Gilts are a long-established part of financial markets, but the term is not always widely understood outside financial circles. In simple terms, they are bonds issued by the UK Government, and in the right circumstances they can play a useful role for investors seeking a defined term, a known maturity value and, in some cases, a more tax-efficient return.

A gilt is a bond issued by the UK Government to finance its spending plans. It pays a fixed level of interest and, at maturity, repays its par value of £100. If a gilt is bought below the £100 par value and held to maturity, the return comes from two sources: the coupon, which is the fixed interest payment, and the difference between the purchase price and the £100 repaid at maturity. The annual return if held to maturity is known as the yield to maturity (YTM), which takes both elements into account.

For gilts bought below face value and held to maturity, the return profile is relatively straightforward, as the Treasury is expected to repay £100 per unit at maturity. Backed by the UK Government, gilts are widely considered a lower-risk part of the market, and can offer investors greater visibility over returns across a one- to five-year horizon, although it is important to note that market prices may fluctuate before maturity.

Gilt portfolios can be structured in several ways: either a single bond can be bought or a ladder of several bonds can be structured. They are often considered in situations where individuals wish to set aside capital for a known future need, such as a future tax payment or school fees, to hold surplus cash more efficiently or to structure maturities across different dates.

For individual investors, gains on UK gilts are exempt from capital gains tax. By contrast, the coupon is taxed as income, based on the investor's usual marginal rate. That is an important distinction. A low-coupon gilt bought below its £100 maturity value may produce only a small amount of taxable income, while a larger part of the return comes from the gain between the purchase price and the amount repaid at maturity. In other words, a low-coupon bond bought below its face value and held to maturity can deliver most of its return free of tax altogether.

For certain UK investors, especially those paying higher or additional tax rates, this combination means that UK gilts may offer a more tax-efficient outcome than a cash deposit offering a similar headline yield.1 With yields at their highest levels in over fifteen years, this can provide an attractive opportunity in the right circumstances.

