The war in Iran transitioned to an uneasy ceasefire over the second quarter, culminating in a peace deal. Equity markets largely looked beyond the conflict as the de-escalation was anticipated, allowing investors to rule out a longer economic shock. After falling to a 2026 low at the end of March, US equities staged a sharp rebound, with strong earnings and AI investment continuing to lift technology stocks and propel the Nasdaq to gains of 21.6% in Q2. Of all the sectors, technology companies had the strongest earnings growth, rising by 55% compared with the same quarter last year. This drove analysts to move future earnings forecasts higher. Oil prices fell by 38.4% to finish the quarter at $72.92 a barrel.

UK local elections in May put Prime Minister Sir Keir Starmer’s position in question. By mid-June, he stepped down as leader of the Labour Party, paving the way for a new leader as early as mid-summer, the UK’s seventh prime minister in 10 years. This instability has weighed on UK government debt, keeping borrowing costs higher.

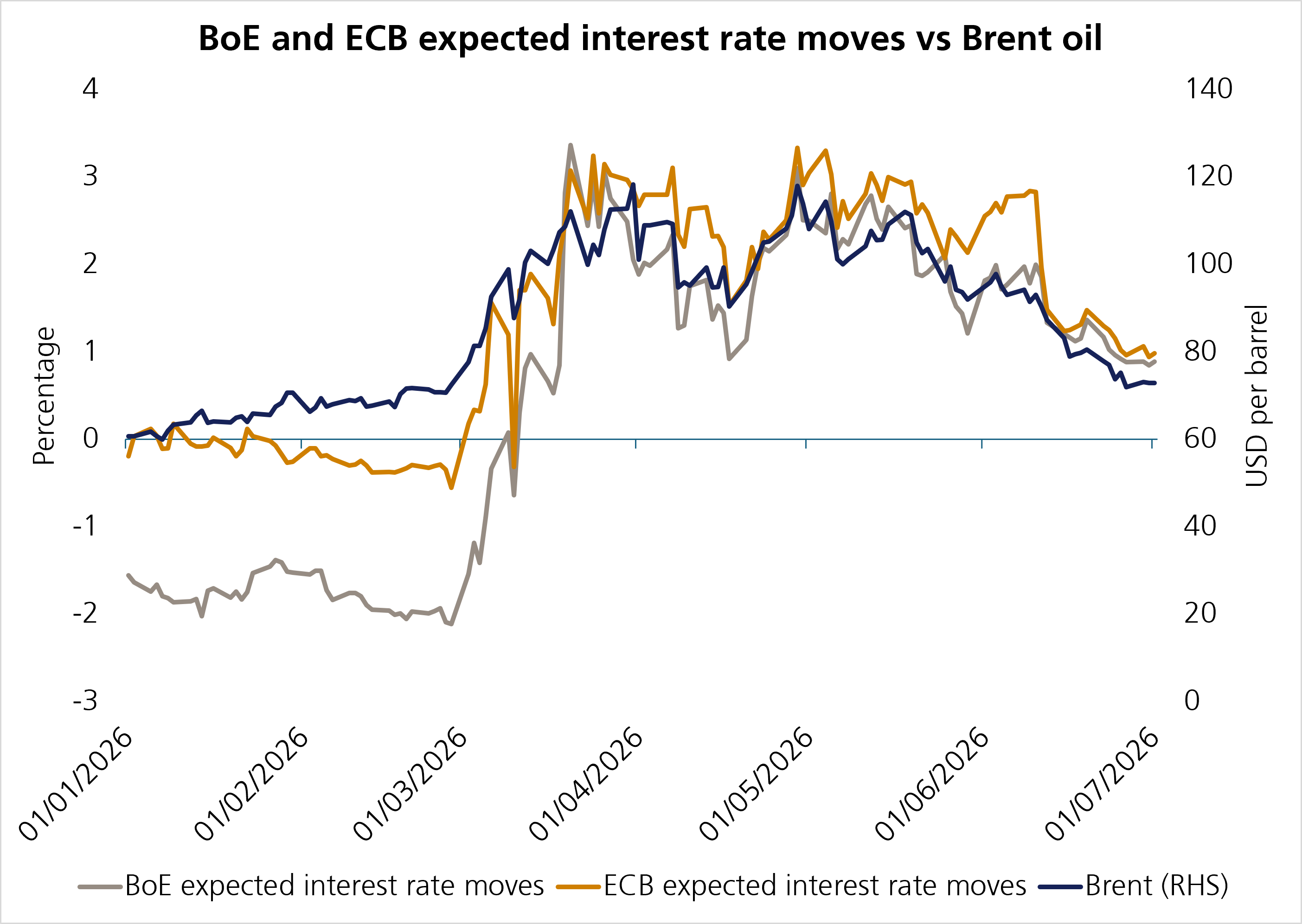

What was supposed to be a short conflict in Iran passed the 100-day mark on 7 June. However, in mid-June, the US and Iran announced the framework of a deal that included an immediate and permanent cessation of hostilities, the reopening of the Strait of Hormuz within 30 days, and a 60-day negotiation period during which both sides sought to resolve outstanding issues surrounding Iran’s nuclear programme and sanctions relief. The tentative reopening of the Strait, a global supply chain chokepoint, drove energy prices lower, as increased shipping capacity diminished the risk of supply disruptions.

