Last year, I wrote about some of the key trends impacting the luxury goods market. Many luxury goods companies, whose stock market listings we follow, experienced strong sales growth throughout the pandemic as consumers spent large amounts of disposable income on luxury goods – given the associated restrictions on travel, dining and entertainment spending. This surge in demand began to fall away as societies reopened and consumers were able to travel, dine out and socialise again.

In this article, I take a closer look at the increasingly important, other side to luxury – luxury experiences. Now growing at a faster rate than luxury goods, luxury experiences are tapping into the preferences of ultra-high-net-worth (UHNW) individuals seeking unique and curated experiences. Luxury experiences can range from fine dining, wellness-retreats, VIP sporting or cultural events, and high-end travel - including five-star hotels and the chartering of private jets and superyachts. McKinsey estimates that spending on luxury hospitality will exceed $390bn in 2028, which equates to growth of +33% (or +6% per annum) from the $293bn spent in 2023. From Bain’s 2024 luxury report, they estimated that the only luxury segments set to grow were all linked to experiences.

The cornerstones to luxury’s success remains exclusivity, quality and status signalling. Luxury goods have long conveyed status, whether through logos on clothing or leather goods acting as ‘social signals’ for the wearer, or ‘quiet luxury’ brands that prioritise ultra discreet branding (where only the initiated would recognise the brand). The unquantifiable membership to this ‘in the know’ sector of society is increasingly becoming the more powerful signal. Experiences are harder to replicate, more difficult to access and, in many cases, more socially distinctive.

Consumers are now seeking rare, personalised experiences; consider concierge services, ultra-luxury boutique hotels or private members’ clubs that offer privacy and exclusivity. Luxurious members clubs and hotel groups blend heritage grandeur with privacy and exclusivity. Soaring demand from global UHNW members reflects the growing preference for rarefied, sometimes invitation-only environments offering access to high levels of discretion and highly personalised experiences that go far beyond traditional hospitality.

Luxury experiences have always existed, but one of the reasons they are gaining more traction is that they are far more visible than they were 15 years ago. Social media has made it easier to share unique experiences, particularly amongst the younger generations. In this sense, luxury spending is no longer only about ownership but the ability to display access. That is particularly relevant for UHNW individuals, whose social media presence often reinforces the exclusivity of the experiences they can access.

Millennials in particular are prioritising ‘memory making’ over material possessions.

This presents opportunities for those in luxury experience sectors, and challenges for more traditional goods brands. This explains why high-end brands are moving further into luxury hospitality, yachts and beach clubs, with names such as LVMH, Bulgari and Armani seeking to monetise the wider customer experience. In parallel, private members’ clubs and curated, invitation-only spaces are seeing strong demand, reinforcing the importance of scarcity, service and access in luxury spending.

The luxury industry has grown ahead of global GDP over the past decade1 and within this growth, the highest spenders (categorised as spending >€70,000/year) have contributed between 40-50%.2 This trend is set to continue and, as estimated from McKinsey’s report, the >€70,000 cohort will be the major contributors to growth (65-80% to 2027). This is incrementally positive for luxury experiences given the exclusive and scarce nature of this segment within the broader luxury sector.

Another facet to the growth of luxury experiences has been a shift in consumer mindset towards assessing both value and quality – the ‘luxury equation’. After several years of price increases and higher inflation, consumers are more selective about whether a purchase feels justified. If you have had to endure price rises, but there is no tangible or commensurate increase in quality, there is a risk that the purchase and/or ownership of the luxury good could be somewhat anticlimactic.

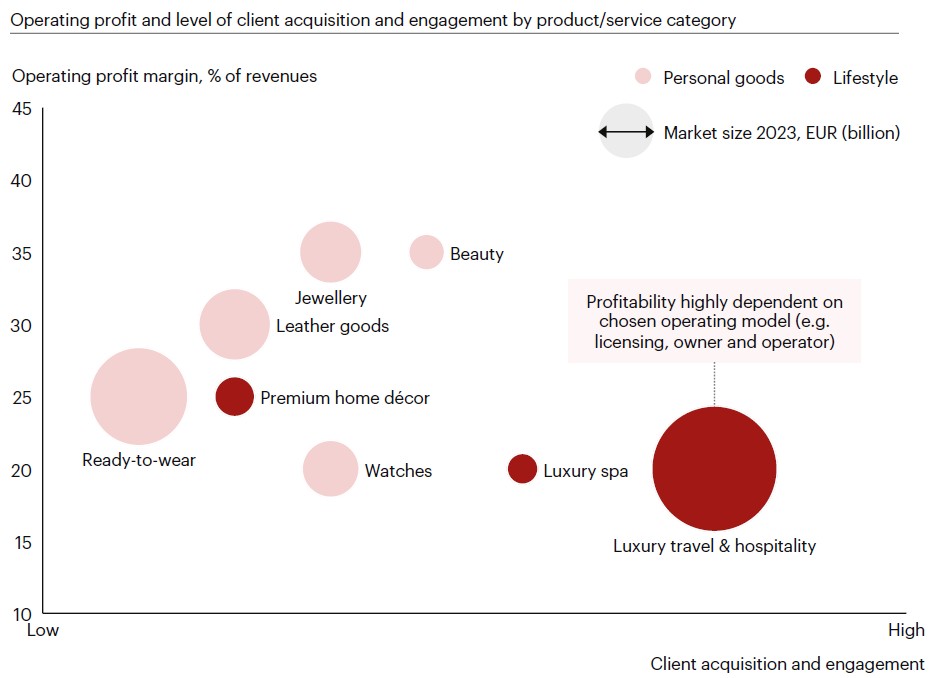

McKinsey reports that ~80% of HNWIs have said they expect to “shift a greater proportion of their luxury spending to experiences and wellness”. Experiences have the ability to offer a potentially longer lasting emotional value and/or benefit for consumers. For many UHNW and HNW individuals, who might already own many luxury goods, there could be a diminishing marginal return or utility derived from each subsequent luxury purchase. However, as experiences are typically unique, they offer more exclusivity which in turn can add to the utility or value to the consumer. The chart below shows that lifestyle categories, as highlighted in red, typically score well on the acquisition and engagement scale compared to tangible goods.

The question which consumers appear to be asking more and more is “will this purchase improve my life?”. Though difficult to quantify, it underscores the growing connection between luxury and wellness. Beyond occasional high‑end travel, consumers are now investing in holistic wellbeing through longevity clinics, retreats and premium beauty treatments. Spending on self‑care not only supports physical and emotional health but also strengthens the sense of justification behind such expenditures.

The evolving drivers of the luxury market are unlikely to fade. Greater visibility, increasingly unique and exclusive experiences, coupled with consumers’ growing focus on health and wellness, should continue to propel experiential spending. This is not to suggest that traditional luxury goods face structural decline – rather, the dynamics of luxury are shifting as the consumer evolves.

[1] Page 11 McKinsey & Company and Business of Fashion, 'State of Fashion Luxury' - 2025

[2] Page 11 McKinsey & Company and Business of Fashion, 'State of Fashion Luxury' - 2025

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.