In his book Pioneering Portfolio Management, the former CIO of the Yale endowment, David Swensen, helped popularise the idea that long-term portfolios should extend beyond traditional stocks and bonds to include assets linked to the real economy and alternative assets such as hedge funds.

First published in 2000, the book drew on lessons from investing across a range of market environments, including periods of elevated inflation. One of its enduring messages is that portfolios can be made more resilient by broadening their sources of return. Swensen argued that one way to do this is via real assets, which can help diversify traditional bond-equity exposures and offer some protection for purchasing power when inflation is higher.1

Real assets are investments linked to the physical economy. They typically include real estate, infrastructure, natural resources and commodities, and, in some cases, listed securities closely tied to those themes. What makes them distinctive is their connection to tangible assets, essential services and long-term demand trends. Since many real assets are linked to physical goods, replacement costs or revenues that can adjust with prices, they are often seen as better placed to keep pace with inflation – hence the term “real” assets.

The reason these assets are back in focus is that the market backdrop has changed. For much of the past two decades, investors operated in a world of subdued inflation, expanding globalisation and reliable correlations between equities and bonds. This enabled investors to create diversified portfolios by mixing both, popularising the 60/40 split strategy. However, that approach has faced challenges recently. Inflation pressures have proved stickier than many expected, while geopolitical fragmentation is reshaping trade, energy flows and supply chains.

Recent years have also been a reminder that supply can no longer be taken for granted. Since 2020, the global economy has absorbed a series of major disruptions – from the pandemic and its aftermath to energy shocks and renewed regional conflict, including the wars in Ukraine and Iran. The latest tensions involving Iran and the wider Middle East are another example of how quickly stress in strategic regions can ripple through commodity markets, transport routes and inflation expectations.

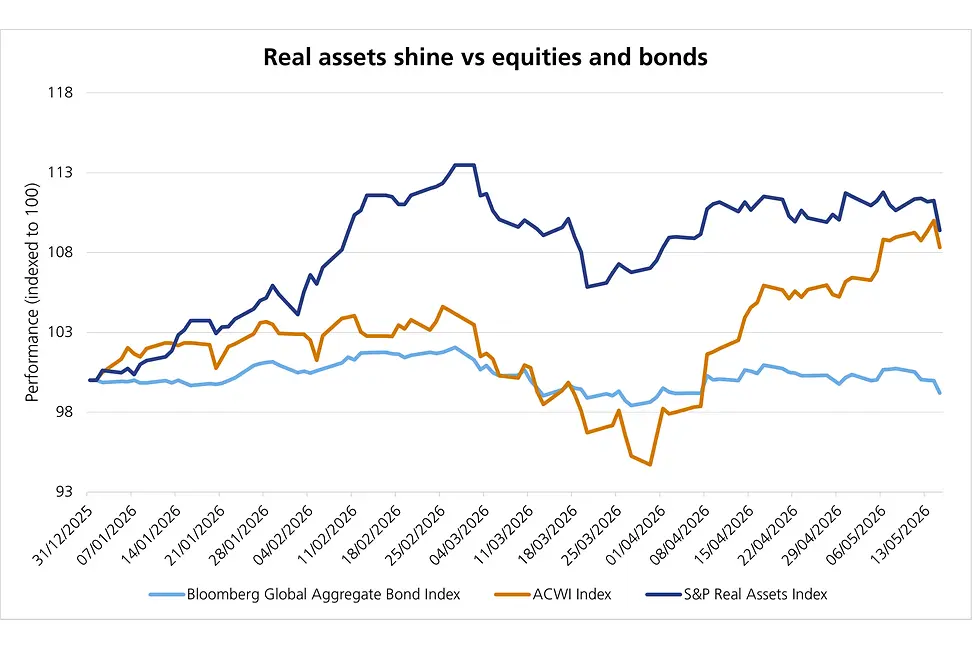

At the same time, the relationship between bonds and equities has become less consistently supportive. When inflation is low and stable, bonds can often help offset weakness in equities. But when inflation risk re-emerges, that relationship can become less dependable. In addition, rising pressure on government deficits may make sovereign bonds less reliable as portfolio shock absorbers. In that environment, assets linked more directly to physical infrastructure, pricing power, contracted revenues, or scarce resources can attract renewed attention.

Another important driver is electrification. The shift towards more electric, digital and energy-intensive economies requires enormous investment in grids, storage, transmission, renewables, transport networks and raw materials. This is not a short-term story, but rather a structural theme likely to unfold over many years and one that touches multiple parts of the real asset universe.

The tectonic plates are shifting at both a geopolitical level, from tariffs and NATO to currency realignment, and at a technological level, namely through the rise of AI. The pace of change is unusually high. Yet when trying to make sense of major transitions, it often helps to look backward as well as forward. In that respect, Swensen’s views on alternatives and real assets look as relevant today as they did in 2000. Real assets can help protect portfolios against the uncertainty surrounding inflation, infrastructure, energy security, supply constraints, and geopolitical change. They provide exposure to parts of the economy that are likely to remain crucial over the next decade.

This does not mean they are immune from volatility. But it does help explain why they have returned to the conversation at a time when old assumptions around growth, inflation and diversification are being tested.

[1] Pioneering Portfolio Management - An Unconventional Approach to Institutional Investment, 2000, David F. Swensen

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.