UK bond markets reacted cautiously following last week’s local election results, with investors assessing the potential implications for fiscal policy, public spending and borrowing.

While the elections do not directly change government policy, the results have increased political pressure on the Labour government and prompted renewed market focus on the UK’s medium-term fiscal outlook.

In particular, investors are closely monitoring whether the government may come under pressure to pursue more expansionary spending measures in response to weaker political support. Any perception of looser fiscal policy could place upward pressure on gilt yields, particularly at a time when inflation and borrowing costs remain elevated.

Sir Keir Starmer and Rachel Reeves are perceived to be part of the more centrist faction of the Labour Party. Former Health Secretary Wes Streeting, who resigned earlier this week to challenge Starmer, is seen as a centrist contender who could bring some stability to gilt markets. Markets are assessing whether political pressure on the government could result in support for Andy Burnham or Angela Rayner, which may increase expectations for high public spending commitments.

This would mark a change from Reeves’s position of maintaining fiscal credibility. In September, Burnham said Britain is “in hock to the bond markets”, suggesting that the government is trying to appease bond markets and international investors.1 At the time, gilts came under some pressure given his prominence within the Labour Party. Some Labour MPs agree with Burnham that the government has become too constrained by the Treasury, although Reeves and plenty of economists say that the British government simply cannot borrow much more money.2 Taken together, these divisions highlight a faction within Labour that would like to see greater fiscal expenditure and higher spending commitments.

Although the timeline of a potential leadership election remains unclear, bond markets are reacting to the prospect of higher borrowing. Given Labour’s poor outcome at the local elections – much like the Conservatives following their defeat in 2024 – the next three years will be crucial for the government to avoid losing more vote share to Reform and the Green Party. This pressure may encourage the party to pursue bolder policy measures, potentially incorporating some of the Green Party’s more interventionist ideas. All of this has resulted in investors reassessing their exposure to UK assets.

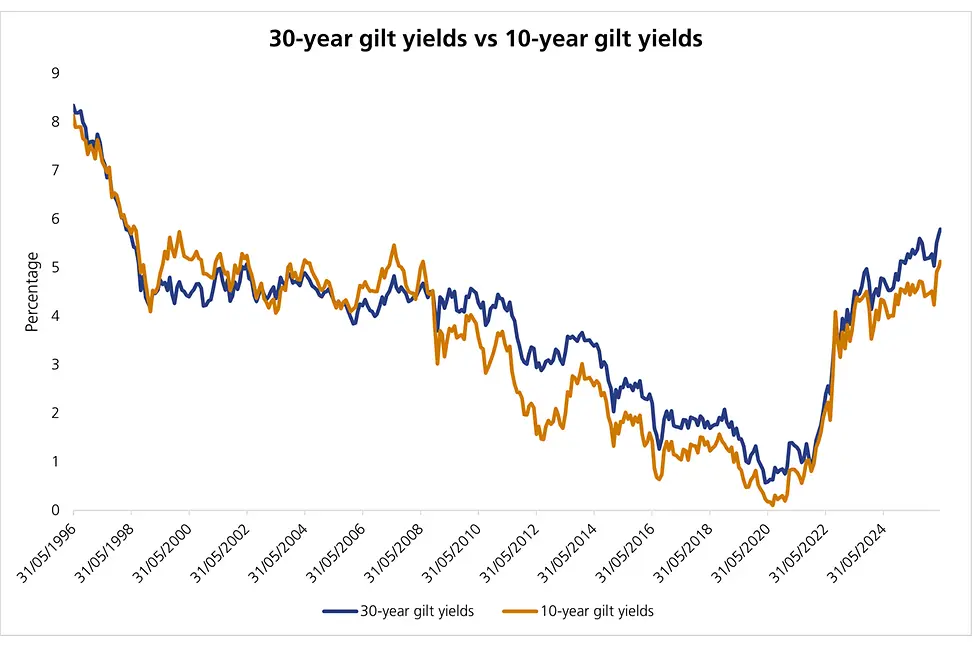

Ten-year gilts decisively broke through 5%, while 30-year gilts are yielding 5.8%, the highest levels since 1998. Although the UK has managed to avoid the title of the “sick man of Europe” – previously used for Italy and Greece during the European sovereign bond crisis in 2010 – international investors are becoming increasingly wary of investing in UK sovereign debt.

Looking ahead, markets are likely to remain focused on the balance between supporting economic growth and maintaining fiscal discipline. For now, investors are demanding a premium to finance UK government borrowing, which may offer opportunities for domestic investors to lock in higher yields over the coming weeks and months, but volatility will remain elevated for some time.

[1] Andy Burnham: Britain is still “in hock to the bond markets” - New Statesman

[2] Andy Burnham's provocative challenge to Starmer shows he is serious - BBC News

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.