A week is a long time in politics, as Harold Wilson observed – and this held true for the Labour Party this week. Recent events in Westminster, including debate over the government’s vetting of former US ambassador Peter Mandelson, have raised questions about the government’s leadership and contributed to political uncertainty ahead of May’s local elections, during which around 30 million voters across the UK will head to the polls.

In Scotland and Wales, voters will elect their devolved parliaments, while in England, a range of major cities and county councils will hold elections. Current polling suggests that, for the second year in a row, Labour and the Conservatives are unlikely to secure a top two position in vote share or seats won.1 This could result in increased representation for smaller parties, including Reform, the Green Party and the Liberal Democrats.

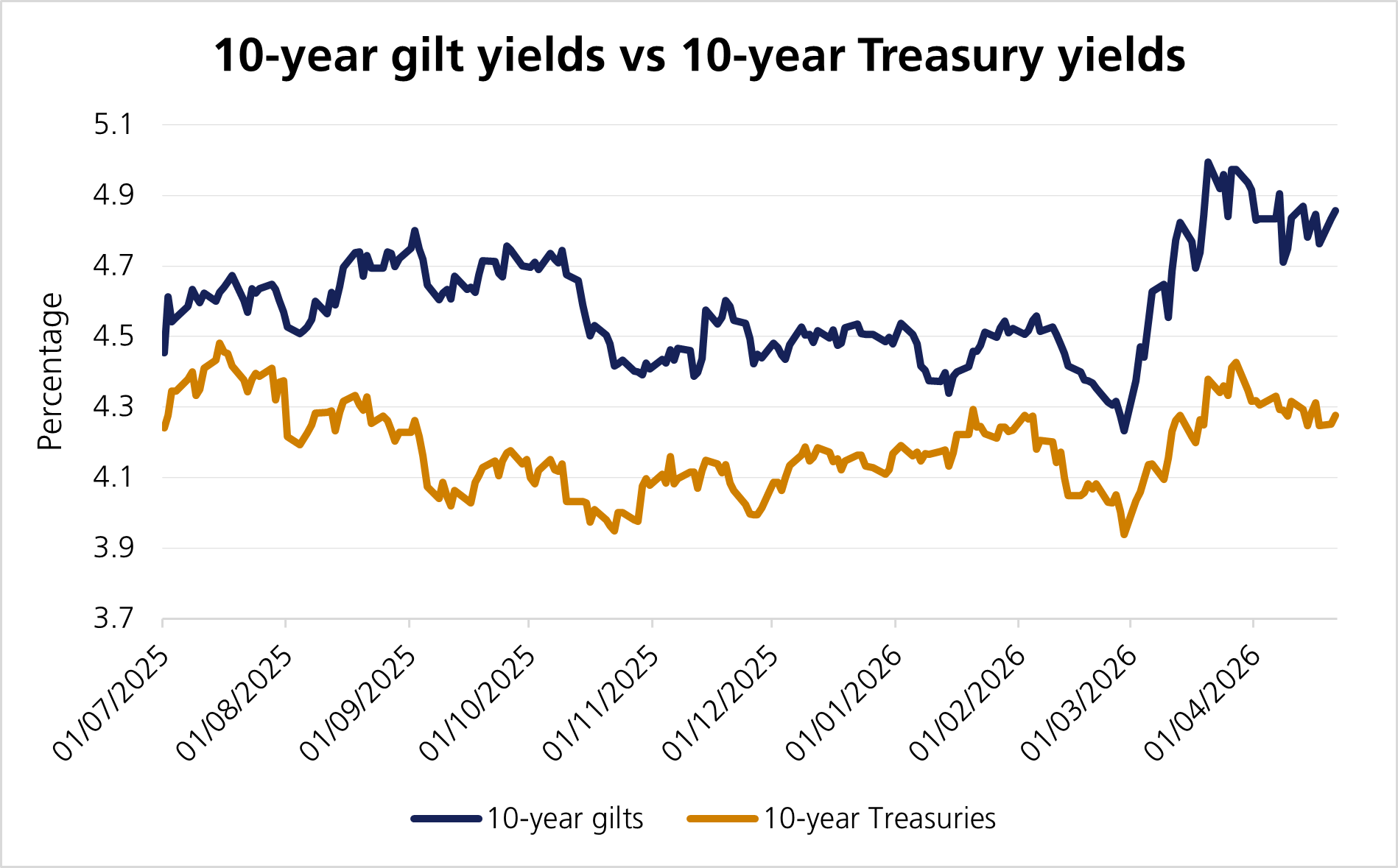

Ever since Liz Truss’s mini-budget in 2022, gilt yields have shown increased sensitivity to political shocks, and the UK’s latest political uncertainty has pushed them higher once again. Labour’s budgets have also influenced government bond yields, as Chancellor Rachel Reeves’s fiscal rules have prioritised fiscal prudence over policy flexibility, making markets more sensitive to unexpected developments.

While many expected the November 2025 budget to include income tax increases, the final measures focused on more subtle tax adjustments with slightly increased fiscal headroom. This, coupled with lower inflation and a period of relative political stability, meant that from October to February, gilt yields declined more than US Treasury yields. This was further supported by expectations that the Bank of England (BoE) would cut interest rates. As a result, gilts were among the best-performing bond markets globally over this period, until the war in Iran disrupted the outlook.

Expectations for BoE rate cuts quickly shifted to a prolonged pause, with some pricing in rate increases, as the ongoing war in Iran has pushed UK energy costs higher. Earlier this week, the Office for National Statistics (ONS) showed that UK inflation rose from 3% to 3.3% in March, upending deflationary trends.2 Against this backdrop, the International Monetary Fund (IMF) revised its growth forecasts, stating in its latest World Economic Outlook that the UK economy will only expand by 0.8% this year, a marked downgrade from earlier projections of 1.3% and one of the largest downward revisions among its developed market peers.3 This illustrates how exposed the UK is to disruption in the Strait of Hormuz.

