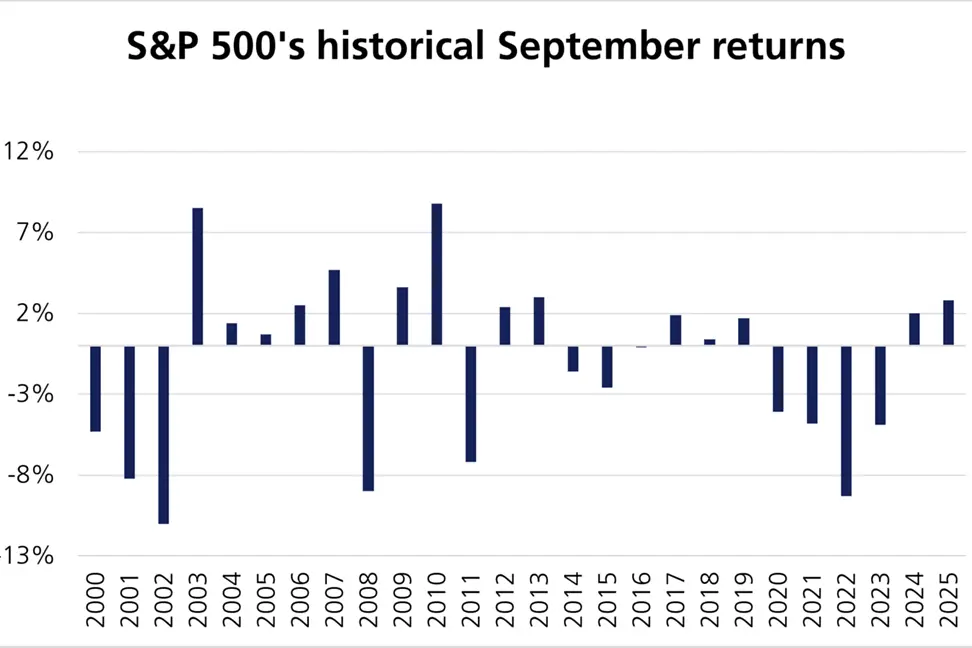

September has a reputation for being a challenging market for global stock markets. Going back nearly a century, equities tend to underperform in September more compared to any other month.1

This year has seen plenty of ups and downs, including tariff-related turbulence, followed by a strong rally in global equity markets. The S&P 500 rose 10.8% through the end of August while the MSCI World rose 5.5% in pound terms. Given September’s reputation, many expected a reversal, but this year, equities bucked the trend, with the S&P 500 rising 2.3% and the MSCI World up 3.1% in sterling terms through 25 September.

There are several reasons why September has historically been a difficult month for equities. One is seasonality. There is the longstanding theory that investors return to work from the summer holidays and rebalance their portfolios or take profits, which results in selling pressure. Tax and fiscal year dynamics have also played a role. In some jurisdictions, mutual funds and institutions may sell holdings before fiscal year-ends – for example, the tax year ends in September for mutual funds in the US – contributing to downward pressure. There is also a belief that individual investors liquidate stocks going into September to offset school fees.

Now, most economists believe the so-called September Effect has faded. Market participants are aware of it and may adjust their behaviour accordingly, such as selling in August instead. Notably, major September selloffs have become rarer since the 1990s.2

The 2.3% jump in the S&P 500’s performance this September can be partly attributed to expectations ahead of the Federal Reserve (Fed) most recent rate cut and the belief that it will lower rates further in 2025. Interest rate cuts benefit equities for several reasons:

While historical trends like the “September Effect” can influence short-term sentiment, they are only one piece of a much larger puzzle. Economic fundamentals, monetary policy decisions, and investor psychology all drive equity performance. Markets are forward-looking. When investors anticipate a shift in central bank policy, such as cutting interest rates, they often react in advance. This is evident as major market moves are often driven more by expectations. This brings to mind the old phrase “buy the rumour, sell the fact.”

Seasonal patterns and historical averages provide helpful context, but making investment decisions based purely on the time of year can lead to undesirable outcomes. Underlying economic trends, fiscal and monetary policy direction, and individual portfolio objectives are far more important. Diversification and a disciplined approach are crucial when navigating market cycles, whether we witness a slump or a surprise rally in September.

[1] September Effect: Definition, Stock Market History, Theories

[2] September Effect: Definition, Stock Market History, Theories

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.