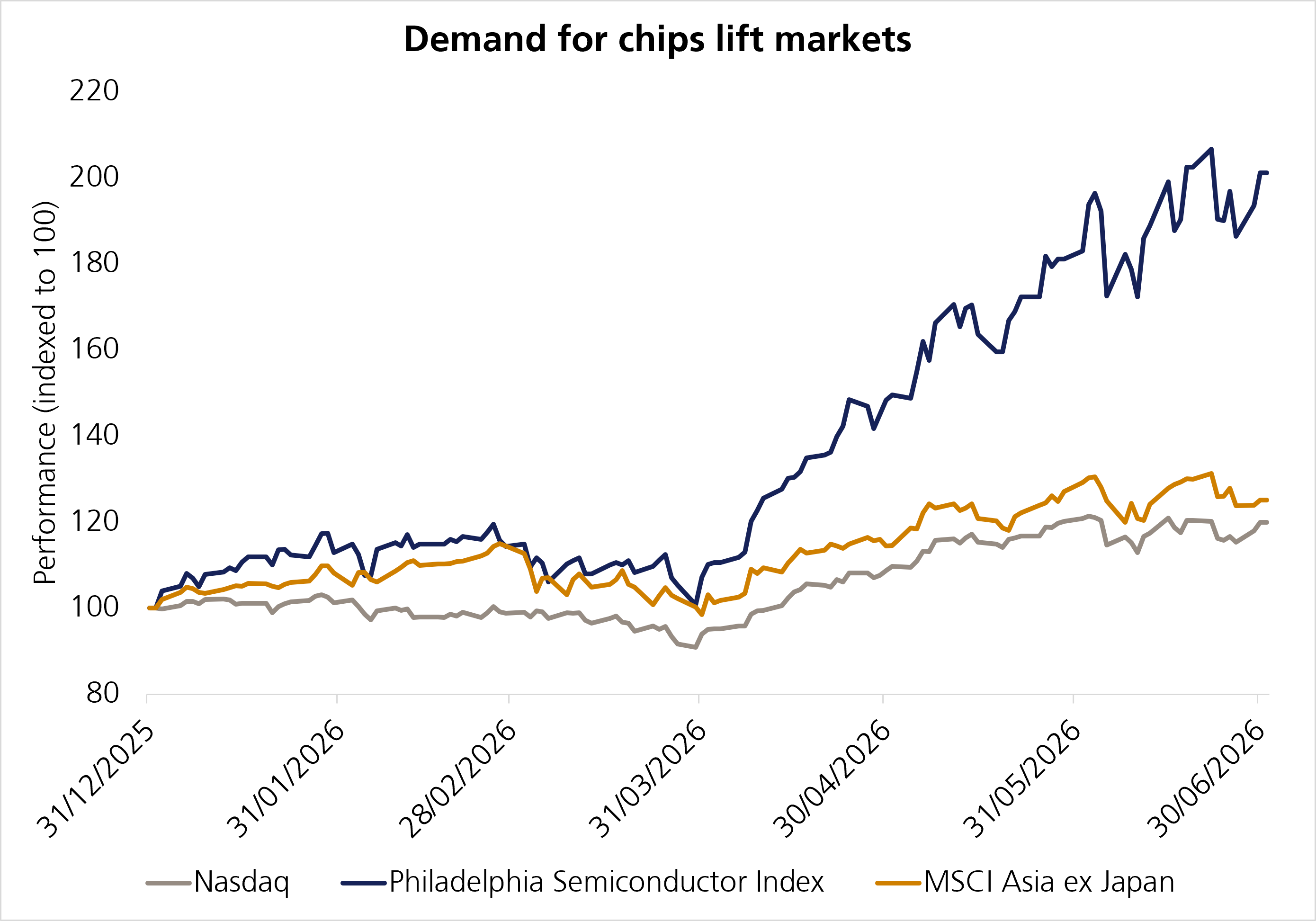

Equities marched higher throughout the quarter as strong earnings accelerated sales growth, particularly for technology-led companies. Demand for chips drove the Philadelphia Semiconductor Index up 88%, its best quarter since the index began in the early 1990s, taking its year-to-date gains to over 100%.1 The S&P 500 rose 15.2%, its best quarter since the second quarter of 2020.2 Gains broadened beyond technology companies, with the S&P 500 Equal Weight Index returning 11.4%. European equities also posted solid gains, with the STOXX 600 Index rising 11.9%, but returns were more muted in the UK, with the MSCI UK Index rising only 3.4% as the sharp decline in oil prices weighed on oil majors.