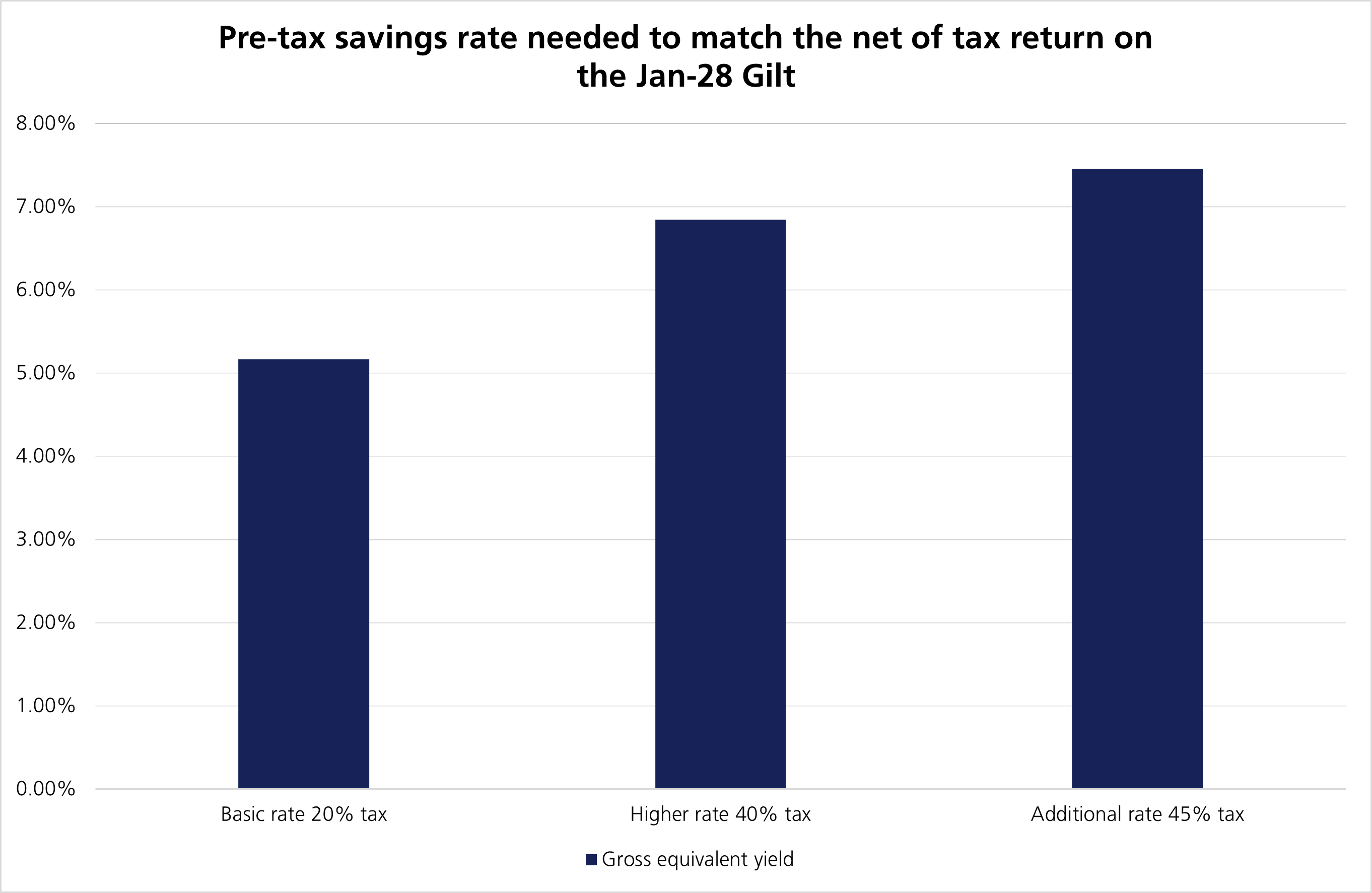

A practical way to compare a gilt with a cash deposit is to look at the gross equivalent yield (GEY). This clearly demonstrates the interest rate that a taxable savings account would need to offer to match the after-tax return of a gilt. For higher-rate taxpayers, this gap can be meaningful – the higher the marginal tax rate, and the lower the gilt's coupon, the larger the gap between a gilt's headline yield and its equivalent cash rate.

