Two powerful themes have driven markets in 2026. The first is the geopolitical uncertainty triggered by President Donald Trump’s sharp shift in US foreign policy. The second is the AI-driven sell-off, with markets shifting from favouring AI leaders to focusing on companies whose business models are most threatened by the rapidly developing technology. These trends have reversed the market’s strong start to the year, as investor attention turns to supply chain vulnerabilities and the potential growing risk of stagflation, when high inflation, weak growth and rising unemployment occur simultaneously.

Few anticipated gunboat diplomacy – the pursuit of foreign policy objectives using military force – would become a defining feature in 2026, particularly as Trump had built his campaign on opposing foreign military action. Positioning himself as a “candidate of peace”, Trump insisted he would use his deal-making skills to end multiple conflicts, notably Russia’s invasion of Ukraine.1

The opening quarter has instead been marked by direct US military action. The US launched an operation in Venezuela to remove President Nicolás Maduro, threatened to take over Greenland, and conducted joint strikes with Israel targeting Iranian military and nuclear facilities intended to destabilise its regime. While the action in Venezuela was contained, the escalation in the Middle East has had far broader consequences.

Iran responded by targeting energy infrastructure across the Gulf and restricting passage through the Strait of Hormuz, the 21-mile passageway where about 20% of the world’s oil supply passes daily.2 The result has been a significant repricing in energy markets, sending oil and natural gas prices higher and materially affecting global inflation expectations.

Equities initially held up against earlier geopolitical developments, but most gains were erased in March, as the Iran conflict and its economic impact weighed on markets. European and Japanese equities were up 7% and 16% to the end of February, before ending the quarter down -0.8% and up 4%, respectively.

The US was more mixed. The headline-level S&P 500 was little changed to the end of February, while the equal-weighted S&P 500 index – which gives each constituent the same weighting regardless of market capitalisation – was up 7%. However, as the quarter progressed, the S&P 500 ended down -4.4% while the equal weighted S&P 500 finished just slightly positive. Asian equities were hit hard by the conflict in the Middle East as the continent receives a significant amount of oil from the Strait of Hormuz. Over the quarter, Hong Kong’s Hang Seng Index lost 3% while China’s Shanghai Composite fell 1.8%. Bond yields moved higher as investors shifted from pricing rate cuts to hikes amid heightened inflation uncertainty.

The conflict in Iran sent oil prices surging in the quarter. Brent crude rose 94%, its biggest quarterly jump since the start of the Gulf War in 1990, to close the quarter at $118.35 per barrel.3 Natural gas rose 71% in Q1 as liquefied natural gas (LNG) disruptions emerged, and secondary effects on commodities such as sulphuric acid and fertiliser flows have added complexity beyond the energy sector. Read more on fertiliser disruption impacting food security.

