Investors began the year expecting central banks to continue gradually reducing interest rates after they peaked three years ago. Since then, most major central banks – including the Federal Reserve (Fed), the Bank of England (BoE) and the European Central Bank (ECB) – have embarked on gradual rate-cutting cycles.

More recently, policymakers have begun discussing whether rates are approaching the so-called neutral rate, the level that neither stimulates nor slows economic growth.

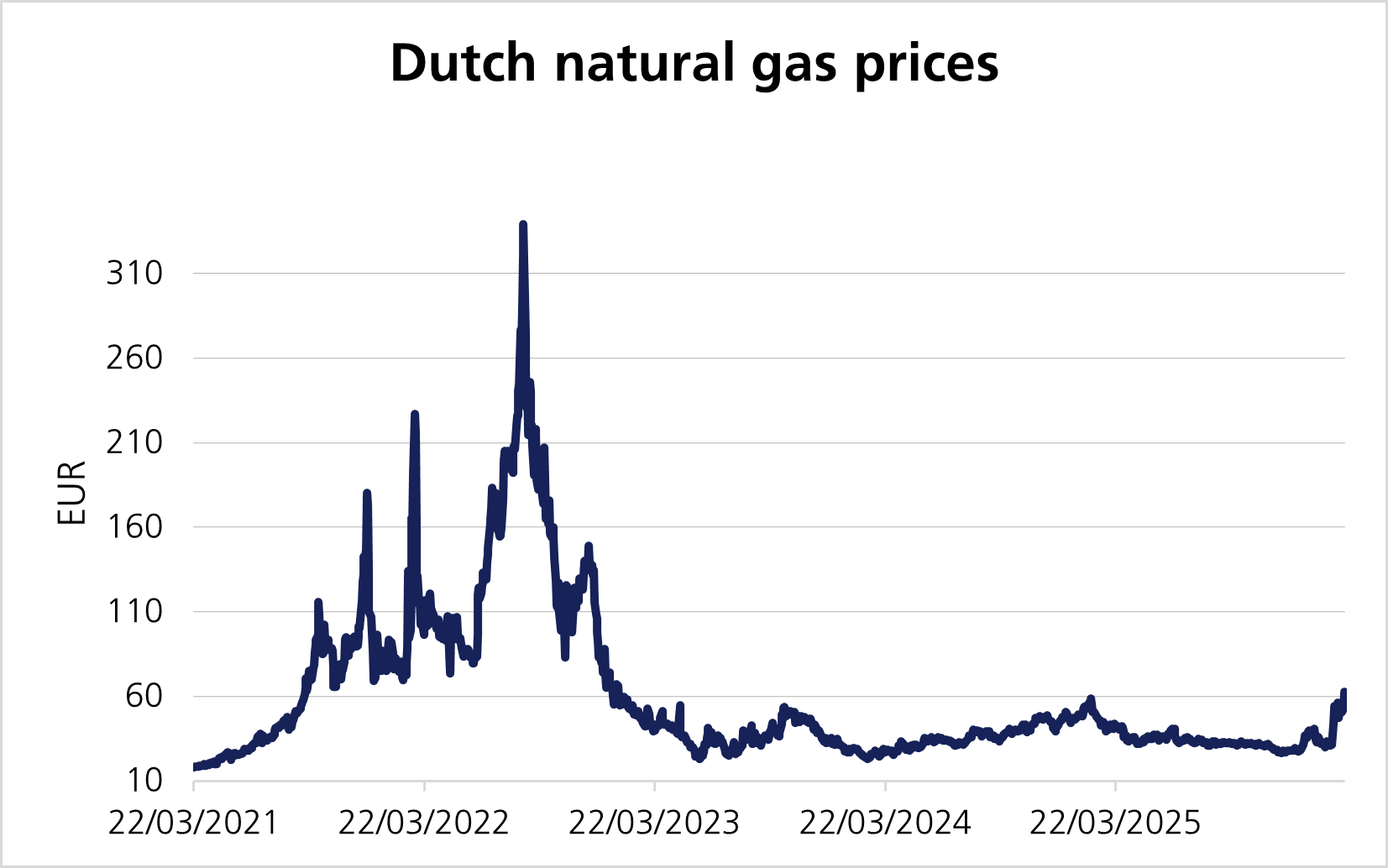

However, this trend has been complicated by the ongoing war in the Middle East which has driven sharp increases in oil and natural gas prices. The Strait of Hormuz – the crucial 21-mile passageway where around 20% of the world’s oil supply passes through – remains mostly closed. This disruption to global energy supplies has pushed energy prices higher and upended the inflation outlook.

