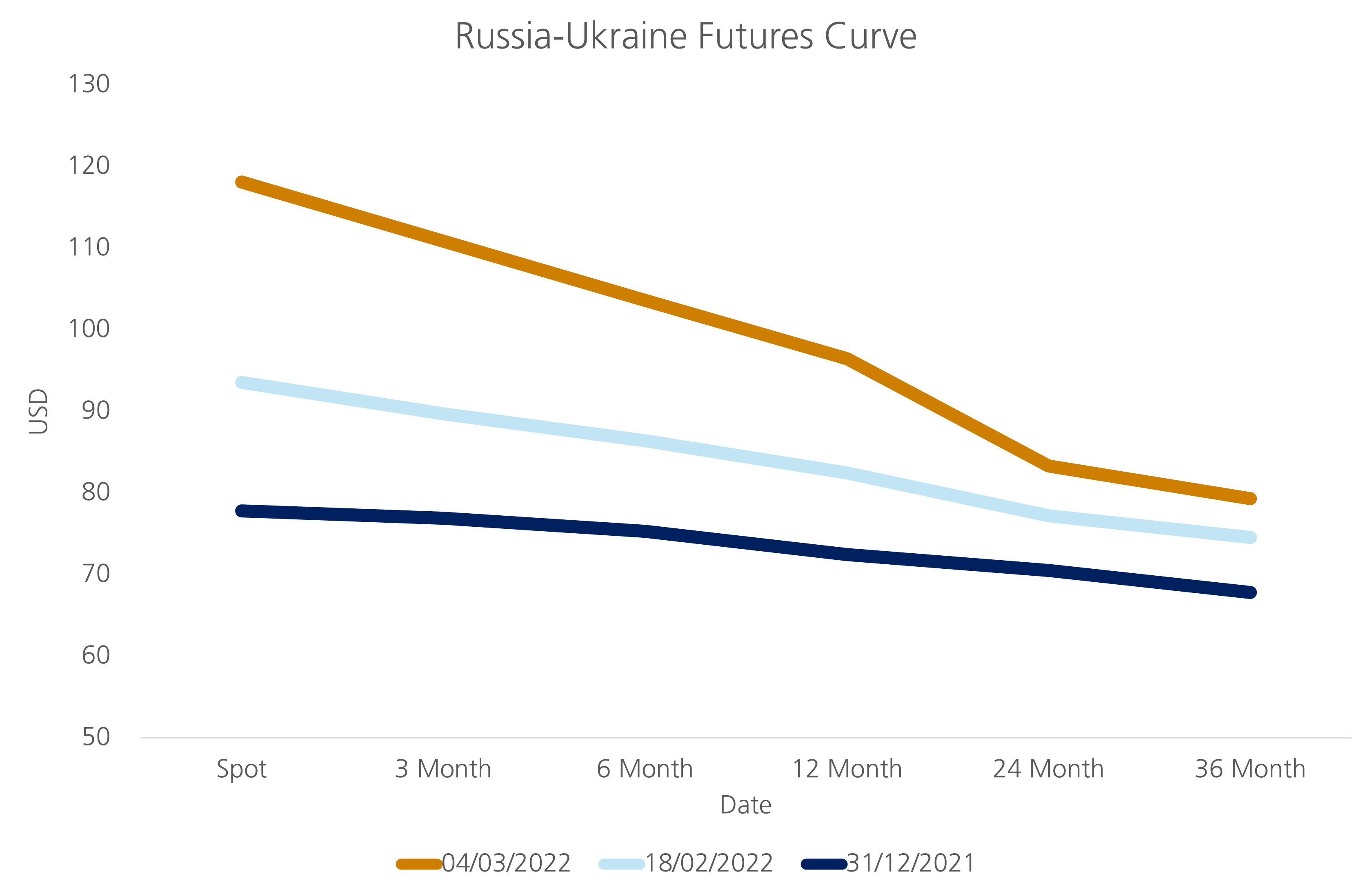

Oil price moves appear more akin to Russia-Ukraine ($40) than the 12 Day War ($9). A more nuanced view comes from looking at the price of oil for delivery in the future – the so-called “futures curve”. The headline “spot” price of oil reflects the supply and demand for oil today, while the “futures curve” reflects what the market believes conditions will be in up to three years’ time. Expectations have not changed as drastically. In fact, the price of oil for delivery in 12 months has risen $17 since the start of the year to $77/barrel, and in 36 months, it is just $7 (to $70/barrel). In other words, markets are pricing in short-term oil flow disruptions rather than long-term supply issues.

One reason oil and natural gas prices have not surged dramatically is that energy supplies are more diversified today than they were in the 1970s. Oil production is no longer concentrated in just a handful of Middle Eastern countries, with significant output now coming from the US, Brazil, Canada and other non-OPEC producers. Furthermore, European countries are less dependent on Middle Eastern supplies than they were on Russian gas in 2022.

The rise of US shale has also added flexibility. Strategic petroleum reserves, sophisticated futures markets and alternative transport routes also provide additional buffers. Short-term regional conflicts may cause price spikes, but the global energy system is structurally better insulated from prolonged supply shocks than the past.

While the situation has led to energy market volatility, major markets have broadly remained orderly. Government bond prices have declined, as rising energy prices increase the risk of persistent inflation. UK gilts have been particularly sensitive as the UK is an energy importer.

Equities have declined, but the moves have been relatively contained. Emerging markets are among the weakest performers due to their reliance on imported energy. But this follows strong performance. Developed markets have fallen but to a lesser extent. During these times, it is important to remember that the underlying investment case for these holdings remains intact, and periods of volatility often create opportunities for active managers to identify high-quality companies trading at more attractive valuations.

While forecasting outcomes in a rapidly changing situation is challenging, it can help to consider incentives.

For the US-Israeli coalition, President Trump’s goal of eliminating threats is a clear objective. However, in addition to deep reservations in the US about deploying “boots on the ground”, higher long-term energy prices are deeply unpopular among Americans. This indicates that a shorter conflict is more desirable. Under this scenario and assuming Hormuz reopens with limited damage, energy prices would likely drift lower, provided peace holds.

On the Iranian side, objectives are difficult to analyse, not least because the leadership prior to the outbreak of the conflict was mostly eliminated in the early strikes. Furthermore, figures in the country and military naturally have not made their goals public. Mojtaba Khamenei, the son of Iran’s Ayatollah Ali Khamenei, who was killed in the strikes, has been chosen as his successor. Unlike his father, he has kept a low profile.3 The Iranian regime appears incentivised to prolong the conflict and inflict an energy price squeeze to accelerate the US-Israeli coalition to the negotiating table. Iran has the advantage here: while US-Israeli military capabilities are superior, it is far simpler and cheaper to launch a missile or drone strike than it is to intercept one. Replacing energy infrastructure is also complex and expensive, further raising the cost if Iran pursues this strategy.

The Prussian military strategist Carl von Clausewitz once wrote that “in war more than anywhere else, things do not turn out as we expect.” War involves a volatile mix of chance, independent actors and chain reactions. Predicting the outcome is therefore impossible. As such, the most important quality for a commander, or indeed an investor, is not forecasting, but perseverance and resilience.

Disciplined investing, attention to incentives, and a long-term perspective remain the best tools to navigate shocks. Even in turbulent times, opportunities exist for those who remain patient, adaptable and committed to resilient strategies.

[1] U.S. Gas Prices Jump for 11th Straight Day, and Oil Pushes Higher - The New York Times

[3] Who is Mojtaba Khamenei, Iran's new supreme leader? - BBC News

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.