How are developed, emerging and frontier markets defined, what distinguishes them, and why do these differences matter?

Most people have probably heard countries described as “developed”, “emerging” or “frontier” markets. The labels appear everywhere, whether in discussions about economic growth, global investing or stock market performance. But what do they actually mean?

At first glance, the categories can sound like a ranking of countries’ wealth levels. In reality, the distinction is more nuanced. These classifications look at a mix of factors, including the size of a country’s economy, how mature and reliable its financial markets are, how easy it is to invest there and how stable its political and legal systems appear to be.

In this guide, we outline what separates developed, emerging and frontier markets, how countries are placed in each category and why these distinctions matter to investors and the wider economy.

Developed markets are generally considered the world’s most mature and established economies. They tend to have large, sophisticated financial systems, strong institutions and relatively predictable business environments, making them attractive to investors seeking stability and long-term reliability.

The United States, United Kingdom, Germany and Japan are examples of developed markets due to their relatively stable political systems and higher standards of living. Stable governments and stronger institutions mean geopolitical risks tend to be lower, while higher income levels provide citizens with better access to quality healthcare, education and necessities.

These markets also benefit from advanced infrastructure and industrialisation, which support innovation and the development of cutting-edge technologies. This is particularly evident in the MSCI World Index, which consists of large and mid-cap companies across 23 developed markets. Information technology (IT) is the largest sector in the index, with companies such as Nvidia, Apple, Microsoft and Alphabet making up roughly 20%-25% of its weight. The index is heavily tilted towards the US, which represents 70% of the MSCI World Index. In the MSCI World ex US index, the weight of IT falls from about 26% to approximately 8% and outside the US, sector weights are evenly distributed across financials, industrials and healthcare.

Developed markets are home to large, mature businesses with well-established market positions and long operating histories. The average market value of the MSCI World Index’s underlying companies is roughly $60 billion, compared to $8 billion in the MSCI Emerging Markets Index and just $700 million in the MSCI Frontier Markets Index. However, because these are mature economies, growth opportunities in developed markets are often limited, unlike emerging economies where many are still industrialising, building infrastructure and growing their middle classes. Developed markets have an average real GDP growth rate of 1.9% over ten years compared to emerging markets, which have grown by an average of 4.1% annually.1

High-growth regions such as India, Brazil and China fall under the emerging markets category. Once largely farming economies, these countries have shifted towards manufacturing, industrialisation and developing infrastructure. Emerging markets typically benefit from a younger labour force, supporting future growth and putting them at an advantage compared to developed countries, which have ageing populations. In addition, these markets tend to have a growing middle class, a cohort that is set to expand over the next decade, leading to higher spending on goods and services that were previously out of reach for many households.

Despite their rapid economic growth, these markets still have a lower income per capita than most developed markets. Their capital markets are also less mature. This means they often rely on borrowing money from foreign investors, which introduces currency risk, as debt borrowed in foreign currencies becomes more expensive to repay if the local currency weakens. The political climate may also be volatile and changes in leadership can drive unforeseen shifts in regulatory frameworks, affecting investor confidence.

Nonetheless, emerging markets are gradually improving their financial institutions and integration with global markets. The MSCI Emerging Markets Index consists of 24 emerging market countries with geographic regions diversified among China (25%), Taiwan (23%), South Korea (15%) and India (13%). The MSCI Emerging Markets Index’s top sector weight is also IT because of companies such as Taiwan Semiconductor and Samsung, underscoring the important role emerging markets have in providing critical inputs for technology infrastructure globally.

Frontier markets, such as Vietnam, Romania and Morocco, are classified as economies at an earlier stage of capital market development, often on a path towards emerging market status. They tend to be less integrated into global financial systems, reflecting developing institutional frameworks and infrastructure, and they remain heavily reliant on local banks, property and natural resources. In many frontier markets, a significant share of economic activity takes place outside formal systems. While this can make it harder to accurately track economic growth, it also reflects evolving economic structures that often formalise over time.

