Gilts are a long-established component of financial markets, yet beyond industry circles they are sometimes misunderstood or dismissed as technical jargon. In this guide, we outline what gilts are, how they work and how, in the right circumstances, they may offer investors tax efficiencies when compared with cash.

A gilt is a bond issued by the UK Government to finance its spending plans. When an investor buys a gilt, they are effectively lending money to the government. In return, the government pays investors a fixed rate of interest each year – known as the coupon – and pledges to repay £100 per bond at a set future date, also known as the maturity date. Most gilts are issued with a face value, or par, of £100.

The overall return over the life of a bond is called the yield to maturity (YTM), which combines both sources of return.

Gilt portfolios can be structured in several ways. An investor may buy a single bond, or they may hold a range of bonds that mature at different times so that cash is returned gradually over several years. This approach can help investors plan for known future expenses, such as tax payments or school fees, and manage surplus cash more efficiently.

For individual investors, gains on UK gilts are exempt from capital gains tax (CGT). However, the interest payments they receive are taxed as income at the investor’s usual tax rate. That is an important distinction. A low-coupon gilt – in other words, a gilt with a low fixed rate of interest – bought below its £100 maturity value, may produce only a small amount of taxable income, while a larger portion of the return may come from the capital gain. This means a low-coupon bond bought below its face value and held to maturity can deliver most of its return free of tax.

For certain UK investors, especially those paying higher or additional tax rates, this can make gilts more tax-efficient than cash deposits offering a similar headline return.1 With yields at their highest levels in over 15 years, they may offer an attractive opportunity in the right circumstances.

