Although there was one full month of the Iran war impacting first quarter 2026 earnings, most companies reported strong earnings. In fact, the quarter has been surprisingly robust, with sales growth of over 10% for the 408 companies in the S&P 500 that have reported so far. That is an acceleration from the 9% growth the S&P 500 saw in the fourth quarter of 2025 and more than double the 5% growth in the first quarter of 2025.

All 11 broad S&P 500 sectors saw revenue growth of over 4%, and eight had more than 10% sales growth, with the IT sector seeing its revenue rise by a quarter. There were two equally valid narratives about earnings.

Firstly, the world’s largest companies – many of them technology-led – have continued to accelerate sales growth. This directly challenges the metaphor that “elephants don’t gallop” – in other words, the idea that very large, mature companies are expected to grow slowly because their size makes rapid expansion difficult. While we wait for the biggest of the big beasts, AI chip designer Nvidia – which has surpassed $5 trillion of market capitalisation once more – to report its earnings, the next largest companies – Apple, Alphabet, Microsoft, Amazon, Meta, and Broadcom – each increased revenue by 17% or more in Q1 2026 compared to the same prior year quarter. All these companies had higher yearly growth rates than Q1 2025, with many of the growth rates more than doubling.

In terms of dollars added, the group added twice as much in quarterly revenue ($95 billion) as they did the previous year ($44 billion). This is just as well, given Alphabet, Microsoft, Amazon and Meta increased their capital expenditure from $71 billion this time last year to $129 billion just in the first quarter, with the vast majority going towards artificial intelligence. Accelerating revenue is clearly a good sign, however, it is worth remembering that growth also accelerated in a similar manner five years ago, and it is still too early to conclude if current growth fully justifies the stratospheric rise in capex. That’s because, while revenue is expanding at faster rates, capital expenditure has accelerated even more aggressively, and the returns on that investment remain uncertain and delayed.

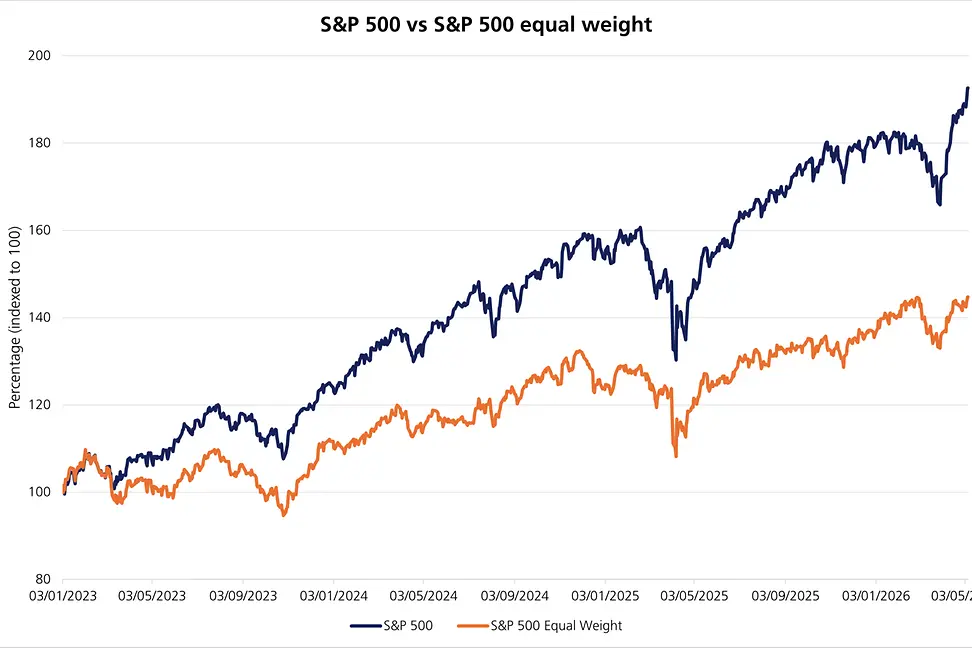

The story of the last three years has been that the largest ‘mega-cap’ tech companies, as detailed above, have driven most of equity market returns. From 2023 to 2025, the market-capitalisation weighted S&P 500 – where larger companies have a larger impact – posted double the total return of the equal-weighted S&P 500, in which every company counts the same.

This leads to the second point. Even if technology is leading other sectors in terms of sales and earnings growth, it is acting as a rising tide lifting all boats, with broad-based revenue and profit growth now evident across most sectors. Sectors as diverse as consumer staples, consumer discretionary and utilities all saw more than 10% revenue growth in the first quarter.

It is early days, but the signs in the first quarter indicate that this broader revenue and earnings growth is feeding through into share price performance, as the equal- and market- capitalisation S&P 500 indices are performing almost exactly in line with each other. The elephants may still be galloping, but the other animals are finally managing to keep pace.

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.