Income levels are generally lower than in more developed markets, which can influence access to healthcare, education and certain essential services. At the same time, frontier markets benefit from favourable demographics, including expanding populations, a growing consumer base and a young labour force.

The MSCI Frontier Markets Index includes 28 countries, with sector exposure mainly within financials, real estate and energy. Most companies are small-cap, reflecting early-stage market development.

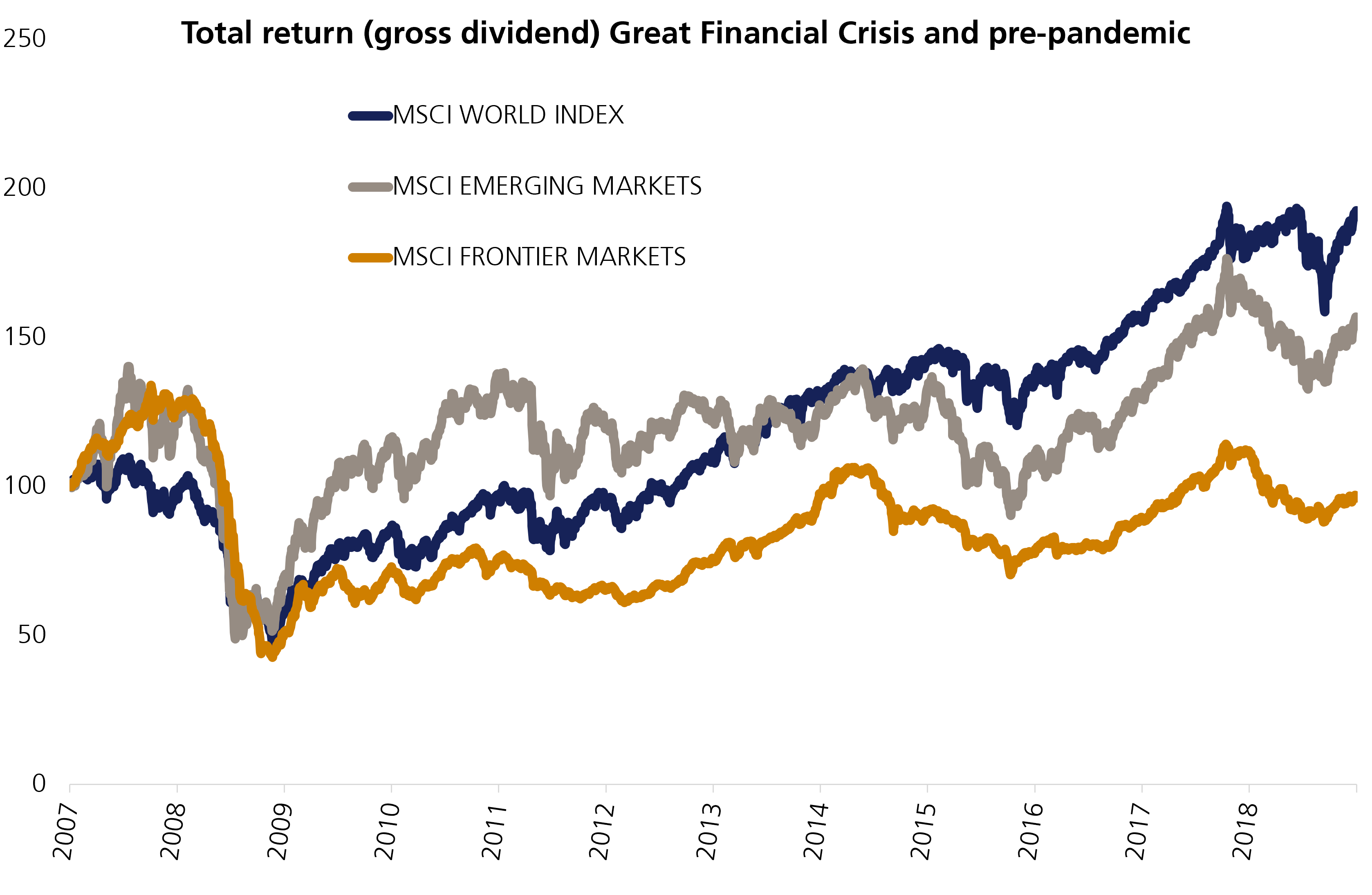

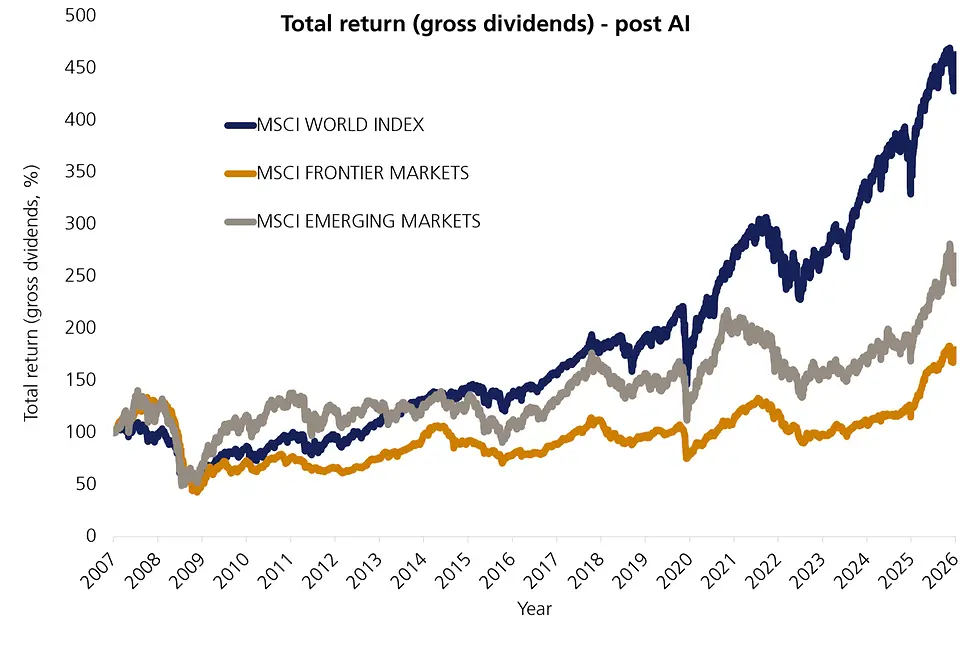

When it comes to making investment decisions, knowing which market you’re investing in is crucial, as they can behave differently over time. After the financial crisis in 2008, emerging markets became an attractive region for investors, due to strong fundamentals, rising credit quality and a China-led stimulus. However, the narrative changed after the US dollar strengthened, growth in China slowed and oil and metal prices collapsed between 2014 and 2016, leading emerging markets to underperform developed markets. More recently, an era of so-called US exceptionalism and the rapid progress in artificial intelligence have made the divergence even more pronounced.