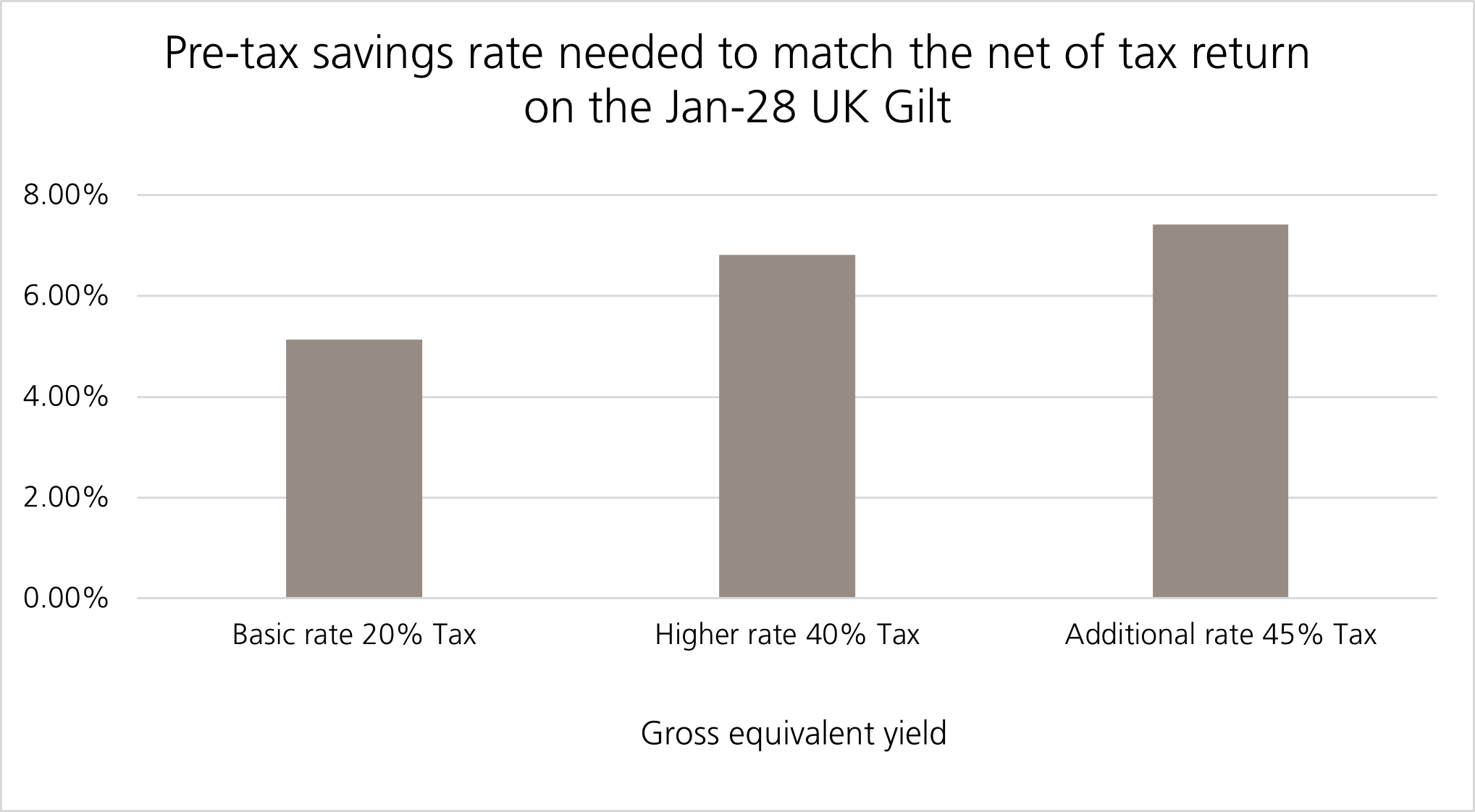

A useful way to compare a gilt with a cash savings account is to use the gross equivalent yield (GEY). This shows the interest rate that a taxable savings account would need to offer to give you the same return as a gilt after tax. For higher-rate taxpayers, this gap can be meaningful – the higher the marginal tax rate, and the lower the gilt's annual interest payment, the larger the gap between a gilt's return and the equivalent return needed from cash savings.

