The European Central Bank (ECB) met this week against a backdrop of heightened geopolitical uncertainty. An uneasy ceasefire in Iran has held despite the US and Iran exchanging fire midweek. While current oil prices have drifted from their highs, broader oil markets continue to reflect concerns that disruptions could persist for the coming quarters.

The ECB raised interest rates this week and signalled that bringing inflation back to its target remains its priority. For investors, however, the crucial question is whether the ECB raising rates marks a one-off response to the inflation shock or represents the beginning of a broader tightening cycle that could raise borrowing costs further.

Earlier this week marked 100 days since the US and Israel launched intense military strikes on Iran, a conflict that has since evolved into an uneasy ceasefire. Escalations earlier this week threatened to upend the delicate truce, and although President Donald Trump said on 8 June the US and Iran are “very close to signing a very powerful deal”, by 10 June, the US and Iran exchanged new strikes. As the US has now opted to stop further strikes, this has increased speculation that a deal is forthcoming. Consequently, investors and central banks have had to adapt to this choppy rhetoric which is resulting in an uncertain outlook.

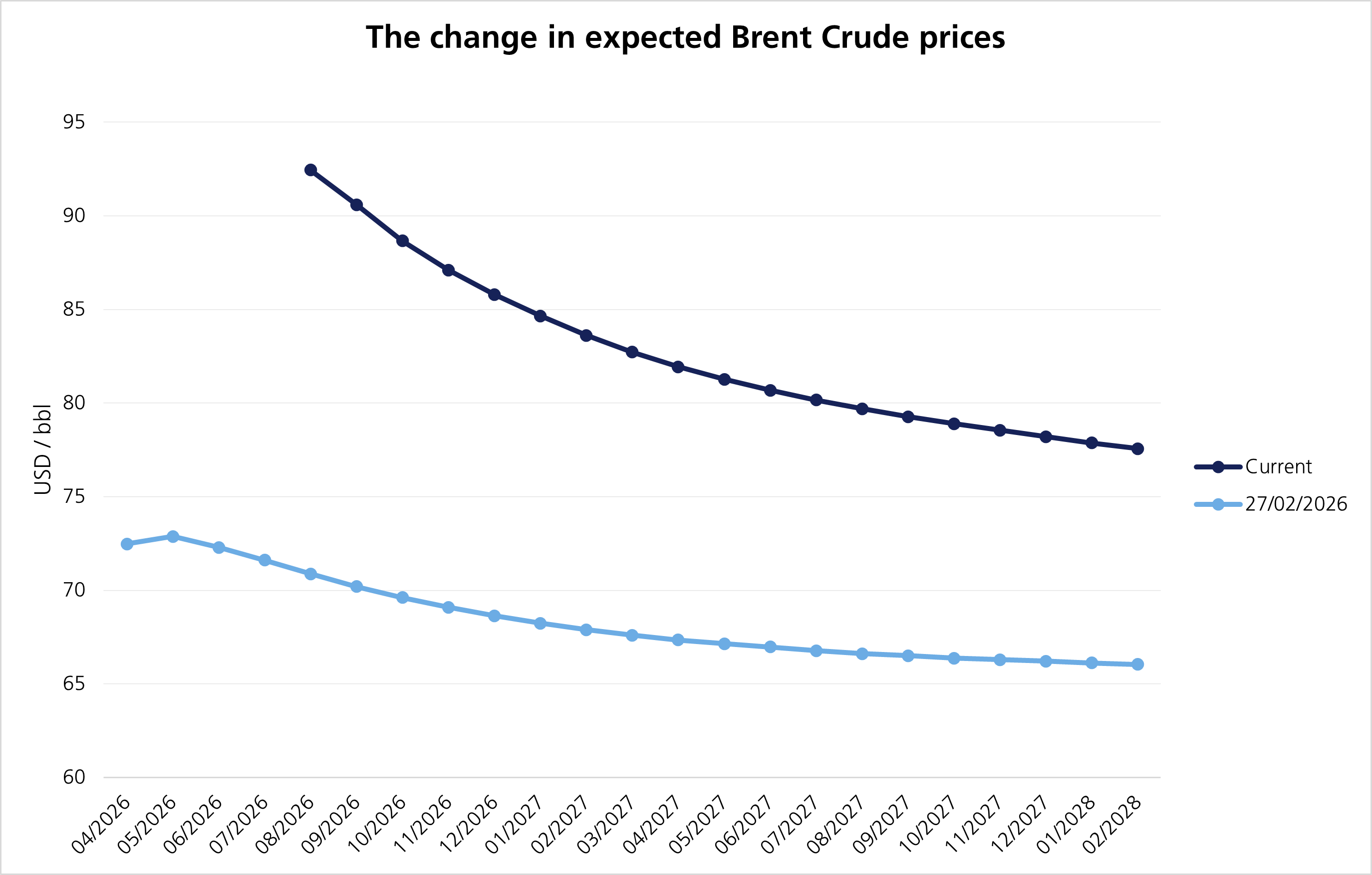

Oil prices rose sharply in early March following the strikes, and although Brent crude prices have eased from peaks of around $118 per barrel in late March, forward-looking oil prices – future prices that reflect investors’ expectations of where oil will be in the months and years ahead – continue to edge higher as uncertainty over the conflict remains. Regardless of what happens with a ceasefire or potential deal, disruptions in energy markets are likely to linger, with Brent futures remaining above $80 per barrel until year-end, a significant increase from the low $60 per barrel at the start of the year.

Against this backdrop, the ECB met this week and as expected, raised interest rates by a quarter of a percentage point to 2.25%, its first hike since 2023.

Although oil prices have come down from peaks earlier this year, inflation remains well above target for most central banks. They remain concerned about the second-order effects of higher oil prices, which raises transport and shipping costs and ultimately feeds into most food and goods. This poses a risk of inflation becoming more entrenched, something central banks are keen to avoid following the experience of recent years.

The ECB rate hike was all but a certainty. The real question ahead of the meeting was what comes next. During the press conference yesterday, ECB President Christine Lagarde noted that “the full implications of the war for medium-term inflation and growth will depend on the intensity and duration of the energy price shock, as well as the scale of its indirect and second-round effects.”1

She also added that the central bank is forecasting that rising energy prices will lift inflation further over the summer and keep it well above target into the first half of 2027, which will impact food, goods and services inflation, before starting to fall towards its target in the second half of next year.