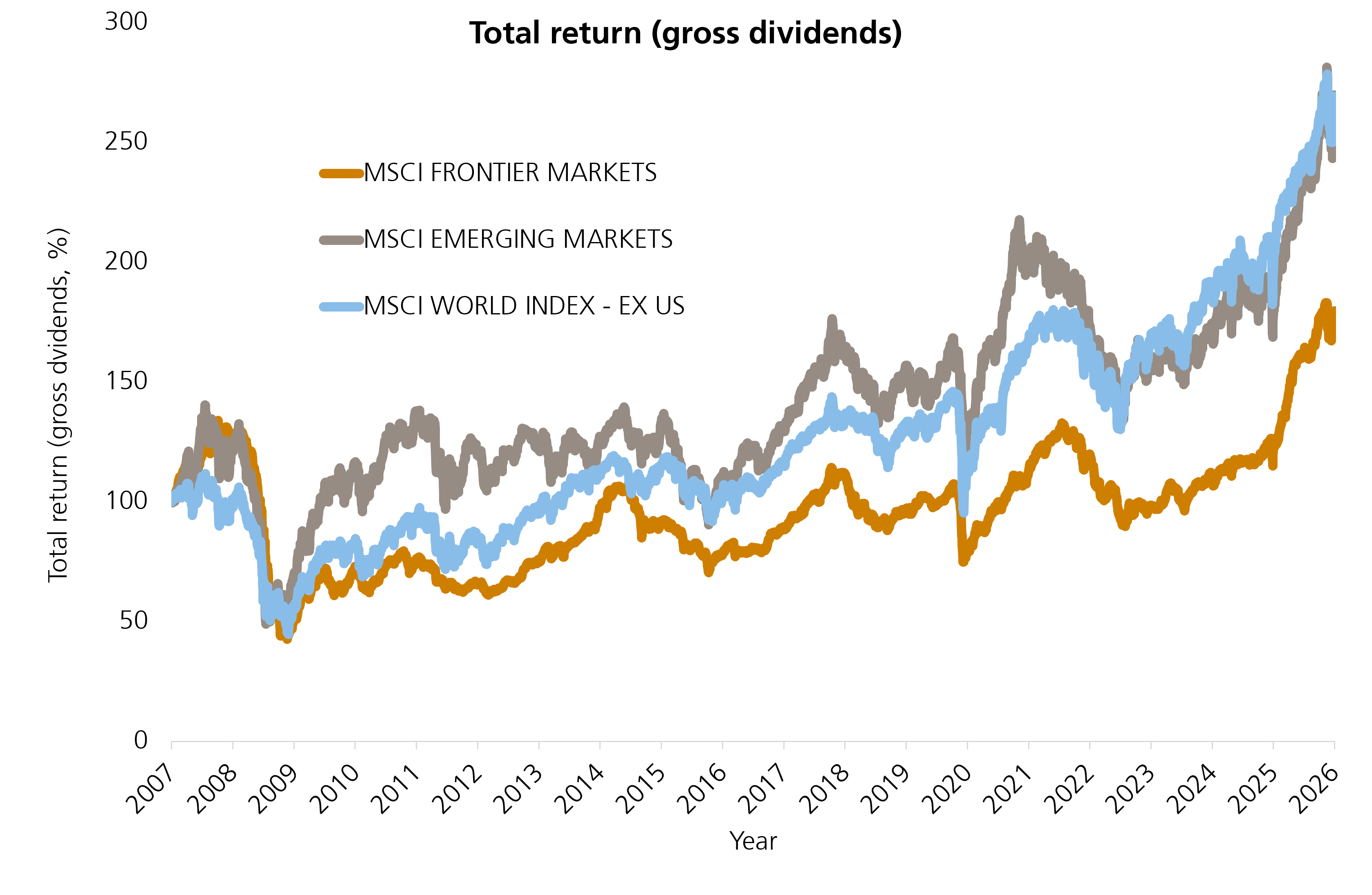

Since the US dominates much of the world index, the outperformance is mainly a US story. Stripping out the US shows that emerging and developed markets have delivered similar returns, suggesting that emerging markets are not structurally weaker, but have generally had less exposure to sectors like technology that have driven global returns in recent years.

Emerging markets and developed markets have meaningful exposures to cyclical sectors, trade flows and commodity prices, and offer attractive opportunities in manufacturing, services and natural resources.