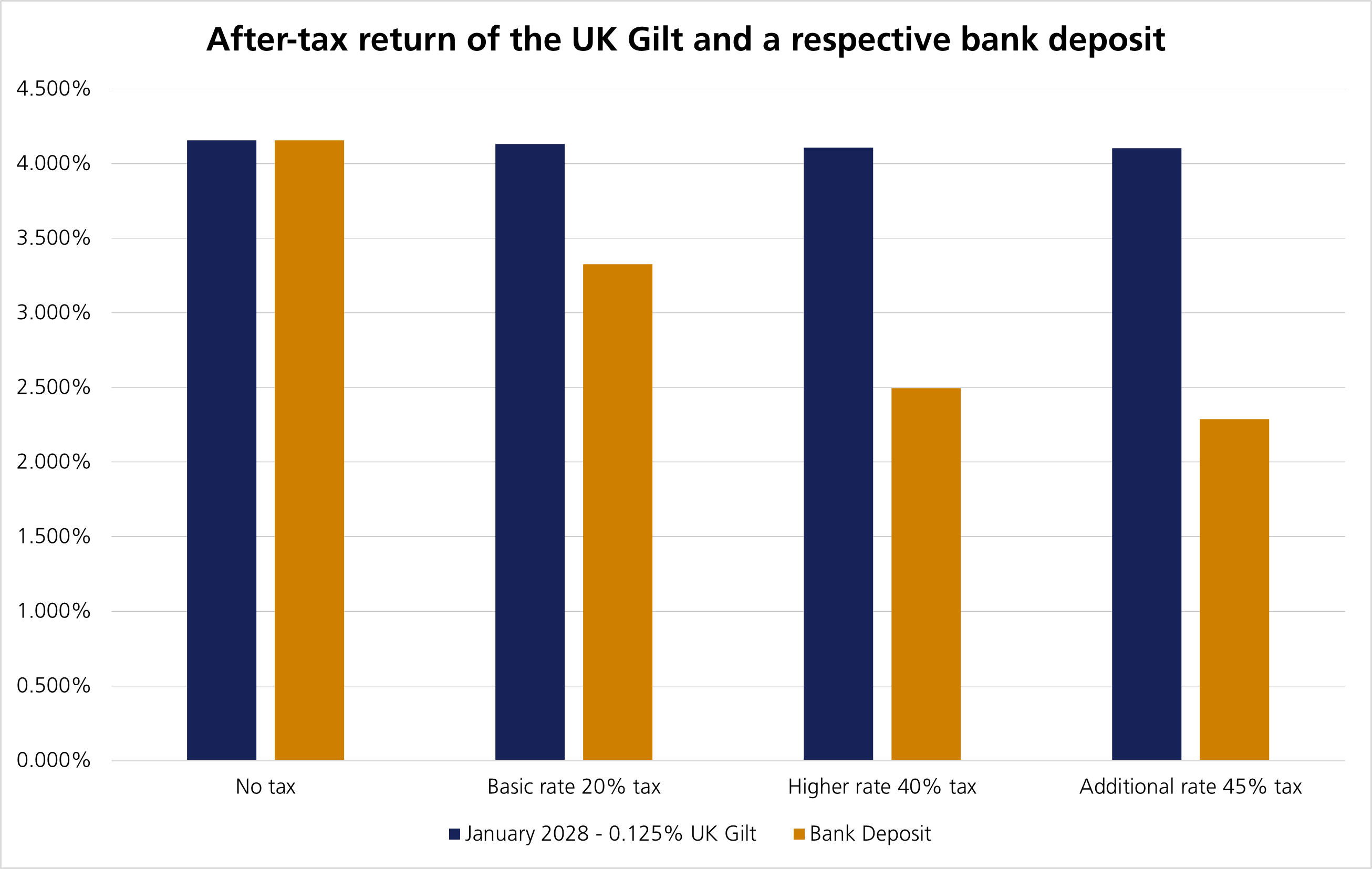

Take Treasury 0.125% January 2028, trading around £93.31 per £100 face value. If held to maturity, the annual return would be approximately 4.16% (YTM), with most of that return in the form of a tax-free capital gain. Here’s a comparison of the after-tax return from this low-coupon gilt, and a bank deposit, taxed at each income tax band:

For a 40% taxpayer, the after-tax return on this gilt would be approximately 4.11%, compared with around 2.50% from a bank deposit offering the same headline rate.

In other words, and using GEY calculations, a higher-rate taxpayer would need a savings account paying roughly 6.85% gross to achieve a similar net return.

The relevance of this investment opportunity has grown with the extended freeze on income tax thresholds. The Office for Budget Responsibility (OBR) estimates that more than 3 million more people will be drawn into the higher and additional rate bands by 2028-29 through fiscal drag alone (OBR, Economic and Fiscal Outlook).2 For many investors, particularly those with substantial cash held outside tax wrappers, the difference between headline returns and after-tax returns is becoming increasingly important.

As with all bonds, gilt prices can be impacted by a variety of factors such as changes in interest rate expectations, inflation data and market sentiment. Although gilts can be sold before maturity, it is important to be aware that prices achieved may be below the original purchase price, which means investors may receive back less than invested if they sell early. For this reason, this approach is best for investors who are comfortable holding the gilt until the fixed date of maturity, for example for those where funds are earmarked for a known time horizon. Taxation rules around gilts may also change, so individual circumstances and appropriate tax advice remain important.

Direct gilts are not a solution for every investor, but for higher and additional-rate taxpayers in the right circumstances they can form part of a more tax-efficient approach to holding capital over a defined period.

[2] The capital gains tax exemption described here applies to direct holdings of individual gilts, rather than collective investment vehicles holding gilts. Investments made through gilt funds – such as ETFs, OEICs or unit trusts – are generally taxed differently.

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.