Given the risks surrounding the conflict, which directly impact the ECB’s inflation target, the ECB opted to sound resolute in the face of the challenging outlook. The door has been left open for further increases, with markets expecting another 0.25% hike in September. While growth has been sluggish across the Eurozone, the ECB wants to act as a brake on inflation, despite the risks that rising borrowing costs will have on growth and labour markets.

Although inflation is above the ECB’s target, it has largely stayed in line with its forecasts, and the recent rise in core inflation – which excludes volatile items such as energy and food prices – appears to be driven by temporary services-sector distortions rather than persistent price pressures. In contrast to 2022, the last inflation shock, wage growth and labour markets remain subdued, reducing the risk of sustained inflation.

Oil prices staying higher for longer and their broader impacts on goods and service prices, mean central banks must be reactive. The Bank of Japan (BoJ) meets on 16 June and is largely expected to raise interest rates by 0.25%. The Federal Reserve (Fed) and Bank of England (BoE) also meet next week but are expected to keep rates on hold. Relative to the ECB and BoJ, policy rates are already higher, giving them more leeway to adopt a wait-and-see approach.

While policymakers are assessing the impact of higher energy prices, the current environment is far removed from the inflation surge seen during the pandemic. Inflation expectations remain stable, the labour market is softer, and there is little evidence of the scale of broad-based price pressures we have previously seen. As a result, policymakers will likely proceed cautiously with policy recalibration, balancing the need to contain inflation against weakening economic growth.

This communication is provided for information purposes only. The information presented herein provides a general update on market conditions and is not intended and should not be construed as an offer, invitation, solicitation or recommendation to buy or sell any specific investment or participate in any investment (or other) strategy. The subject of the communication is not a regulated investment. Past performance is not an indication of future performance and the value of investments and the income derived from them may fluctuate and you may not receive back the amount you originally invest. Although this document has been prepared on the basis of information we believe to be reliable, LGT Wealth Management UK LLP gives no representation or warranty in relation to the accuracy or completeness of the information presented herein. The information presented herein does not provide sufficient information on which to make an informed investment decision. No liability is accepted whatsoever by LGT Wealth Management UK LLP, employees and associated companies for any direct or consequential loss arising from this document.

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority in the United Kingdom.