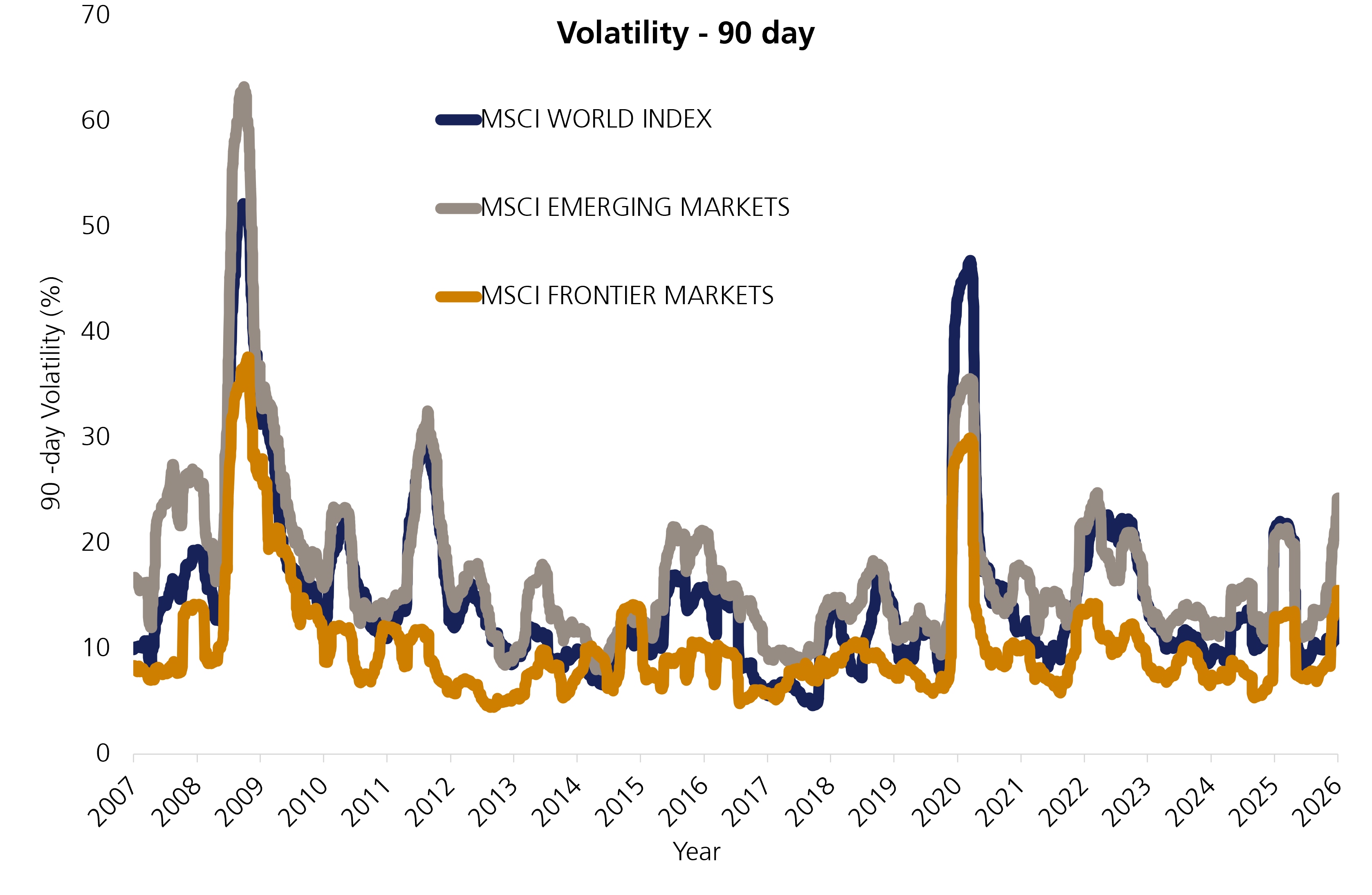

Total returns are only one part of the story. Volatility levels – a measure of how sharply and frequently investment prices rise and fall over time – are also a key factor in investor decision making. Currency fluctuations, commodity price swings and political uncertainty all drive volatility in emerging markets. Contrastingly, frontier markets often display lower volatility, but this is mostly due to illiquid markets and lower trading volumes. Price movements can be infrequent and may not fully reflect underlying risks. Ultimately, a lack of transparency in frontier markets remains a challenge for investors.

Market classification helps set expectations around different economic realities and shape how investors view risk and opportunity. Developed markets are generally seen as larger, more stable and predictable; while emerging and frontier markets may offer faster growth but with greater uncertainty. Knowing whether a market is developed, emerging or frontier provides insight into its potential growth prospects, liquidity, volatility and risk profile. The question is not which market is superior but rather what role each plays within a portfolio.

[1] International Monetary Fund

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.