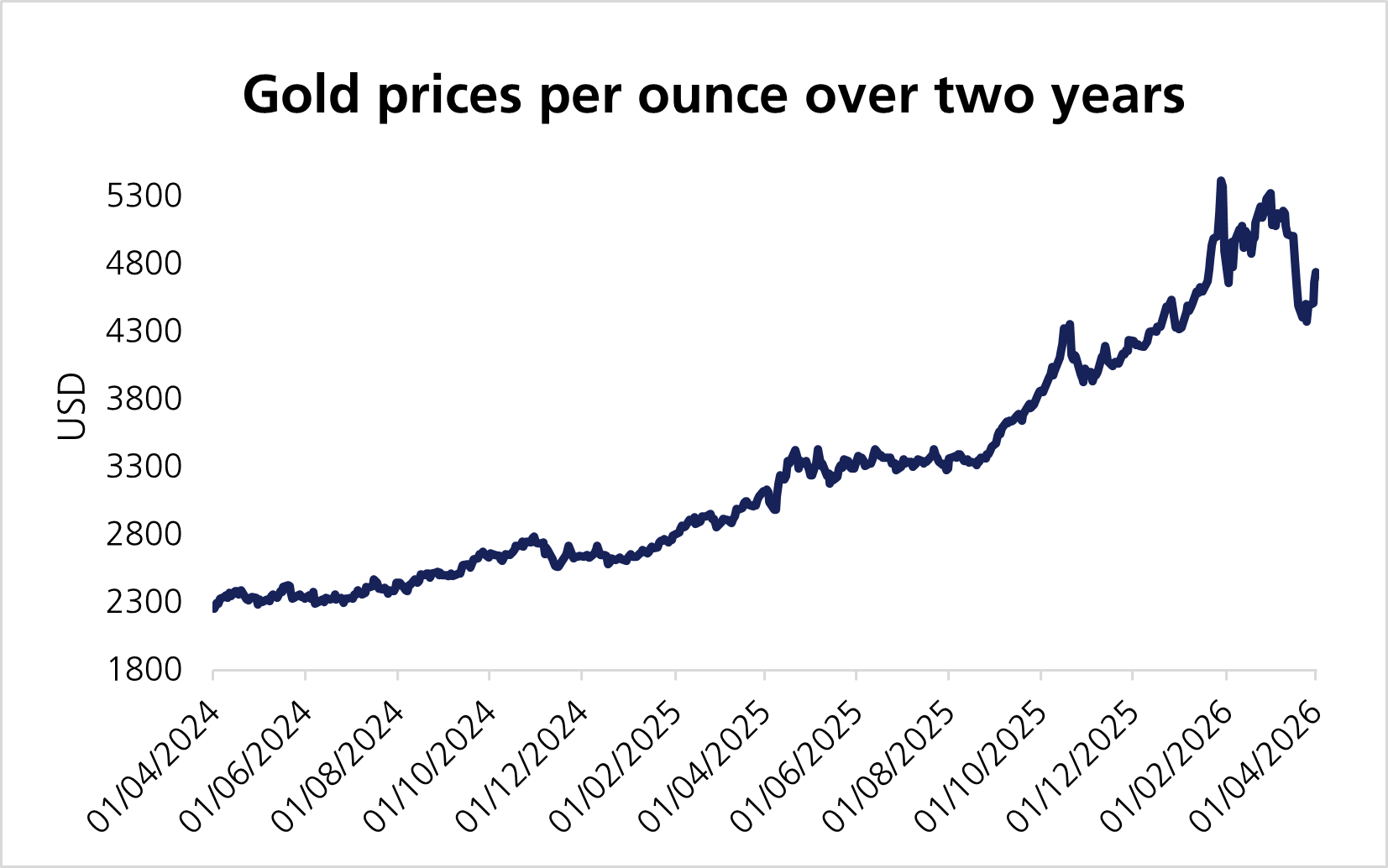

Even traditional safe-haven assets such as gold have not been immune. After a strong 2025 and a record start to the year, gold fell 11.6% in March after the conflict escalated. While gold typically performs well during periods of uncertainty as investors seek assets that preserve value, in extreme risk-off environments investors often sell their best-performing and most liquid holdings to raise cash – and gold, following its recent rally to record-high holdings, fits that profile. Its effectiveness as a safe haven is also highly dependent on the broader macro backdrop, particularly inflation, interest rates and currency movements. As such, the recent pullback is neither unexpected nor, in our view, a cause for concern, as asset prices tend to mean revert over the medium- to long-term.

The conflict is expected to feed directly into inflation – higher crude prices will raise transportation costs, airline fares and freight rates, while also affecting consumer sentiment. In addition, restricted shipping lanes are raising availability concerns for essential commodities. However, if a resolution is reached in the Middle East, the inflationary impulse would likely prove temporary, giving central banks scope to look through the near-term pressure rather than respond with further rate hikes.

It was a solid earnings season, although shares of software companies suffered significant falls after the release of industry-specific plug-ins for Anthropic’s new Claude Cowork tool. This tool – which uses language instructions to complete complex, multi-step work including file organisation and document creation – appears to compete with traditional software-as-a-service (SaaS) models. This has led investors to reassess SaaS company valuations. As a result, the S&P 500 Software Industry Index fell 24% in the first quarter, with most declines occurring before the war.

At the start of 2026, most expected central banks to continue cutting interest rates. This outlook has been upended by the ongoing Middle East conflict.

The Federal Reserve (Fed), Bank of England (BoE) and European Central Bank (ECB) all met mid-March and as expected, each left policy rates unchanged, citing the uncertain outlook shaped by rising oil and natural gas prices, which will likely fuel inflation and weigh on growth. Businesses and consumers will need to adapt to higher costs and supply chain disruption, which could intensify if the conflict continues. Policymakers must now decide whether to pause the cycle or even raise rates as inflation pressures mount.

On 30 January, Trump nominated Kevin Warsh to replace Fed Chairman Jerome Powell, subject to confirmation and pending the ongoing investigation into Powell. The Fed is no longer expected to cut rates but will likely hold.

Expectations for the BoE have shifted from two cuts this year to pricing in possible rate hikes to control inflation. The BoE’s latest forecast shows inflation hitting 3.5% in July.4 The ECB is closely monitoring medium-term risks to its inflation outlook and stands ready to adjust policy if necessary. Most economists now expect the ECB to raise rates a few times this year, although before tightening policy, global central banks will need to weigh the trade-off between containing inflation and supporting growth.

On 8 February, Japanese voters handed Prime Minister Sanae Takaichi and the long-ruling Liberal Democratic Party a supermajority in the lower house of Parliament – the first party in the post-war era to achieve such dominance. This gives Takaichi greater political room to pursue her agenda, which includes a tougher stance on immigration, a review of rules around foreign ownership of Japanese land, and policies to increase spending while cutting taxes to stimulate the economy.

Japanese equities posted strong gains post-election, although some of these gains had tapered off by quarter-end. Japan’s Topix (Tokyo Stock Price Index) rose 16% through February but ended the quarter up only 4%. Before the election, Japanese government bonds sold off amid election pledges for more consumption tax cuts, with 30-year yields rising to 3.86%, the highest since their introduction. Yields fell back from these highs, only to rise again with the Iran conflict.5

On 20 February, the US Supreme Court ruled that sweeping tariffs imposed by Trump on key trading partners violated federal law, dealing a major blow to the administration’s trade strategy and creating uncertainty over existing agreements. In response, the administration introduced a replacement tariff framework, starting at 10% and potentially rising to 15%, using a little-tested provision that allows the president to impose broad tariffs for up to 150 days without congressional approval.

Looking ahead to the remainder of 2026, markets are likely to remain highly sensitive to both geopolitical developments and technological disruption. The ongoing conflict in the Middle East will continue to influence energy markets, global supply chains and inflation expectations.

In our experience, while these periods are unsettling and unpredictable, history shows that knee-jerk reactions tend to cost investors over the long run. We continue to monitor markets and stand ready to reposition portfolios should opportunities arise. Volatility often creates attractive entry points and maintaining a disciplined, long-term approach can allow investors to capture gains as markets recover.

[1] How to Avoid a Forever War in Iran | WPR

[2] Iran war: What is the Strait of Hormuz and why does it matter? - BBC News

[3] Deutsche Bank, Bloomberg

[5] Deutsche Bank, Bloomberg

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.