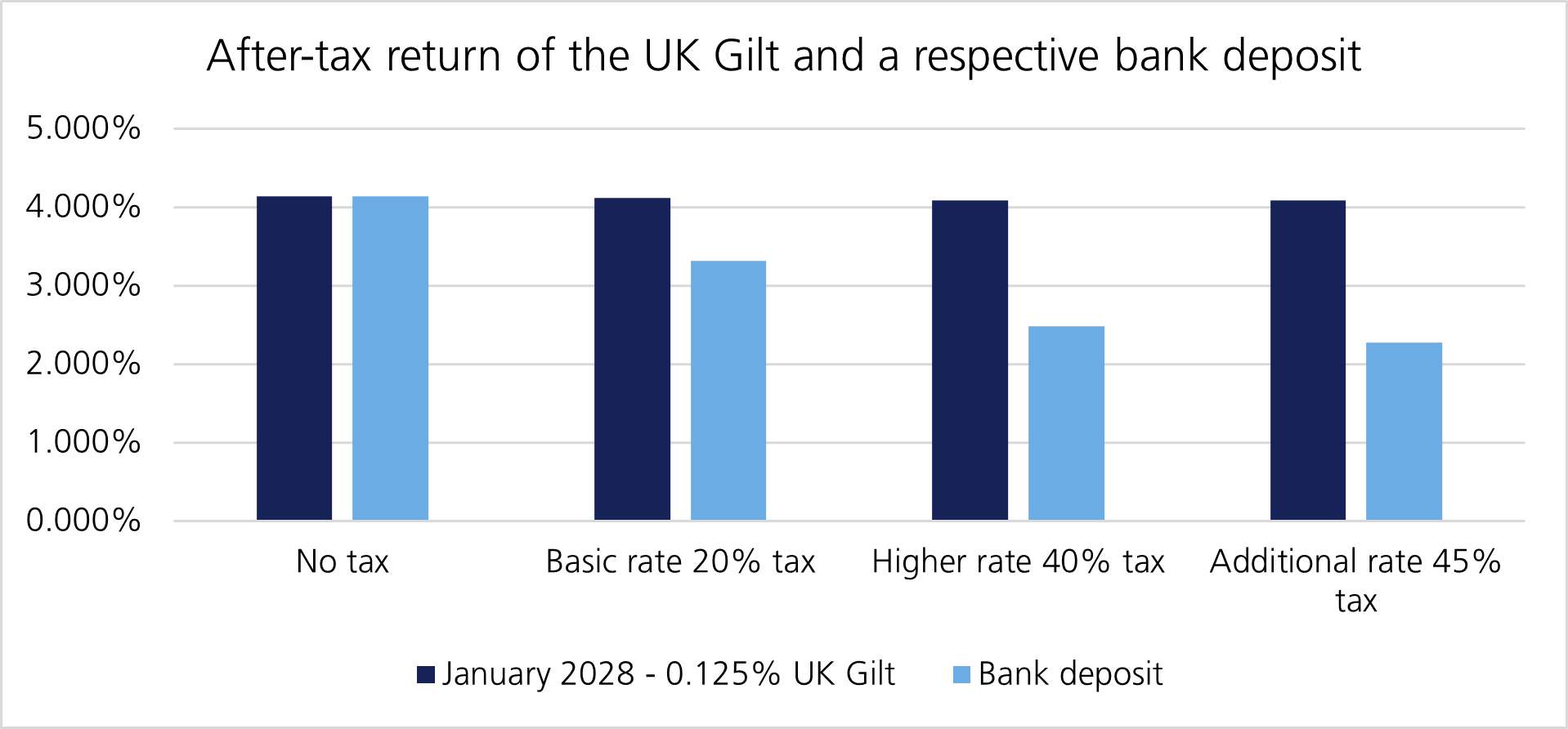

For example, as at the time of writing, the UK Treasury 0.125% January 2028 bond is priced at around £93.48 for every £100 it will repay at maturity. If held to maturity, it would deliver an annual return of approximately 4.14%. Because the interest rate on the bond is very low, most of this return comes from the increase in value as the bond moves towards its £100 repayment amount. Here’s a comparison of the after-tax return from this low-coupon gilt, and a bank deposit, taxed at each income tax band:

For a 40% taxpayer, the after-tax return on this gilt would be approximately 4.09%, compared with around 2.48% from a bank deposit offering the same headline rate.

In other words, and in using GEY calculations, a higher-rate taxpayer would need a savings account paying roughly 6.82% gross to achieve a similar net return. It is worth caveating that the returns from a gilt are less evenly distributed over time than the interest from a savings account, because much of the gain is realised at maturity.

This investment opportunity has become more relevant as income tax thresholds have been frozen for an extended period. The Office for Budget Responsibility (OBR) estimates that, as a result of “fiscal drag” – where people are pushed into higher tax bands as incomes rise – more than 3 million more people will be drawn into the higher or additional rate bands by 2028-29.2 For many investors, particularly those holding substantial cash outside tax wrappers, the difference between headline returns and the amount received after tax is becoming increasingly important.

As with all bonds, gilt prices can go up or down depending on factors such as changes in interest rate expectations, inflation data and overall market conditions. Although gilts can be sold before their maturity date, there is a risk they may be sold for less than they were originally bought for, meaning an investor could get less back than they invested if they sell early. For this reason, gilts used for this purpose are generally more suitable for investors who are comfortable holding them until their fixed maturity date – such as when the money is set aside for a known future need. Tax rules can also change over time, so investors should consider their individual circumstances and seek appropriate tax advice where needed.

Direct gilts are not suitable for all investors, but for certain higher and additional-rate taxpayers, in the right circumstances, they can offer a tax-efficient route of holding money over a set period. These themes underscore the need for proactive financial planning. Investors must consider the timing and structuring of gilts, balancing tax efficiency with financial security.

[1] The capital gains tax exemption described here applies to direct holdings of individual gilts, rather than collective investment vehicles holding gilts. Investments made through gilt funds – such as ETFs, OEICs or unit trusts – are generally taxed differently.

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.