As the commodity price shock interrupted the gradual decline in inflation, this week’s central bank meetings were particularly important. Surging energy costs, from rising oil and natural gas prices, will lift inflation and weigh on growth. This will force businesses and consumers to adapt to higher costs, issues that will likely intensify if the conflict persists. This is a particularly difficult combination for central banks, especially those that target inflation. Policymakers must decide whether to continue cutting interest rates, pause the cycle for a period, delay further easing altogether, or even potentially raise rates.

The latest nonfarm payroll figures in the US showed the economy lost 92,000 jobs in February.1 In normal circumstances, this would be a key development for the Fed and arguably more important than inflation, but this has changed post-conflict. Meanwhile, in the UK, private sector wage growth moderated to 3.3%, which would have cemented the case for a March BoE rate cut had it not been for the events in the Middle East.

On 18 March, the Fed held rates steady as widely expected, although officials indicated they still expect to deliver a one-quarter point rate cut later this year, even as the war in Iran has made the outlook uncertain. Chairman Jerome Powell emphasised that it was far too early to know how inflation and the labour market would be affected. “The thing I really want to emphasise is that nobody knows,” Powell said.2 On whether the bank would focus on inflation or employment, he indicated the Fed would look to balance both, but the immediate risks to inflation are more acute. Consequently, no action is off the table, but a prolonged pause seems likely.3

Both the BoE and the ECB held rates steady as policymakers assess the impact of rising energy prices on inflation and growth. The BoE held rates at 3.75%, a unanimous decision. This was a hawkish surprise, as the market expected some Monetary Policy Committee members to vote for cuts.4 Before the conflict, markets were expecting the BoE to cut rates twice this year, but expectations have now shifted sharply towards potential rate hikes amid concerns of rising inflation, driving gilt yields notably higher. Governor Andrew Bailey noted the BoE “stands ready to act” to keep interest rates at levels that will keep inflation under control.5 The BoE said that the conflict could push inflation as high as 3.5% in July.6

The ECB kept rates steady at 2% while raising its inflation forecasts to an average of 2.6% this year from 1.9%. Further out, they expect inflation to return closer to their 2% target. Consequently, they are closely monitoring medium-term risks to their inflation forecasts before deciding on future moves.

British and European government bond yields have sold off sharply as markets scale back expectations for rate cuts and begin pricing in the possibility of a rate hike later this year. Since the end of February, ten-year government bond yields in the UK, US and Germany have risen by 0.6%, 0.3% and 0.3% respectively.

To put the situation into context, it is useful to compare it with the 2022 energy shock. At that time, gas prices were already sharply higher over the cold winter and consequently surged by over 300%. While gas prices have nearly doubled in these few weeks, the scale of increases dwarfs that of 2022.

Furthermore, interest rates were much lower and labour markets stronger in 2022, allowing employees to negotiate higher wages. This kept inflation higher for longer, prompting central banks to tighten monetary policy aggressively.

Today the situation looks different. Labour markets are weaker, meaning employees are in a less powerful position to demand higher wages to offset rising living costs. It seems likely the energy shock will drag on growth, as real household incomes are squeezed in the months ahead.

While the latest energy shock has reignited inflation concerns, the broader economic backdrop suggests a more nuanced outlook. Softer labour markets and weaker growth mean central banks will proceed cautiously, balancing near-term inflation risks against longer-term economic stability. Central banks will hold steady while remaining open to adjusting policy once the outlook becomes clearer. As bonds adjust to these shocks, there may be opportunities for investors to lock in higher yields.

[1] Bureau of Labor Statistics

[2] Fed Holds Rates Steady as War in Iran Upends the Economic Outlook - The New York Times

[3] Fed Holds Rates Steady as War in Iran Upends the Economic Outlook - The New York Times

[5] Bank of England holds interest rates at 3.75% - live updates - BBC News

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.