The combination of a more uncertain domestic political environment and an economy facing renewed supply-side pressures has increased the premium investors demand for holding British government debt.

Investors’ shifting perception of gilts continues to drive sharp swings in UK debt relative to other developed market peers. This reinforces international investors’ view that gilts are increasingly suited to a short-term trade rather than a long-term investment opportunity. However, the resulting premium allows nimble investors to lock in gilt yields at higher levels. Although shifting perceptions could result in meaningful price movements in both directions, for taxable clients who benefit from favourable capital gains treatment of gilts, this volatility may offer an opportunity for investors to buy longer-maturity gilts at higher yields.

The table below shows UK government bonds with different maturities, and what prospective returns investors can broadly expect depending on rising or falling interest rates. It illustrates that over one year, the starting yield provides a meaningful cushion even if yields move higher over the coming weeks and months.

In this environment, disciplined position sizing and a focus on time horizon remain key when considering opportunities across the gilt curve.

| 1yr Return UK Gilts | ||||||

UK | Starting yield | +1.5% | +1% | +0.5% | -0.5% | -1% | -1.50% |

2Y | 4.25 | 3.0% | 3.4% | 3.8% | 4.6% | 5.1% | 5.5% |

5Y | 4.36 | -0.8% | 0.9% | 2.6% | 6.1% | 7.9% | 9.8% |

7Y | 4.57 | -2.8% | -0.4% | 2.0% | 7.2% | 9.8% | 12.6% |

10Y | 4.86 | -4.9% | -1.8% | 1.5% | 8.4% | 12.1% | 15.9% |

30Y | 5.56 | -12.8% | -7.3% | -1.2% | 13.0% | 21.4% | 30.7% |

Source: Bloomberg

NB: This table is based on hypothetical yield scenarios, showing increases and decreases to gilt yields of 0.5%, 1% and 1.5%, and is for indicative purposes only. Past performance and simulated returns are not a reliable guide to future performance. The value of gilts may fall as well as rise.

[1] Local elections 2026: polls, predictions and areas to watch

[2] Office for National Statistics

[3] World Economic Outlook, April 2026: Global Economy in the Shadow of War

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.