Since the start of the month, investors have been assessing whether the war in Iran will be short-lived or escalate into a more prolonged conflict. Over the weekend, President Donald Trump posted on social media that if Iran didn’t “fully open, without threat” the Strait of Hormuz within 48 hours, the US could respond by targeting Iranian power infrastructure. Iran indicated it would retaliate by targeting energy infrastructure across the Gulf, raising fears of sustained high energy prices.

This prompted a sharp sell-off in equities and bonds on Monday morning as Brent crude rose above $110 per barrel on 23 March. Trump subsequently announced a five-day pause on attacks on infrastructure, stating that talks with Iran were progressing. This pattern of de-escalation amid mounting pressure has been a key feature of Trump’s second term.

About a year ago, Trump stunned markets by proclaiming 2 April as so-called Liberation Day and announcing tariffs on the US’s largest trading partners. This triggered a significant sell-off in equity and bond markets. However, the measures were later paused to allow time for trade negotiations, helping restore confidence. Ultimately, strong enthusiasm for artificial intelligence (AI) and broader global growth outweighed tariff concerns, driving equity markets to double-digit returns in 2025.

After announcing talks were in progress on 23 March, the following day the US reportedly sent Iran a 15-point proposal to end the war, with mediation discussions said to be taking place in Pakistan. 1 At this stage, it remains unclear whether this is a temporary delay ahead of further escalation or the start of a meaningful path towards a ceasefire.

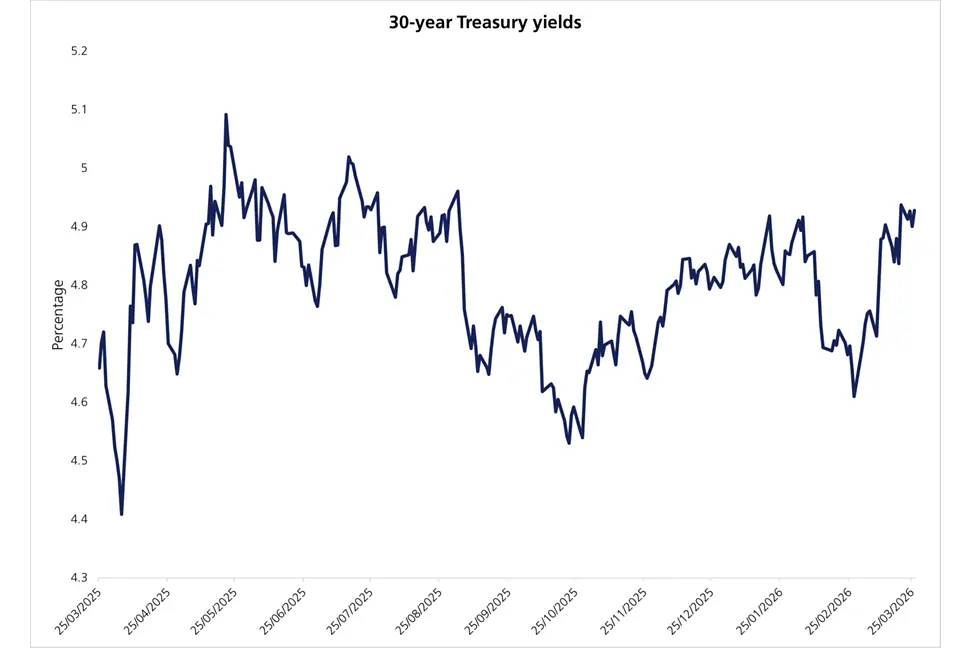

Bond markets may offer insight into the Trump administration’s pressure points. When 30-year Treasury yields hit 5% in 2025 following the tariff announcement – signalling concerns about inflation and borrowing costs – the US government ultimately stepped back and paused the tariffs. This week, 30-year Treasury yields approached similar levels.

At the start of the year, investors expected Trump to focus on tax cuts included in the “Big, Beautiful Bill” passed last year, aimed at supporting household incomes and boosting consumer confidence. This, in turn, could strengthen support for the Republicans ahead of the November midterm elections. Inflation was a key factor in the 2024 general election, and Trump has remained focused on keeping energy prices low to support consumer sentiment.

The recent surge in energy costs – driven by the conflict in Iran – directly challenges this objective, which is why many investors expect the situation to remain contained. Prices for essentials such as food, housing and consumer goods remain elevated, and if petrol prices – previously a point of political strength for Trump – remain high, this could lead to big losses for his party in November.2 Some observers believe that, alongside rising bond yields, higher petrol prices in the US have contributed to Trump moderating his tone in recent days.

There are, however, several challenges for investors. Conflicts are inherently unpredictable and require agreement from both sides to reach a resolution. It also remains uncertain whether Iran will be willing to engage in negotiations – its control over the Strait of Hormuz has given it leverage that is working in its favour, and global leaders have urged Trump to step back. There are now reports Iran is working on a draft bill that would impose a $2 million fee on vessels seeking safe passage through the Strait, a policy unlikely to be accepted by its Gulf neighbours.3

Markets recovered this week as Trump adopted a more conciliatory tone, easing pressure on energy prices. Brent crude began the week at $115 per barrel and ended at $106 on Thursday, while European equities, after falling sharply on Monday, rebounded by 3% from their lows by the close on 26 March. Bond yields initially declined as expectations for further interest rate increases faded, although hikes were priced back in towards the end of the week.

The conflict is ongoing and the outlook remains unclear. However, the apparent willingness to pursue negotiations has eased immediate concerns. The situation is likely to remain fluid, with the risk of further escalation still present. The speed at which policy direction can shift highlights the danger of reacting too quickly to short-term market movements. While opportunities may arise for investors, it remains important to stay cautious and maintain a disciplined, long-term approach in the face of short-term volatility. This is especially important given the sharp intraday moves seen in equities, which moved by as much as 4% within a 15-minute window on Monday.

[1] Surge in US gas prices deepens political peril for Trump over Iran - BBC News

[2] Iran drafts law to impose tolls for transiting Strait of Hormuz | The Straits Times

[3] Trump's 15-point plan passed to Tehran as Iran says US is 'negotiating with itself' - BBC News

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.