Outside the US, Asia shone, with the Topix gaining 14.3% and Korea’s Kospi rising 68% in Q2, as the country’s technology bellwethers Samsung, LG Electronics and SK Hynix benefited from the ongoing AI boom. It was a more mixed picture for Chinese equities. Hong Kong’s Hang Seng fell 6.4% while the Shanghai Composite rose 6% in Q2.

The pipeline of mega-IPOs is shaping up to be one of the defining features of the current equity market cycle. After years of remaining private while raising unprecedented amounts of capital, a handful of AI and space technology companies have reached a scale that rivals many of the world’s largest listed businesses.

SpaceX, Claude’s creator Anthropic and ChatGPT founder OpenAI have raised over $330 billion in private funding and are now turning to the public equity and bond markets. SpaceX raised approximately $75 billion from its offering. SpaceX shares closed the end of June around 25% higher than their floatation price, representing a market capitalisation over $2 trillion.

Meanwhile, Anthropic3 and OpenAI4 have each filed with the Securities and Exchange Commission5 to take their companies public in the future.6 In addition to closely monitoring these companies’ IPOs, investors will keenly watch their debt financing – SpaceX has already raised $25 billion in bonds after its IPO.7

At the Federal Reserve’s (Fed) June meeting – Kevin Warsh’s first as chairman – the central bank opted to leave interest rates unchanged but adopted a more hawkish tone than expected. Policymakers indicated they had growing concerns that inflationary pressures could re-emerge, driven by the underlying strength of the US economy rather than by external shocks in the Middle East. A stabilising labour market, resilient consumer spending, fiscal support and strong AI-related investment have lifted domestic demand, prompting the Fed to be more cautious about easing policy. Reflecting this shift, the latest dot plot – which shows where individual Fed policymakers expect interest rates to be in coming years – showed that roughly half of policymakers expect at least one further rate increase before year-end.

Meanwhile, in a widely anticipated move, the European Central Bank (ECB) increased interest rates at its June meeting to 2.25% from 2%, signalling that bringing inflation back to its target remains a priority. The peace deal was signed after this meeting, which will reduce the need for immediate rate hikes, leading to lower expectations for further policy tightening. The Bank of England (BoE) kept rates steady in June in a 7-2 split, helped by softer-than-expected inflation data and lower energy prices. Inflation came in at 2.8%, while core inflation – which excludes energy and food – was 2.6%, both below expectations.8 This suggests that the need for tightening has diminished, allowing the BoE time to keep policy on hold while assessing the economy further.

In Japan, the Bank of Japan (BoJ) raised rates by 0.25% as expected, given that inflation remained sticky. While policymakers signalled further hikes ahead, the pace remains slow, prompting further weakening of the yen.

Sir Keir Starmer resigned as leader of the governing party on 22 June, with most expecting former Manchester Mayor Andy Burnham to become the UK’s next prime minister as he is currently uncontested in the leadership election. Questions remain on his potential policies, although gilt markets were supported after Burnham committed to maintaining Rachel Reeves’s fiscal rules in a speech on 30 June.9

Overall, the second quarter reinforced the dominant themes that have shaped markets in recent years, as investors moved past the Middle East conflict. Strong corporate earnings and accelerating AI-related investment are supporting solid economic growth. This has led the Fed to become more cautious as inflation risks shift from external shocks to domestic demand.

Markets have so far taken confidence from strong company fundamentals and broadening profit growth across sectors. As we enter the second half of the year, the key question for investors is whether earnings and productivity gains can continue at the current pace without prompting intervention from central banks.

[1] Deutsche Bank

[2] Bloomberg, Deutsche Bank

[3] Anthropic raises $65B in Series H funding at $965B post-money valuation \ Anthropic

[4] Racing to a Trillion: OpenAI and Anthropic's Funding History

[5] Confidential submission of draft S-1 to the SEC | OpenAI

[6] OpenAI plans stock market debut, setting up new race with Anthropic - BBC News

[7] SpaceX - SpaceX Announces Pricing of $25 Billion Inaugural Bond Issuance

[8] Office for National Statistics

[9] Burnham to give mayors more power in 10-year plan to transform economy - BBC News

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.